Netflix Fell 10% After Earnings. Is It Actually Cheap Now?

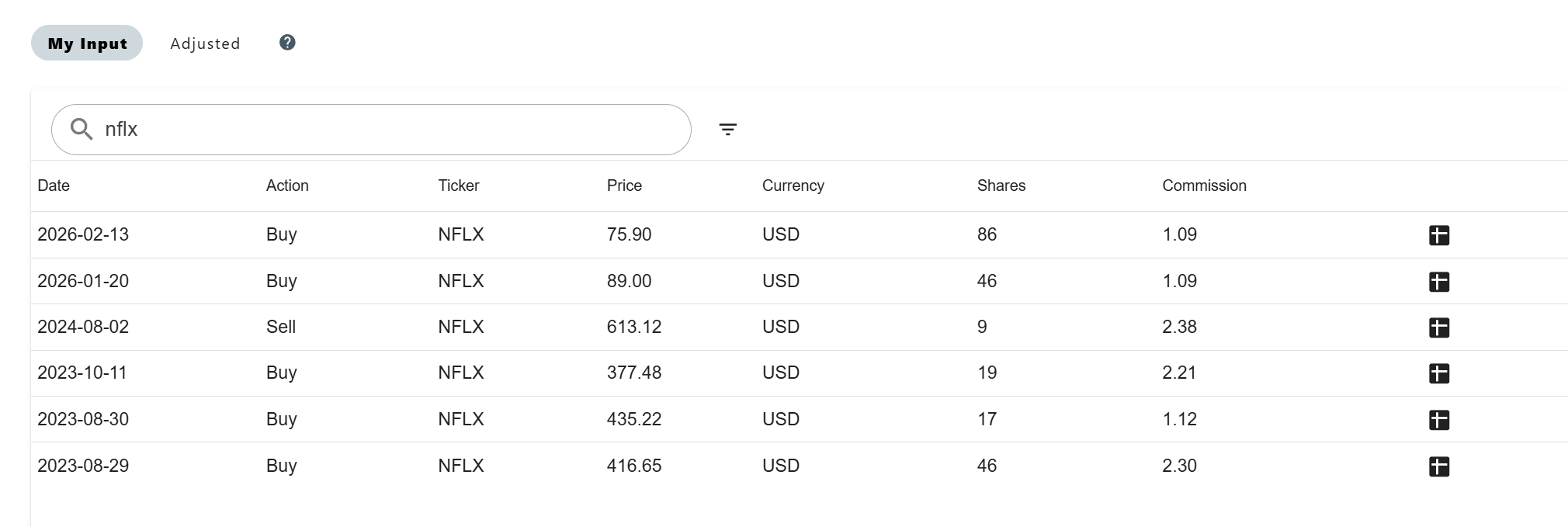

Netflix has been a hugely profitable stock for me. I've not shown this before, but here are my past buy transactions since I began accumulating the stock back in 2023 (note: divide pre-2025 stock prices by 10 to compare against current levels, due to the 10-for-1 split in November 2025):

And my overall gain so far nearly doubling my overall position at +97%:

This most recent earnings has been quite interesting, and in this article, I'll quickly cover:

- The Bad: Why the stock fell

- The Good: Highlights of Netflix Q1 2026 earnings

- Wrapping up: Should we be worried or optimistic on Netflix long-term?

- So, is Netflix undervalued or overvalued after this fall? My buy levels and portfolio positioning

Post Q1 2026 earnings, Netflix stock fell roughly 10% and is still 28% below its 52-week all-time high (see diagram below).

The Bad: Why the stock fell

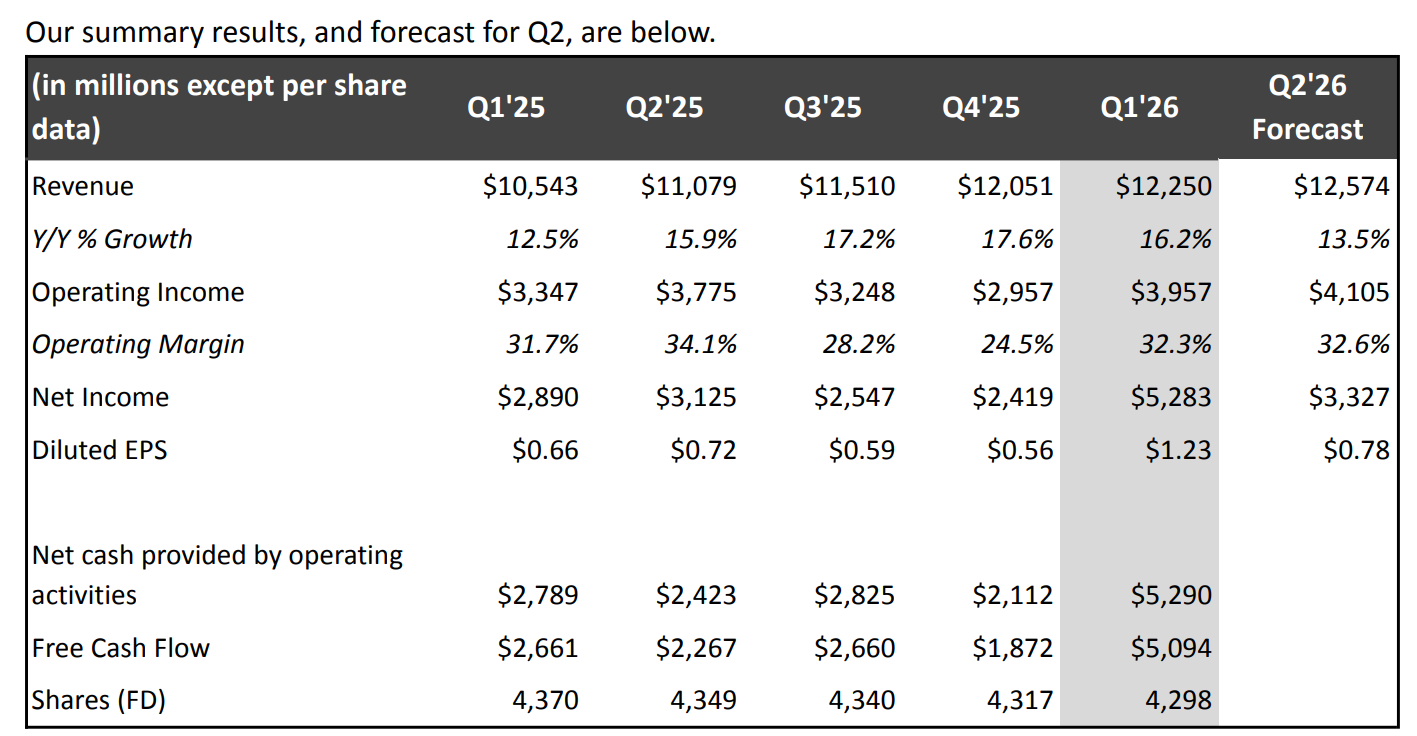

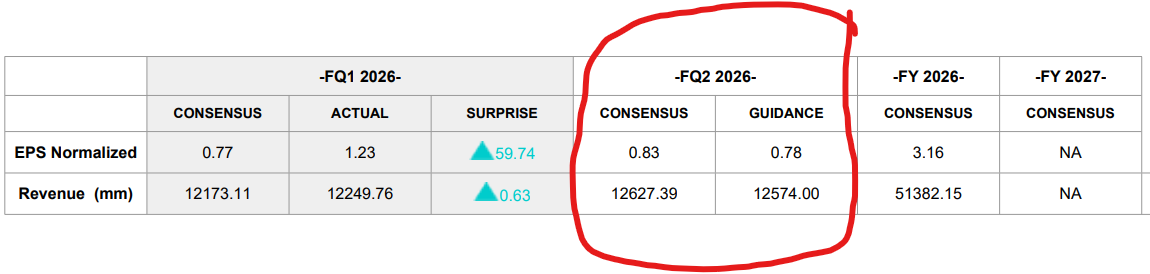

Weaker Q2 guidance

Revenue growth is set to decelerate from 16.2% in Q1'26 to 13.5% in Q2'26 (versus 15.9% in Q2'25).

- Operating margin is also guided down to 32.6% (vs. 34.1% in Q2'25)

- Diluted EPS of US$0.78 in Q2'26 will only be slightly higher than Q2'25's US$0.72, a significant deceleration from recent quarters.

Management did explain this in the shareholder letter. Content amortization is front-loaded in the first half of 2026 due to the timing of title launches.

So this is a timing issue, not a structural one. But the market doesn't care much about that nuance on earnings release as usual in the short-term! (Which is awesome, because analysts' short-termism is my long-term opportunity).

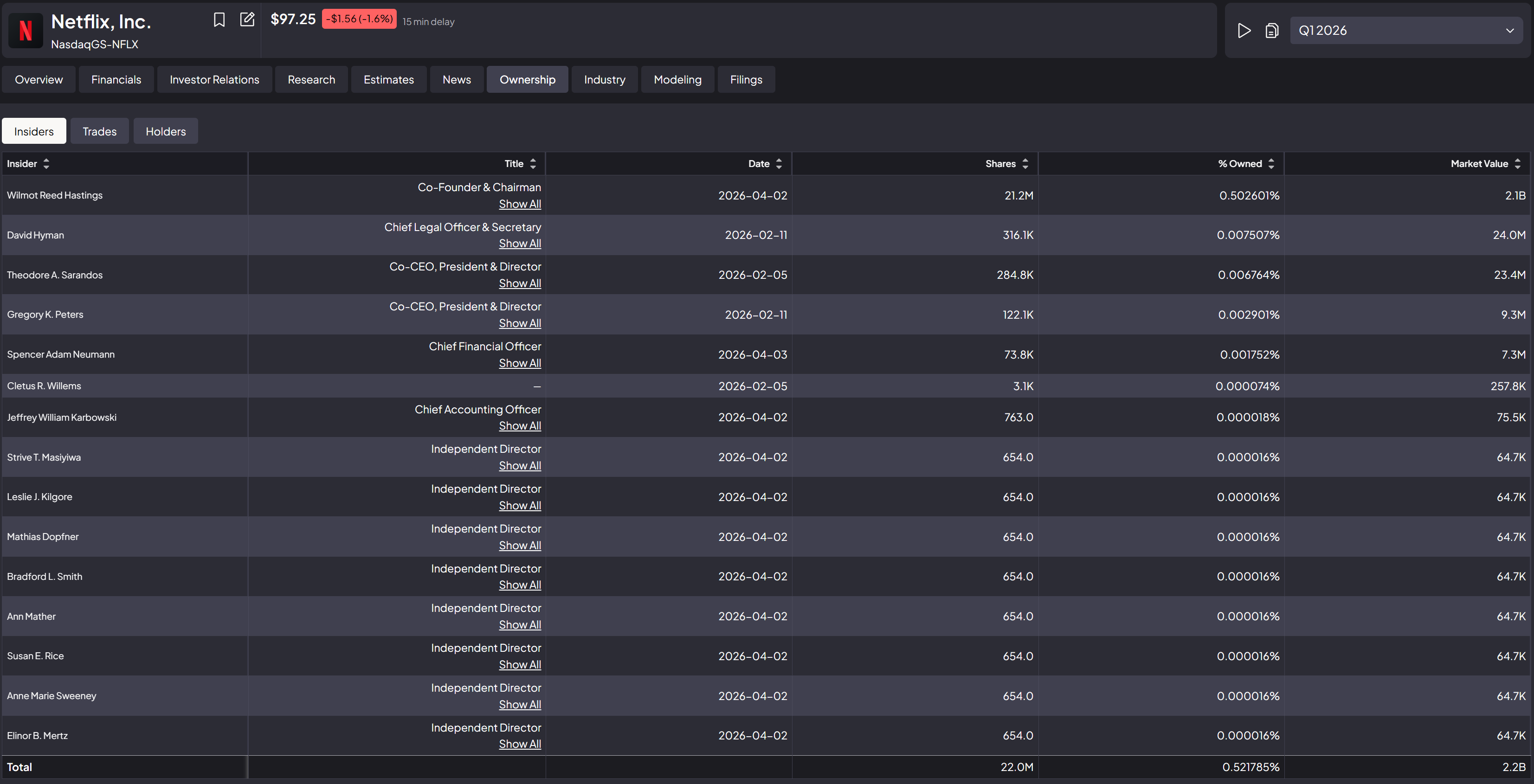

Reed Hastings is stepping off the board

In my opinion this is the biggest negative in this earnings print. Reed Hastings has informed the company he will not stand for re-election as Chairman to the Board at the upcoming June 2026 Annual Meeting.

That said, I really like the culture he's left behind with Ted Sarandos and Greg Peters as Co-CEOs. The way they handled the Warner Bros situation shows how far the leadership team has come. Sarandos put it well on the call: when the cost of the deal grew beyond the net value to the business, they were willing to put "emotion and ego aside" and walk away.

During the earnings call, Sarandos also said something important: it's very unusual for a founder to step away after a succession, but Reed is no ordinary founder. The succession has been planned for more than a decade and is not a sudden exit, so I'm not as fussed as I would be if a founder were suddenly leaving without any notice or reason.

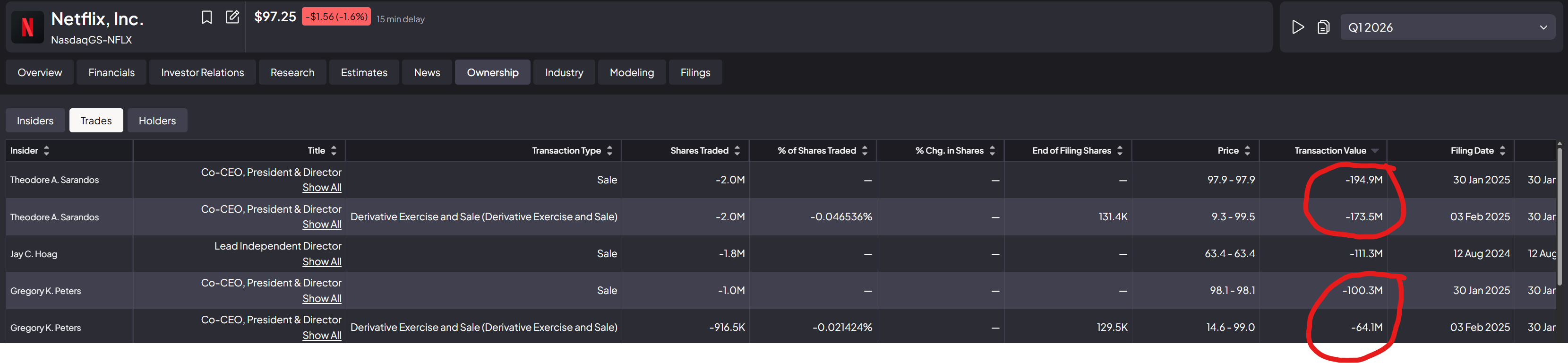

Skin in the game: the co-CEOs vs. Reed

Here is what I don't love. Sarandos and Peters both sold heavily in early 2025, near what turned out to be near-ATH levels. Sarandos offloaded roughly US$195M in a straight sale and another ~US$174M via derivative exercise-and-sale in Jan/Feb 2025. Peters sold ~US$100M straight and ~US$64M via derivative exercise-and-sale in the same window.

The result: current direct holdings are Sarandos at ~US$23M and Peters at ~US$9M.

Reed, who up till now has had by far the biggest skin in the game as chairman (21.2M shares, ~US$2.1B, most of his net worth is in NFLX), is the one leaving the board. So the two executives who'll be running the company day-to-day have meaningfully smaller personal capital at stake than their predecessor. A small part of me is worried about incentives being less motivating than they ideally would be.

The Good: Why I'm still optimistic

Advertising is still very early, and accelerating

Advertising revenue remains on track to reach ~US$3B in 2026, up 2x year-over-year. Netflix now works with over 4,000 advertisers, up 70% year-over-year.

To put US$3B in perspective, that's only about 6.5% of LTM revenue. Plenty of runway to go. And adoption signals are strong: the ads plan represents over 60% of all Q1 sign-ups in ad countries.

Operating margins are trending up, long-term

Q1'26 came in at 32.3%, and the 2026 target is 31.5%, up from 29.5% in 2025. Short-term, Q2 will dip to 32.6% vs. 34.1% last year due to the content amortization timing I mentioned above. But if we zoom out, overall direction of the operating margin trend still looks good! So it really depends if investors are in this for the long haul or short-term.

Gaming optionality

Two great positives on gaming were mentioned during the call:

- Netflix's virtual game controller app recently topped the US iOS download charts

- Greg Peters explicitly framed gaming as a ~US$150B consumer spend TAM opportunity (ex-China, ex-Russia, and not even counting ad revenue).

If even a fraction of the US$150B market becomes capturable, it's a meaningful long-term lever to increase revenues and profits. Overall, I see Netflix as having the potential to develop into a full entertainment platform, a place where we can watch movies/shows and play games and potentially listen to podcasts? (Speculating on the podcast part, but that effectively takes spotify marketshare)

Podcasts are proving incremental

Netflix has been quietly expanding into video podcasts, and the early data is interesting. Two specific signals on the call were mentioned:

- Podcast consumption happens during daytime hours, which is when Netflix historically has less engagement

- There is more mobile consumption of podcast, which is a surface where TV and film historically don't show up much. So this isn't cannibalising core TV viewing but is instead filling in new pockets of time in the day and so, is overall a genuinely additive engagement lever.

The bigger picture: monetization diversification lowers risk

For years, Netflix was essentially a one-lever business, i.e. grow subscribers, or go bust. That made the stock violently sensitive to every quarterly subscriber release. Today the levers have multiplied: pricing, advertising, engagement (via live events, gaming, podcasts), and distribution partnerships like MELI. Each one contributes independently, and each reduces dependence on any single driver.

A more diversified revenue engine is a more resilient revenue engine, and over time, a more predictably valuable one.

Wrapping up: the long-term thesis

There is no perfect investment where every checkbox is ticked green. Most of the time, you have to be happy with the conviction that the total long-term impact of the good outweighs the bad of a stock. My philosophy is:

Don't miss the long-term forest for the trees.

For Netflix, there are three primary reasons I'm looking to hold for the next 5–10 years (though I may be slightly less inclined to top up as aggressively now, given reduced skin-in-the-game concerns with Reed Hastings' departure):

- Advertising is still very early, with US$3B representing only ~6.5% of LTM revenue. Lots of runway for Netflix to grow revenues, profits and hence the stock price.

- Lots of optionality to expand the engagement and monetization surface: gaming (early/nascent), podcasting (early signs of success) and live events (pretty successful e.g. recent baseball game in Japan and Taipei 101 Alex Honnold) .

- Stable and expanding operating leverage, with margins trending up steadily over the years. Short-term guidance dips (like Q2'26) don't change the long-term direction.

So, is Netflix undervalued or overvalued after this fall? My buy levels and portfolio positioning

Note: The following does not constitute financial advice/recommendation and is merely a journal of my own portfolio investment actions.

Given that Q1'26 earnings carry a bonus US$2.8B termination fee paid by WBD to Netflix, we need to make some adjustments to value the stock properly today and remove the one-off distortion.

The way I like to assess Netflix's valuation is by looking at the...