Why I’m investing in the Nvidia of Medtech

Note: This is a premium tier article from Stock Research Vault. Most of it is free and at the end, I outline why I believe this company has more growth ahead, the risks and specific valuation buy levels I will be interested to add to my portfolio.

Over the past year or two, I've spent quite a bit of time in hospitals: seeing the gynae before my baby was born, then the gastro doctor for some stomach issues. Across completely different clinics, I kept noticing the same thing. Each one proudly display a certification plaque from one specific MedTech company.

I soon discovered that this company had, for more than two decades, effectively monopolized the soft-tissue robotic surgery field, and that its stock had returned roughly +20,000% since its 2000 IPO, against about +410% for the S&P 500 over the same period.

That company is Intuitive Surgical (Ticker: $ISRG).

Before I go further, I must admit something. If you've read this article, you'll know ISRG breaks my first criteria, Circle of Competence, since I don't work in the medical field. I won't pretend to be an insider, but to make up for it, I spent far longer than usual on this one, not just reading historical financial reports but speaking to as many doctors as I could and analyzing interviews with practicing surgeons.

In this article, I cover the following:

- What Intuitive Surgical does

- Business model and Economic Moat

- Industry & Competitive Positioning

- Financials

- Management

- Risks (🔒premium tier)

- Optionality & Growth Catalysts - Why it's still early days (🔒premium tier)

- Valuation Buy Levels & Portfolio Next Step (🔒premium tier)

What Intuitive Surgical does

Intuitive Surgical was founded in 1995 and develops robotic systems for minimally invasive surgery. Its flagship product, the da Vinci, was cleared in the US in 2000 and remains the clear market leader in robotic-assisted surgery.

Robotics is now the default for certain procedures. It accounts for roughly 95% of US prostatectomies (removal of prostate, mostly via da Vinci) and about 15% of US general surgery. Zooming out, robotic surgery is still only around 5% of all procedures in the US, 2% in Europe, and under 1% in the rest of the world.

Why Robotic Surgery over traditional surgery?

Before I dive into the company, it's worth mentioning why there is a need for robotic surgery at all.

Originally, open surgery (one large incision) was the norm, but it causes heavy bleeding and higher infection risk. Laparoscopic, or "keyhole," surgery came next: operating through a few tiny incisions instead of one big cut, which means faster recovery, less pain, and shorter hospital stays.

The problem with laparoscopic surgery

Manual laparoscopy has real drawbacks.

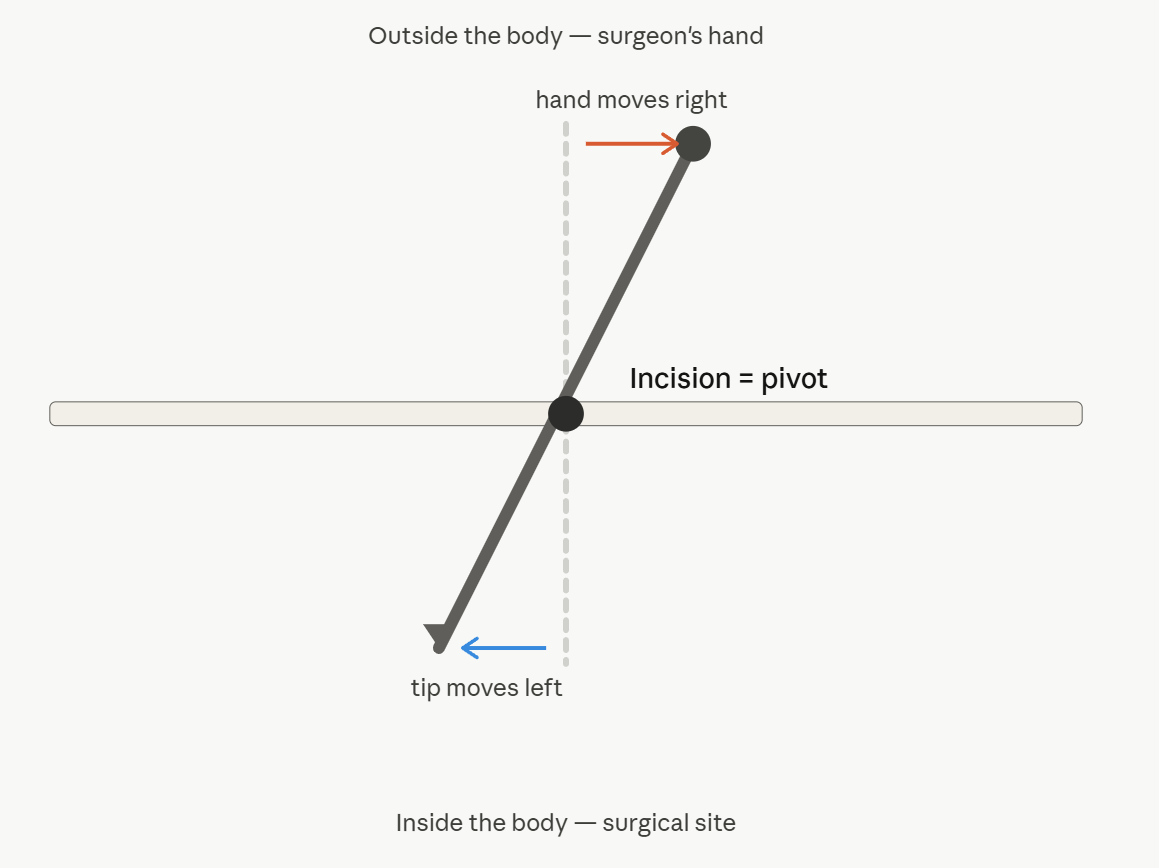

For doctors, dexterity is the big one. When a surgeon passes a long steel instrument through a small incision, he has to track the angle, depth, and rotation of the tool inside the patient's body the entire time. The hardest part is that every movement is reversed, because the incision acts as a pivot. Move your hand right, the tip swings left inside (see image below) and vice versa.

The surgeon's brain has to invert every movement, which is deeply unintuitive. The da Vinci robot removes this entirely. The surgeon sits at a console and uses hand controls that map directly onto the instrument tips inside the body, while the software un-reverses the motion, making the procedure more intuitive - hence the name, Intuitive Surgical.

With age, a surgeon's fitness may decline and there is a risk of shaking hands affecting surgical outcomes. The da Vinci system also filters out hand tremors, giving steadier movements than any human hand.

Ergonomics matter too. Traditional setups force surgeons to hold awkward hand and back positions for hours, wearing them down and affecting their career longevity after working with unergonomic setups over years. da Vinci lets surgeons operate seated at a comfortable console, reducing fatigue on long, complex cases.

Better for Patients

For patients, robotic surgery generally improves outcomes, providing faster recovery, shorter hospital stays, less blood loss, and a lower chance of needing a transfusion than open surgery.

In addition, although the cost of using robotic surgery is higher than traditional open or laparoscopic procedures for patients, when considering the reduced subsequent stay and potential for recurrent treatment, the total cost is either comparable or even lower, making it an all-round better choice for patients.

With that, let's get into Intuitive Surgical's business model and economic moat.

Business model and Economic Moat

Every da Vinci robot uses attachable instruments with limited-life. Each one has a built-in chip that counts how many times it's been used, and after a set number of procedures (e.g. 10), the chip shuts off. That forces the hospital to throw it away and buy a brand-new one from Intuitive. This is Intuitive's "razor and blades" money machine - the robot is the razor, the instruments are the new blades they keep selling.

We can see it in their financial statements:

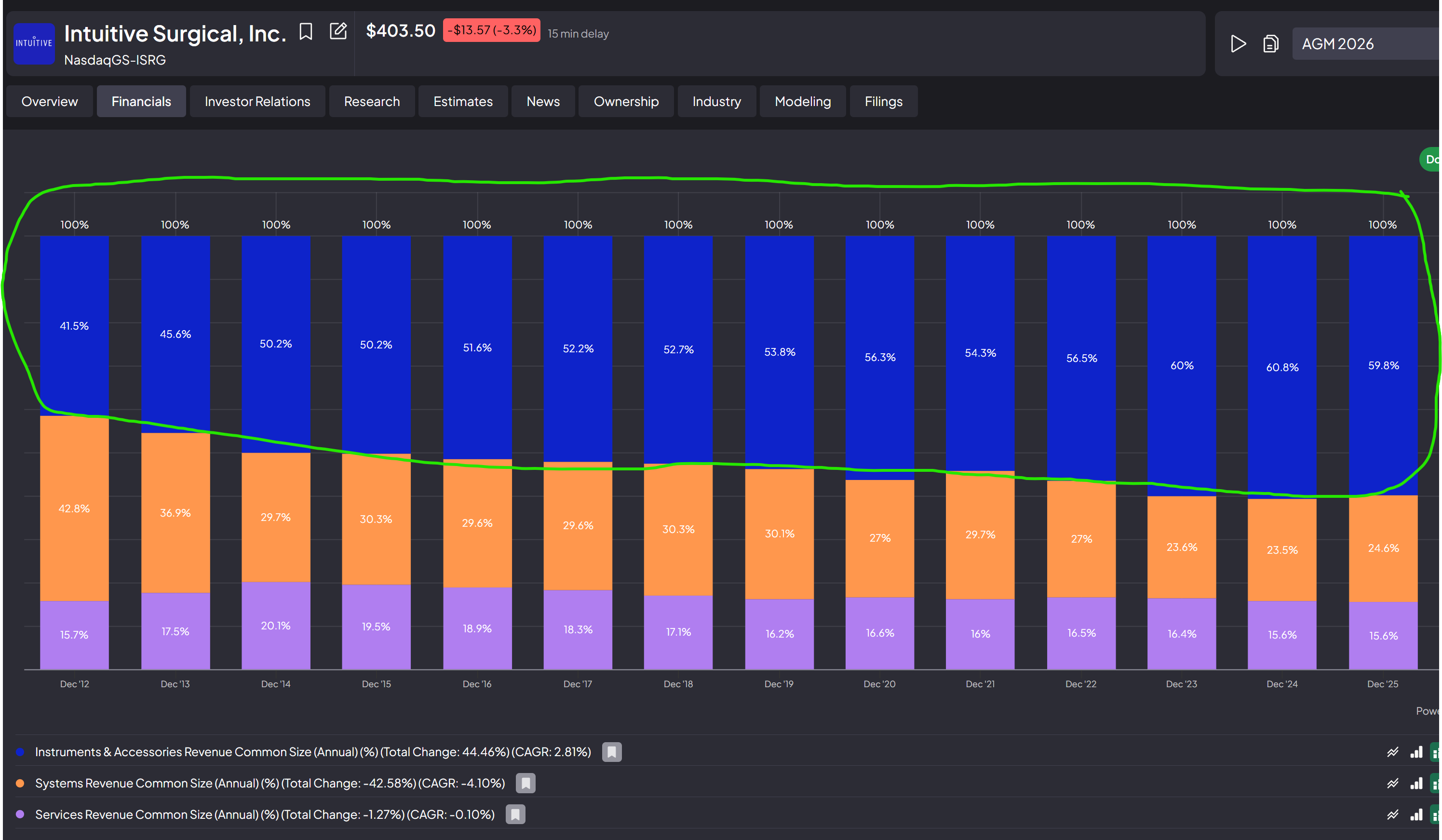

Over the last 13 years, I&A (Instruments & Accessories) has grown from about 42% of revenue to roughly 60%, and is now the clear majority. The trend continues to point in that direction.

The other revenue contributions include Systems Revenue (which is selling or leasing the da Vinci or Ion machines) as well as Services Revenue (which includes maintenance contracts and training programs).

Around 84% of Intuitive's revenue is now recurring (instruments, accessories, services, and usage-based system leases), not one-off machine sales.

Now the key question: what makes ISRG so special? What is the economic moat that lets it fend off competition and allows it to keep growing revenues and profits long-term?

Switching Costs & Ecosystem Moat

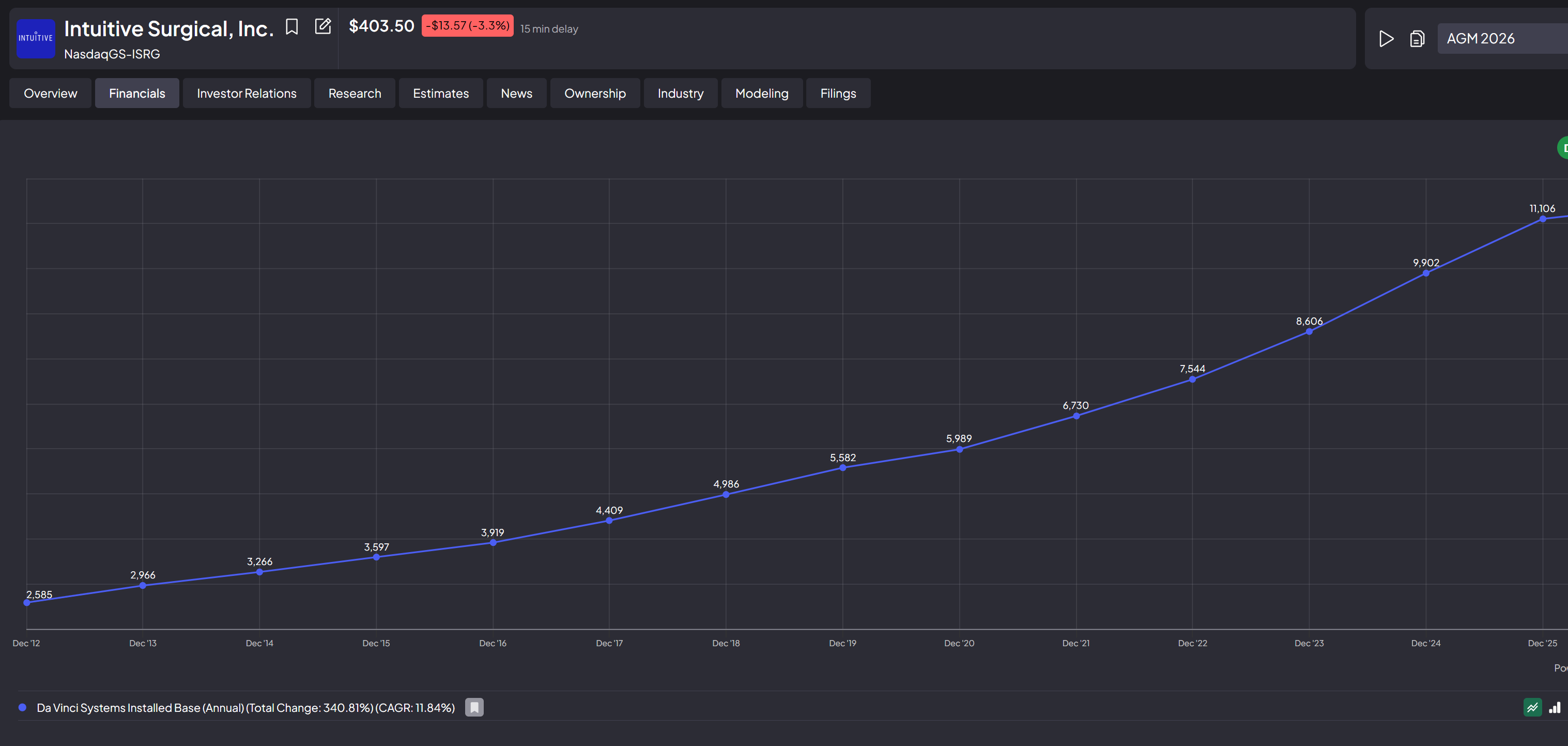

Since da Vinci's inception, Intuitive has grown its installed base to over 11,000 da Vinci systems worldwide (more than 12,000 counting its Ion lung-biopsy system), doubling on average every 6 years. Once a hospital adopts an Intuitive system, it gets embedded in procurement, or workflows, and daily operations, which makes it costly and disruptive to rip out, especially given the mission critical nature of surgical procedures.

The ecosystem is deeply entrenched in the global medical field as well. Over the past 25 years, Intuitive has trained more than 76,000 surgeons on da Vinci machines globally (including the doctors I visited in the past 2 years!). The robotic systems are also supported by 48,000+ peer-reviewed articles and to date, 20M+ procedures have been performed using Intuitive's systems. In a high-stakes, heavily regulated field such as surgery, this documented track record matters even more than ergonomics or a good sales pitch. Surgeons want to see clinical evidence, and no competitor comes close to da Vinci's ecosystem depth in soft tissue surgery.

This is why I equate Intuitive to the Nvidia of Medical Technology - a huge head-start in the field, plus the largest ecosystem of surgeons trained on its platform (much like Nvidia's CUDA lock-in).

This ecosystem continues to compound. da Vinci procedures generate data captured by the system, the data feeds academic work, that work proves out the system's efficacy, and the evidence loops back into Intuitive's R&D and the next sale and upgrade cycle.

This brings me to my next point on the industry and competition.

Industry & Competitive Positioning

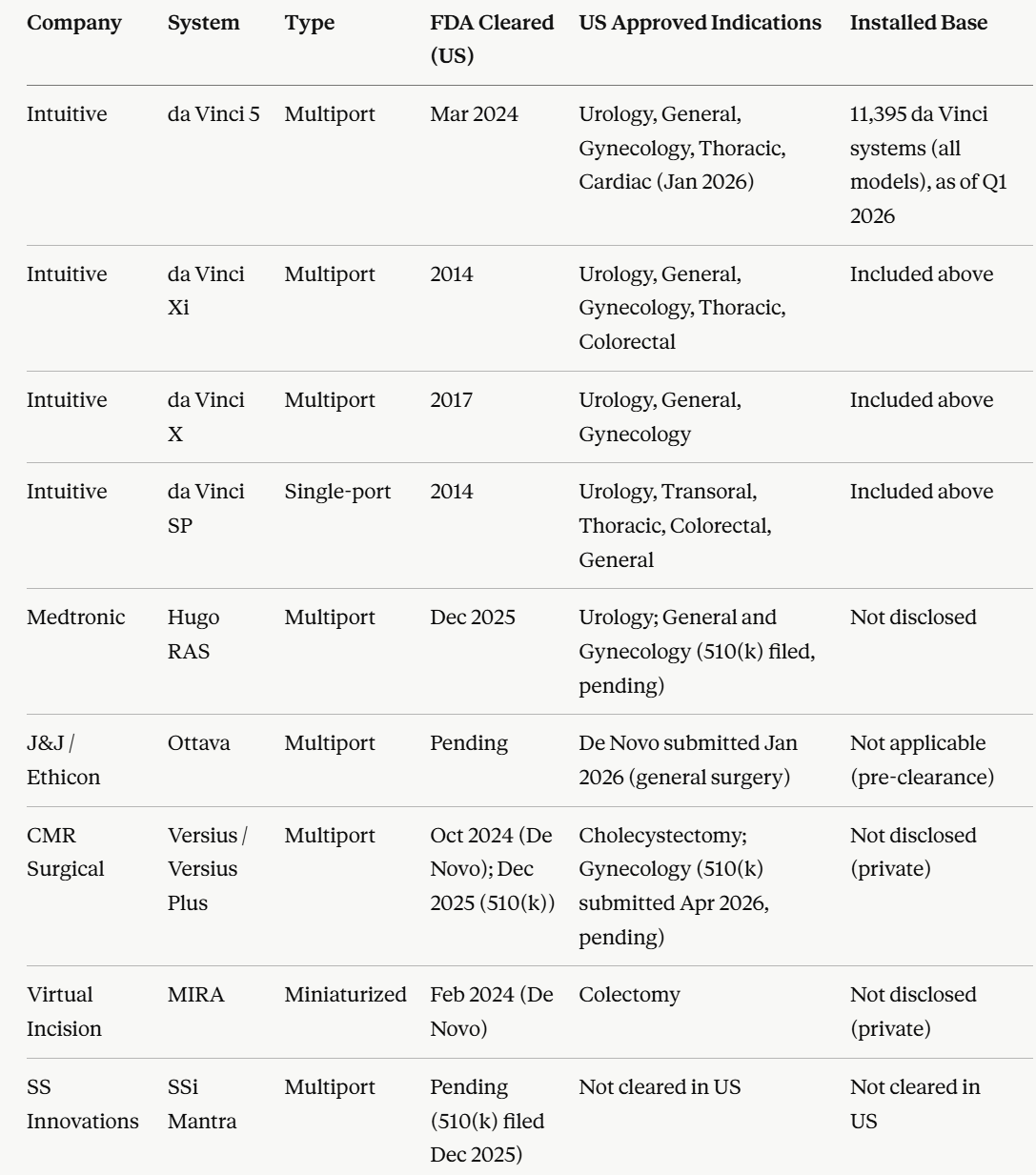

The table below lists competitors with cleared or pending FDA indications amongst competitors in the Soft Tissue Robotics space, the primary focus of Intuitive's market. For the layman, "Indications" just means the types of procedures a system is cleared for. The da Vinci 5, for example, is now cleared for five (Urology, General, Gynecology, Thoracic, and Cardiac as of Jan 2026). Every new indication expands the same machine's addressable market, letting hospitals run more procedure types on hardware they already own.

What stands out is that, thanks to its two-decade head start, Intuitive has the most FDA-cleared indications across the widest portfolio of systems (the various da Vinci models).

The closest US competitors to watch are Medtronic (Hugo, recently cleared for urology) and J&J (Ottava, pending). Internationally there's SS Innovations (India) and several China-based players I haven't listed.

Competitors can get FDA clearance eventually, so the FDA pathway itself isn't the barrier. The barrier is breadth - each indication needs its own filing, data, and time, and by the time a rival receives a new indication's clearance, Intuitive would already have pulled further ahead with newer da Vinci versions possessing greater capabilities.

There's also an economic problem for hospitals to consider. A competitor's machine cleared for only one or two indications would be comparatively under-utilized compared to a da Vinci 5, where urology, general, gynecology and other departments share one da Vinci system and keep it busy. That utilization gap makes the purchase harder to justify.

Drilling into Medtronic and J&J's robotic programs is where it gets interesting.

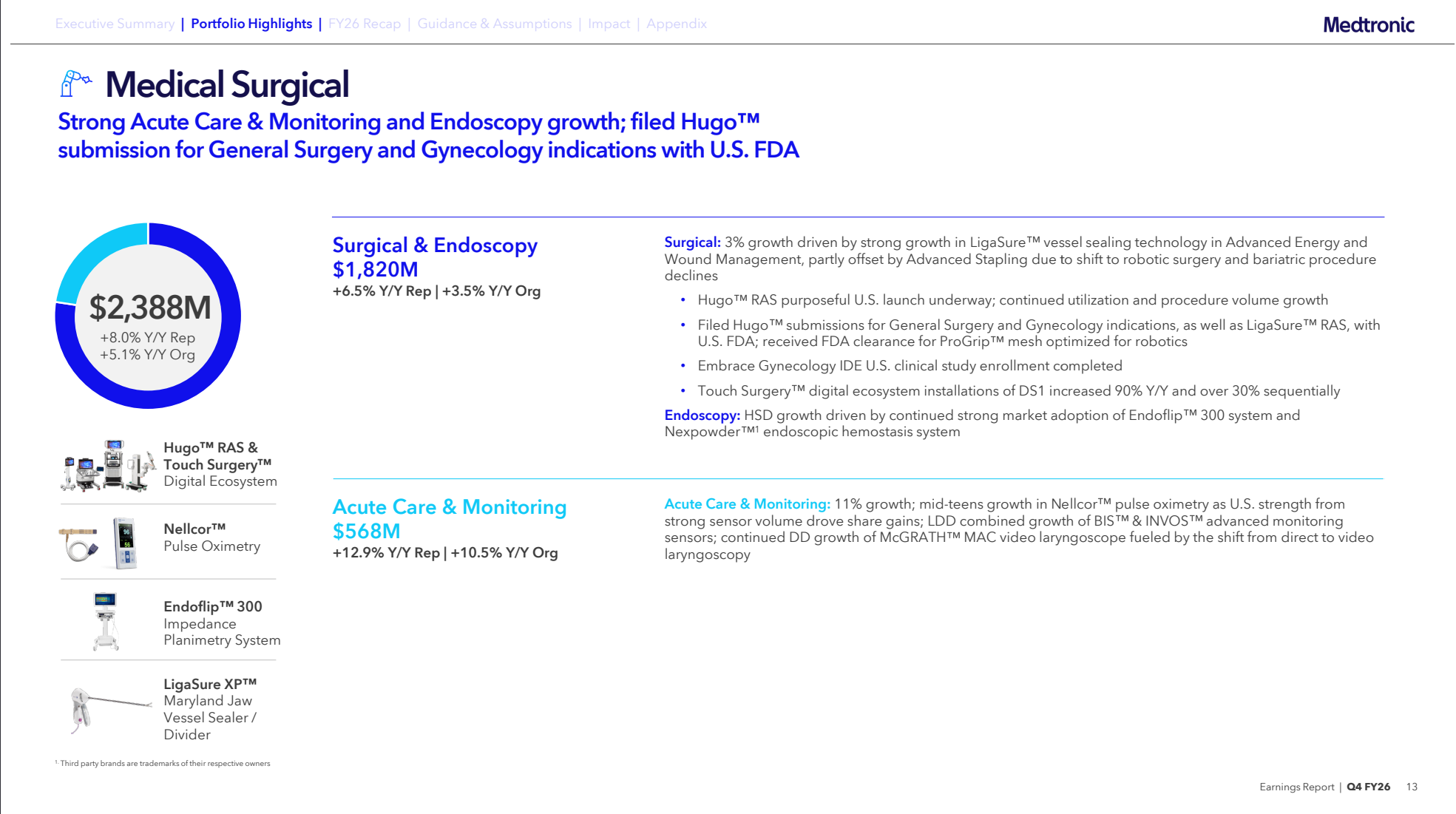

In Medtronic's latest quarter (below), Surgical & Endoscopy was $1.82bn of $9.8bn total revenue, about 18%, and their Hugo Surgical Robot is only a small slice of that, having been FDA-approved barely six months ago. Even generously assuming Hugo is 5% of surgical revenue, that's roughly 1% of Medtronic's total, barely a focus area for a company with four separate business lines. Intuitive, by contrast, puts 100% of its revenue and R&D efforts behind robotic surgery.

One interesting (and slightly hilarious) point I've observed is that in the quarterly declaration above, Medtronic stated that surgical growth grew only 3% "partly offset by Advanced Stapling due to shift to robotic surgery...". That is Medtronic effectively admitting that Intuitive (growing ~20%+ YoY) is taking share from its traditional, non-robotic stapling business. That pressure is likely why Medtronic built Hugo in the first place, a defensive move, and it points to the secular tailwind behind robotic surgery.

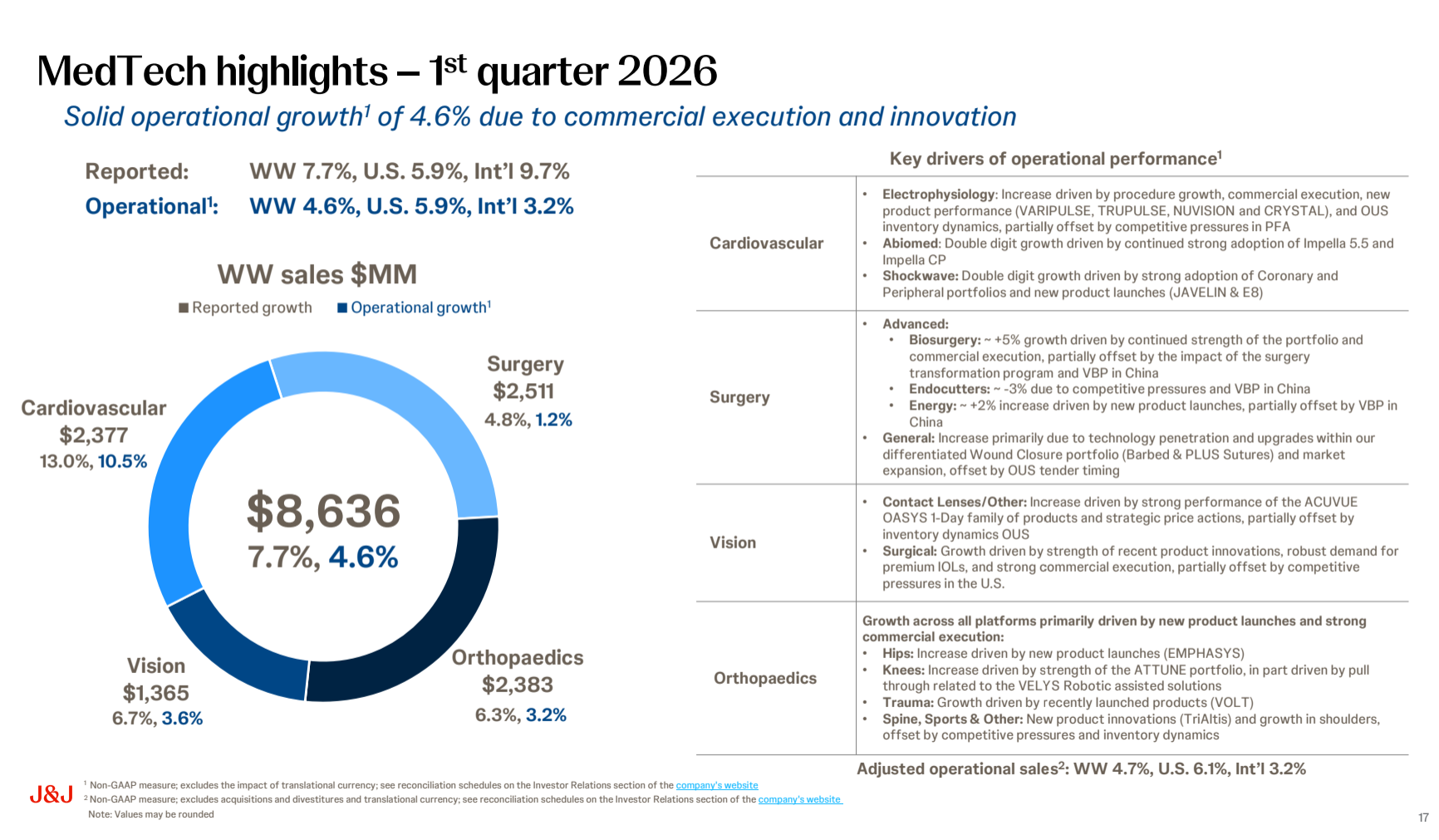

J&J's latest quarter tells a similar story.

J&J's Surgery line is $2.51bn, 29% of total MedTech revenue, one of four business lines. Ottava isn't approved yet, so it contributes nothing today. The lines to watch are Endocutters and Energy, the traditional instruments used in manual laparoscopy. When a hospital converts a manual procedure to da Vinci robotic systems, it stops buying J&J's handheld instruments (from the Endocutters and Energy business lines) and switches to Intuitive's platform-locked ones.

Both lines are stalling - Endocutters actually declined about 3% and Energy grew only about 2% YoY. J&J attributes this to competitive pressures and China volume-based procurement, so it's not all robotic substitution, but the direction reinforces the theme - traditional surgical supplies are flat-to-down while Intuitive compounds at over 20% YoY.

In a recent interview (39:39 to 40:20), Guthart makes a candid point about how Intuitive got here. For most of the last 25 years, the giants who could have challenged it simply looked the other way. J&J and Medtronic, the kings of manual laparoscopic instruments, had little reason to cannibalize their own cash cows, and the big imaging and capital-equipment players like GE and Siemens never seriously entered the field at all. That left Intuitive almost entirely alone, free to compound a single focused robotics bet for a quarter of a century while everyone else watched. By the time the incumbents grasped what robotic surgery had become and moved to compete, the lead was already built: thousands of installed systems, a deep base of trained surgeons, and a clinical-evidence record no rival can replicate quickly. Guthart frames it as a stroke of luck, but those same 25 years of uninterrupted execution are what turned the luck into a strong competitive moat.

With a feel for the business and the competition, we can finally get to Intuitive Surgical's financials.

Financials

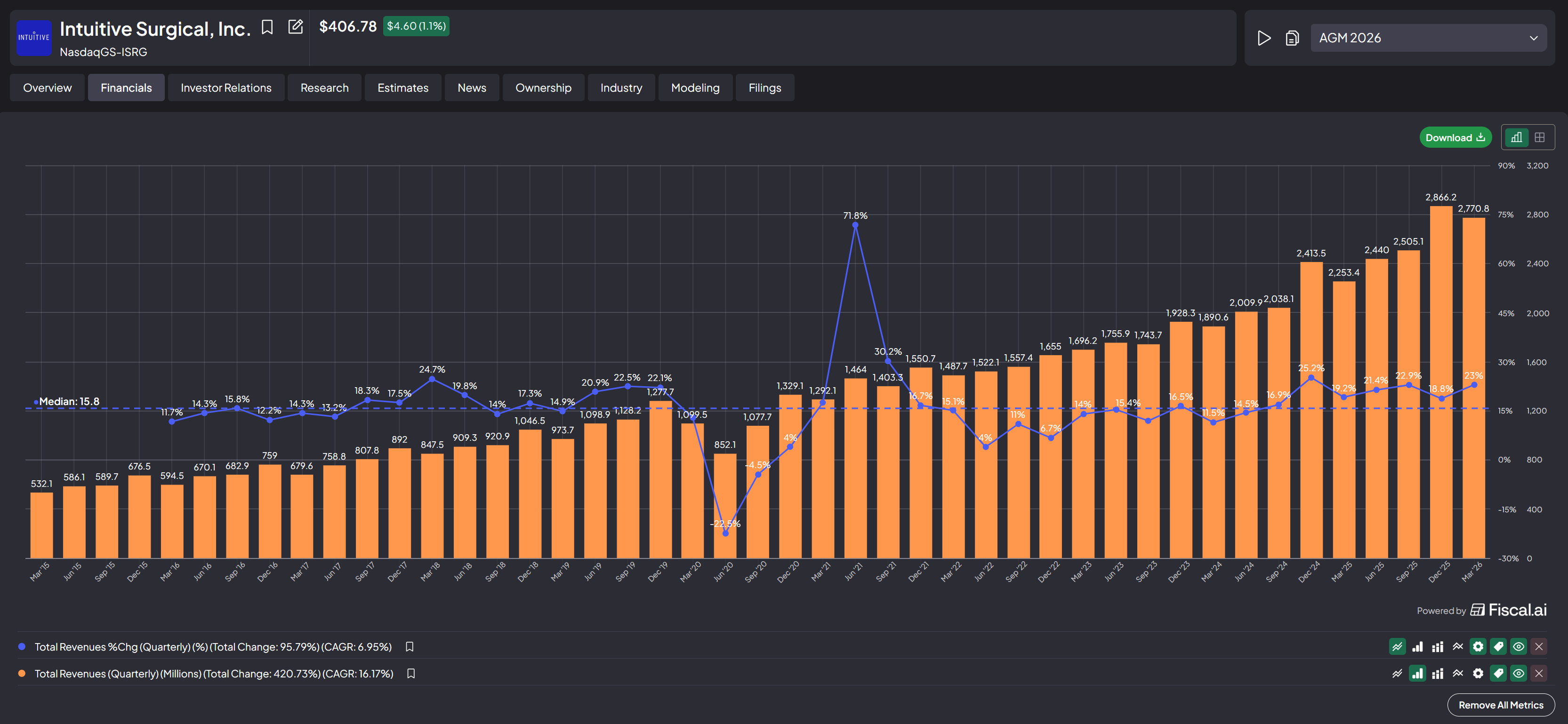

Over the last 10 years, Intuitive has grown revenues in a consistent uptrend (apart from the Covid dip), with median year-on-year quarterly growth of about 15.8% (see below).

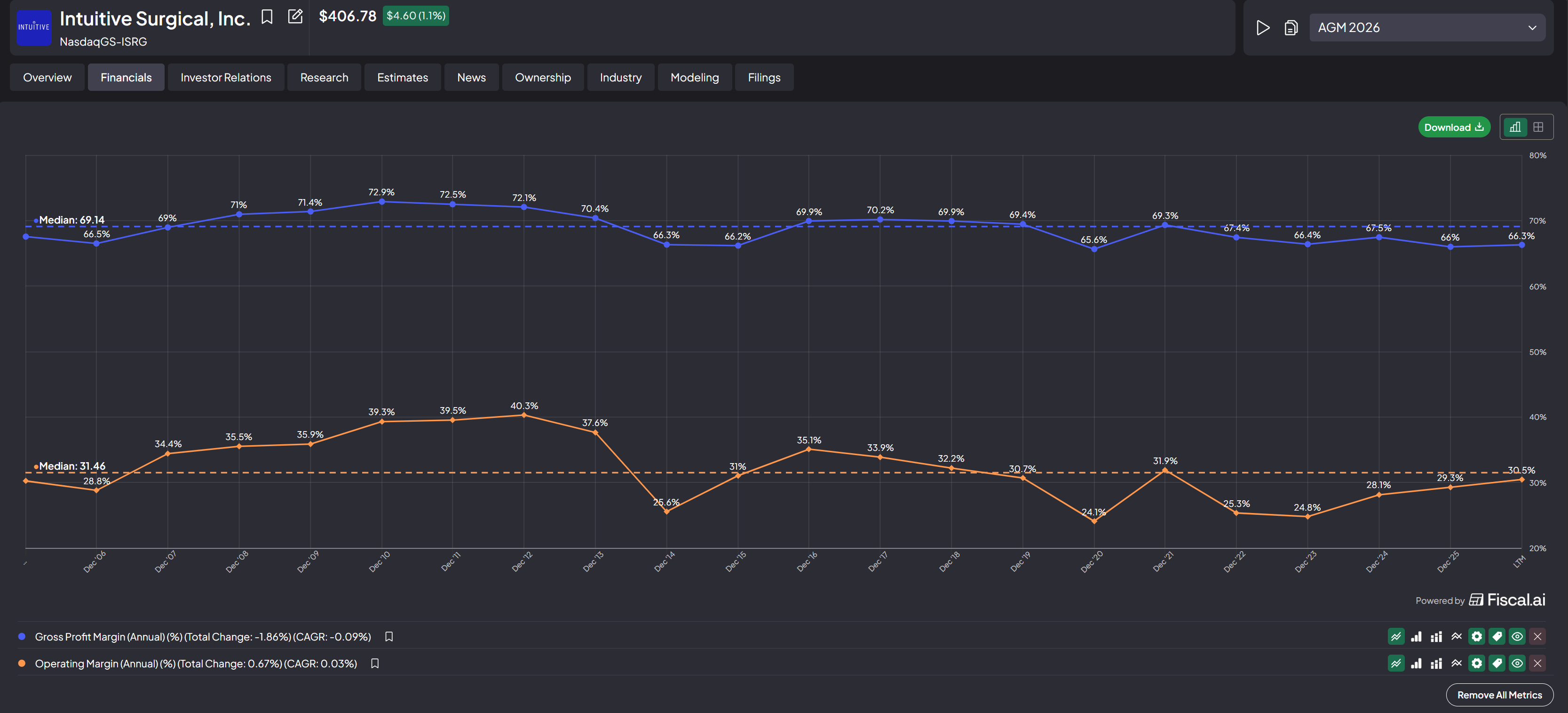

Margins-wise, Intuitive has held gross margins steady at a median of 69% (a good sign signaling USP/Product Moat is still largely stable), and over the same 20 year period, it has been very disciplined with costs, running operating margins at a median of ~31% (see below).

One of the highlights is that Intuitive has the highest historical margins (~31%) versus its US peers - J&J (~25%), Medtronic (~19.5%), Boston Scientific (~14.7%).

There is a reason why Intuitive has held the highest operating margins compared to its peers over the past 2 decades. Gary explains it best in this interview at the 49:55 mark:

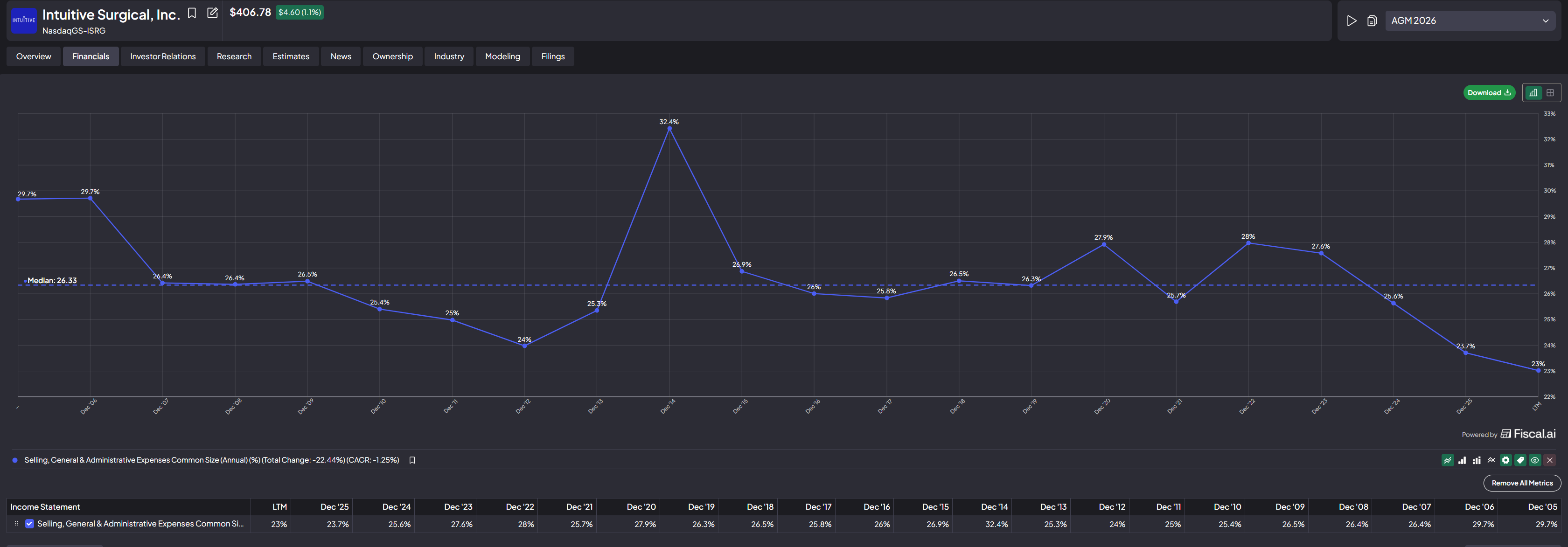

our SG&A is lower than our peer companies. And if you go why is that? It's not so much that our sales model is that different than theirs, but we have a highly concentrated portfolio. So we're not selling eight divisions worth of different products. We're quite narrowly focused and there we took inspiration from Apple and Steve Jobs have a narrow product set and make it really good. So that allows you to manage your uh expenses and um so we do that and we try to be on our administration functions we try to be highly efficient and do really well.

On checking the SG&A across the peer set, this appears to be true. We can see from the below, Intuitive's SG&A runs at ~26% (median) of annual revenues, compared to J&J (29.5%), Medtronic (33.9%) and Boston Scientific (35.7%), explaining why Intuitive produces the highest historical operating margins of the lot.

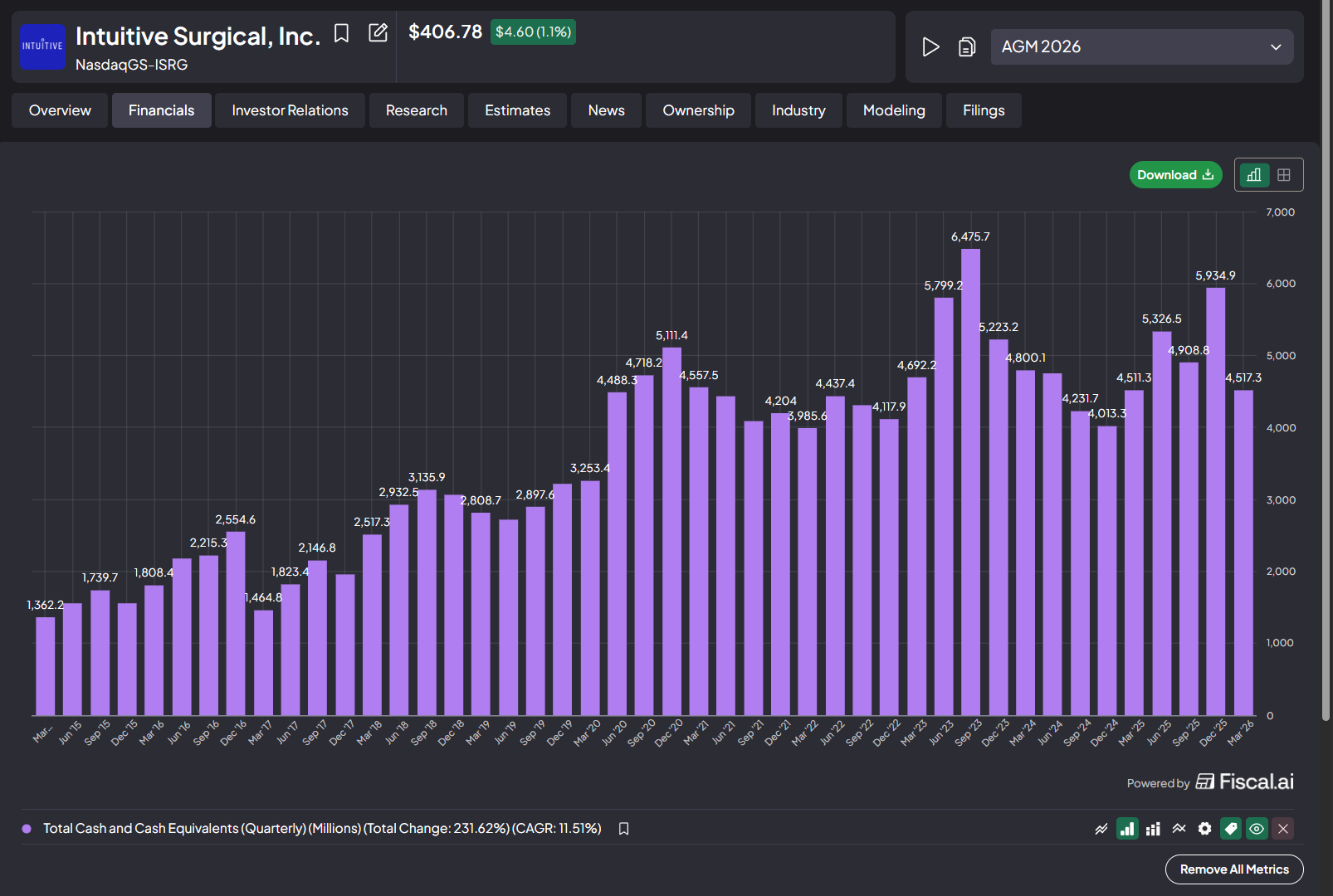

On balance sheet, Intuitive has been debt-free in the past decade! In fact, its net cash position has generally been on an uptrend as we can see below, and as of the latest quarter, is in a net cash position of ~$4.5bn.

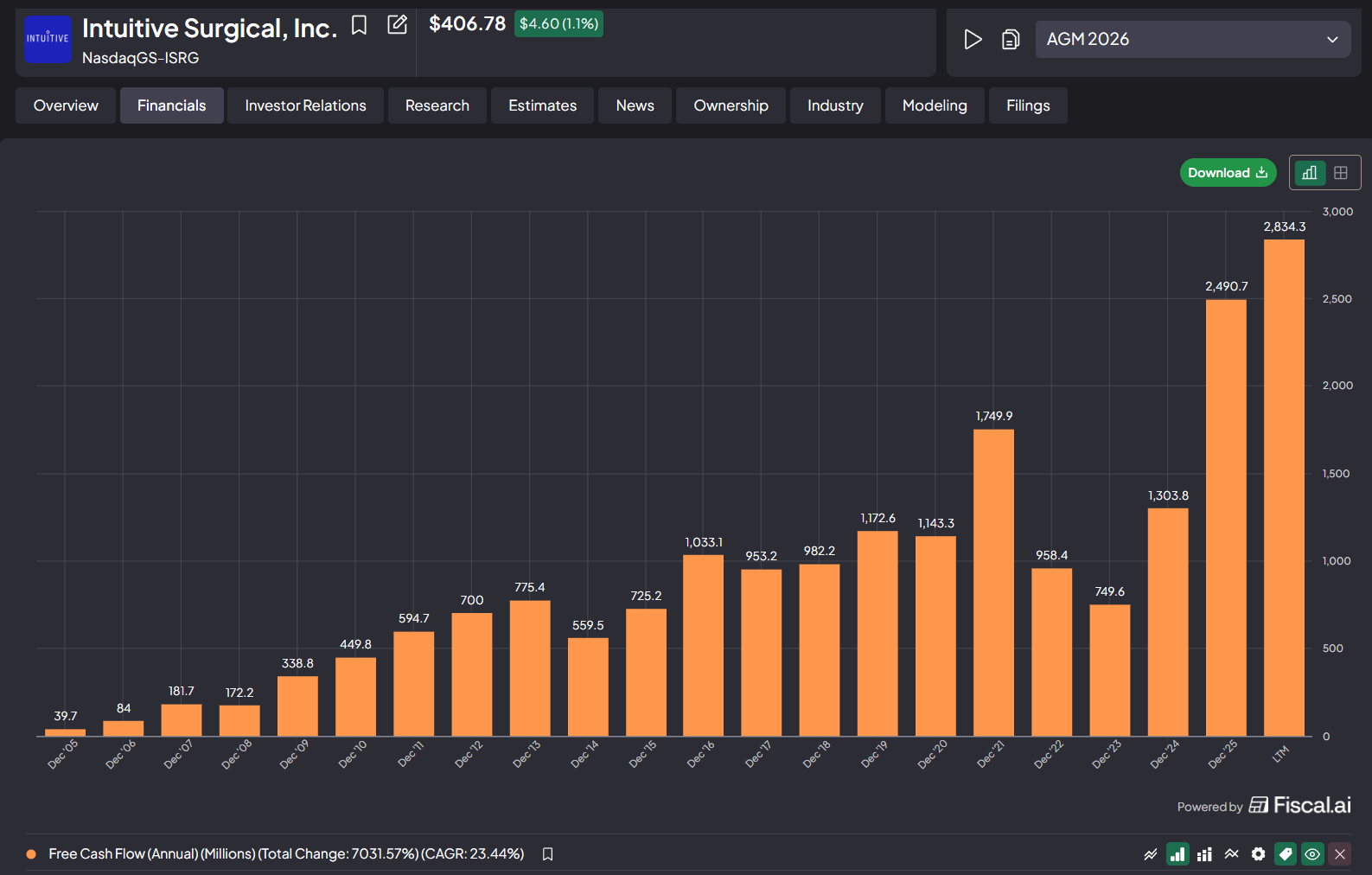

On the Cash Flow statement, Intuitive has consistently returned positive Free Cash Flows (FCF) at a CAGR of 23.4% over the last 2 decades! (see below)

Generating positive, growing FCF while funding heavy R&D shows how cash-generative the business is. Management is also disciplined about how it spends that R&D. Gary Guthart (ex-CEO, now Executive Chairman) described their approach to platform upgrades in this interview (at 41:21 mark). I quote:

With regard to pacing of upgrades, we always felt like there were three things that we tried to do to time something. We never did it by the calendar. We never set out went out and said the new model year for the Mercedes E-Class should be six years from now. We never planned that way because it was hard to predict and it didn't make any sense to me. So what we said is we need to do something that improves the technology infrastructure that gives us future growth. We need to do something that allows the customer to do something new in terms of a pure indication and we've got to futureproof something that we now learned. If we can get those three together, that's time for a platform iteration. Sometimes in the early days we're learning a lot. It could go fast. Sometimes this gets a little later. We needed a little more time. So it would be accordionlike and but each time we brought it the engineers are motivated because they're getting a new technology stack and it was ready...

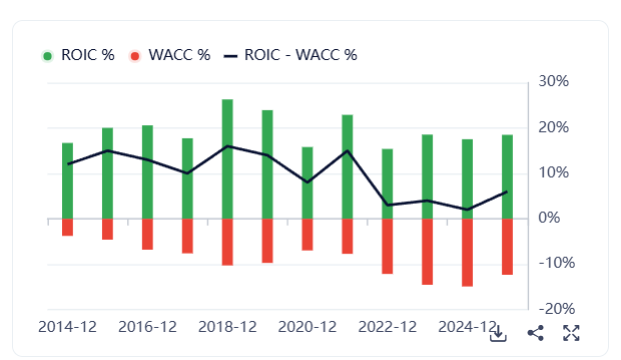

The point is that they only invest in a new platform when it genuinely expands the franchise, not on a calendar basis going through the motion. ROIC has stayed above WACC over the past decade (see below), indicating capital reinvested has historically earned more than it costs. Combined with the two-decade FCF record, I am inclined to trust management's stewardship.

Intuitive Surgical also discloses some granular numbers of their business.

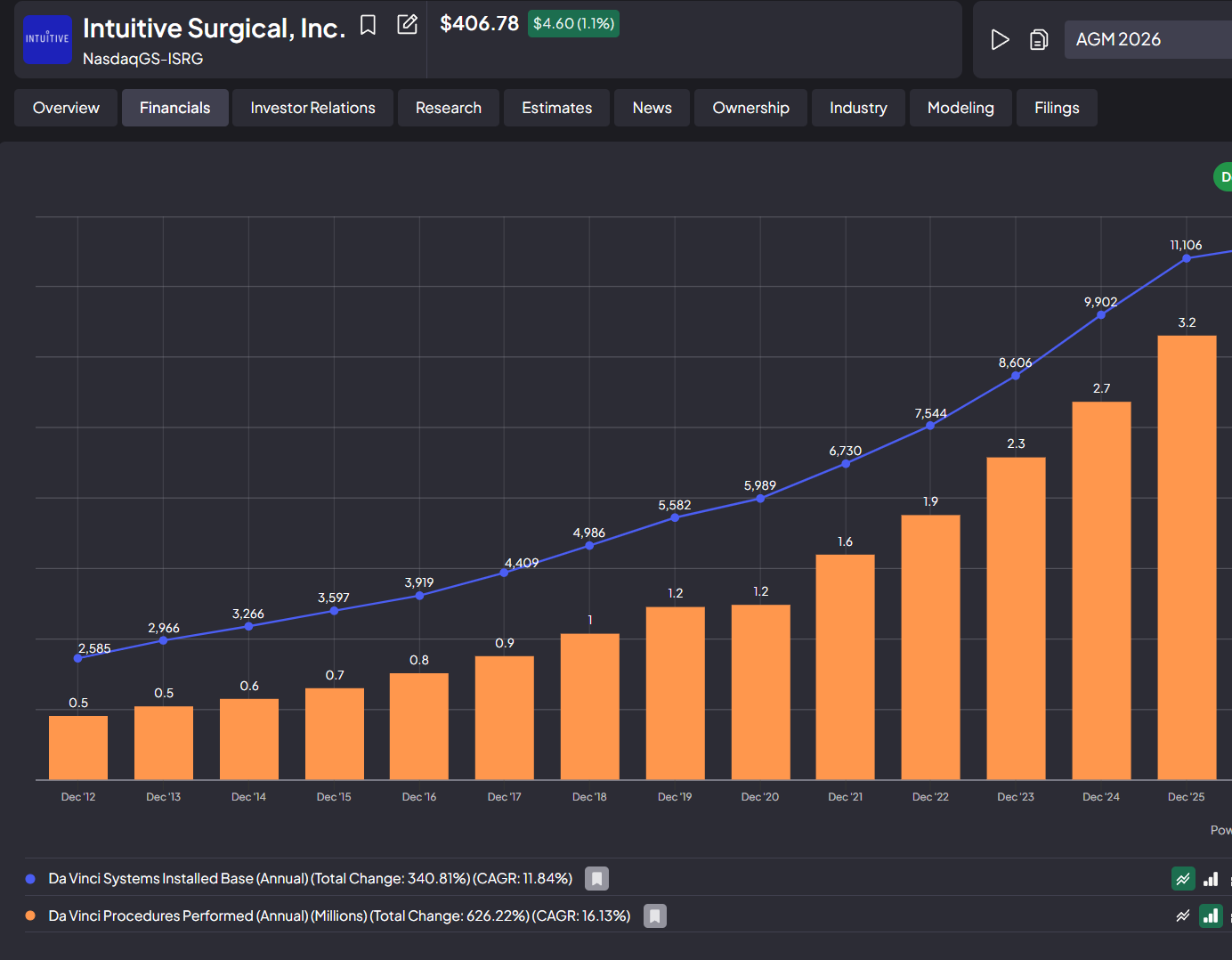

First, the da Vinci installed base has compounded at 11.84% over the past 13 years, while procedures have outpaced it at ~16%. Because procedures are growing faster than the number of systems, the average procedures done per system (what Intuitive calls "utilization,") keeps rising.

Rising utilization matters in two ways.

- For hospitals - running more cases on each robotic system spreads its high upfront cost over more procedures, improving the return on what they paid for it.

- For Intuitive - instruments are consumed per procedure, so more procedures per system means more recurring razor-blade revenue from the same installed base.

Procedural growth is the more important leading metric, because more da Vinci procedures means more surgeons are buying into robotic-assisted surgery, driving I&A revenue and feeding the data and evidence flywheel further. It is one of the main metrics I will be watching in subsequent quarterly earnings.

Management

Soul in game

Intuitive's current CEO, David Rosa, joined the company in 1996 and has spent 30 years there, rising through the product and engineering side before taking the top job in July 2025. He took over from Gary Guthart, another long-tenured insider who came up through engineering (CEO from 2010 to 2025, now executive chair). What I like is that both leaders were part of Intuitive's pioneer generation and built their careers in product and engineering, the kind of background that tends to produce a culture of organic invention rather than just M&A dealmaking.

Skin in game

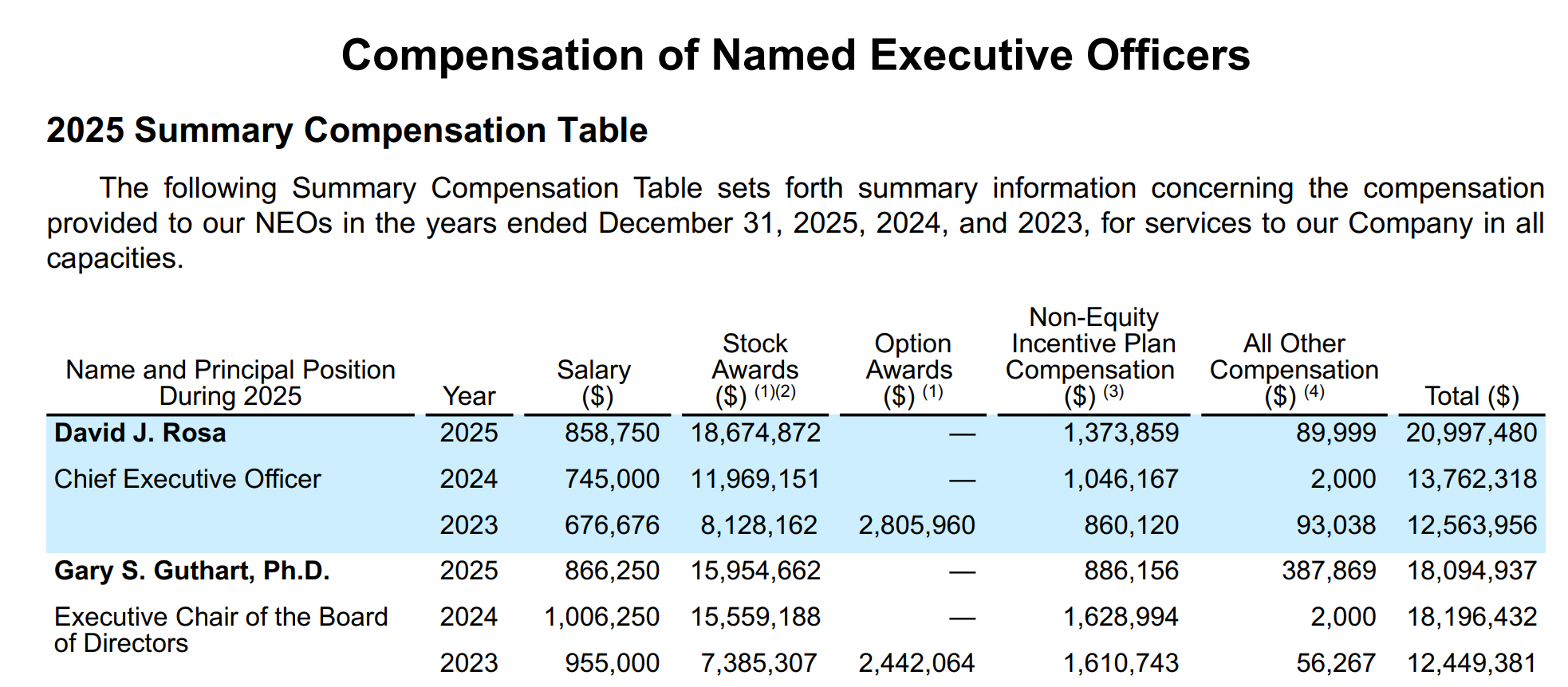

Gary and Dave Rosa's latest shareholdings are per the table below.

Neither Guthart nor Rosa appears on Forbes or Bloomberg's Billionaire list, so it is not possible for me to estimate what % of their personal networth is in the form of ISRG shares.

What we can do however, is to assess what multiple their shares' market values are compared to their fixed cash salaries, to get a sense whether they would lean closer to an 'owner' mindset or an 'operator' mindset - the former is more ideal because that means they are on the same boat as shareholders.

Per the 2 tables above, Rosa holds about $99M of ISRG shares, roughly 45x his ~$2.23M in annual cash compensation (salary plus bonus), while Guthart holds about $1.0bn, on the order of 580x his ~$1.75M of cash pay.

The bulk of each of their recent annual compensation also comes as stock rather than cash, further increasing the ratio of equity to cash. If either of them undermines the company, the hit to their equity ownership would dwarf anything they take home in fixed cash salaries, which is why I am inclined to believe they both have deep skin in the game and will continue to guide the company from an owner's perspective.

Risks(🔒Unlock with premium tier)

As with any investment, there will always be risks! In the final 3 sections, I cover

- 2 Potential risks to monitor for anyone thinking of investing in an $ISRG position

- 4 Growth catalysts and why it is still early days for Intuitive Surgical

- Valuation - Specific buy levels I'm looking to acquire shares at for my portfolio

There are 2 risks to pay attention to for prospective Intuitive shareholders that I haven't yet mentioned, firstly...