Why I Just Deployed $20,000 into This Company — and my Next Steps

Note: The following does not constitute financial advice/recommendations and is merely a journal of my own portfolio investment actions. Please remember to Do Your Own Research!

For premium subscribers who were notified by email when I executed this trade last week, you’d have noticed I tagged the transaction as a “fat pitch”. What you may not know is that this wasn’t just any fat pitch - it was the single largest transaction I’ve made in the past two years.

To fund it, I sold a portion of my equity from the tech company I currently work for - a rare move that underscores my long term conviction.

The company in question? $META.

In this piece, I’ll explain:

- Why I pulled the trigger to buy the dip

- The significance of this move, how I’m positioning my portfolio (bottom of article) and what’s next for $META

Meta reported its Q3 earnings on 29 October 2025 after market close. The next day, the stock gapped down nearly 9% at open, extending its decline to about 25% below its 52-week highs.

This was only the fourth time in the past five years Meta’s share price dipped below the 200-day Simple Moving Average (SMA) - a level that historically signals major inflection points. (See chart below.)

What Triggered the Dip

Two factors likely drove the market’s knee-jerk reaction:

- Earnings per share missed analyst estimates by 84.4%, largely due to a one-time tax hit from the “One Big Beautiful Bill” Act.

- Management commentary hinted that “capital expenditures dollar growth will be notably larger in 2026 than 2025.”

2025 Meta fears ≠ 2022 Meta fears

Some of the takes, like below, that I've seen on Fintwit draw parallels to what happened back in 2022, when Meta dipped by ~-80% and there seems to be fear of a repeat:

What these takes miss is that the conditions in 2022 were fundamentally different from today. Back then, three uncertainty factors hit Meta simultaneously:

- Apple’s App Tracking Transparency (ATT)

- TikTok’s rise amid post-pandemic normalization

- Reality Labs’ heavy cash burn

Apple's ATT Privacy Changes

ATT was the most consequential blow. In 2022, Meta’s management warned investors that the new privacy restrictions could slash annual revenue by as much as $10 billion. The change crippled deterministic ad tracking and forced Meta to rebuild its entire advertising architecture from the ground up.

In response, Meta began developing a probabilistic ad targeting model to replace the old deterministic system - an ambitious, high-risk effort with no guarantee of success.

At the time, I was personally involved in technical work related to Facebook advertising, and witnessed firsthand how ATT disrupted campaign performance and advertiser confidence. The fear and pessimism across the digital ad ecosystem on the ground were palpable.

TikTok’s Surge During the Post-Pandemic Slowdown

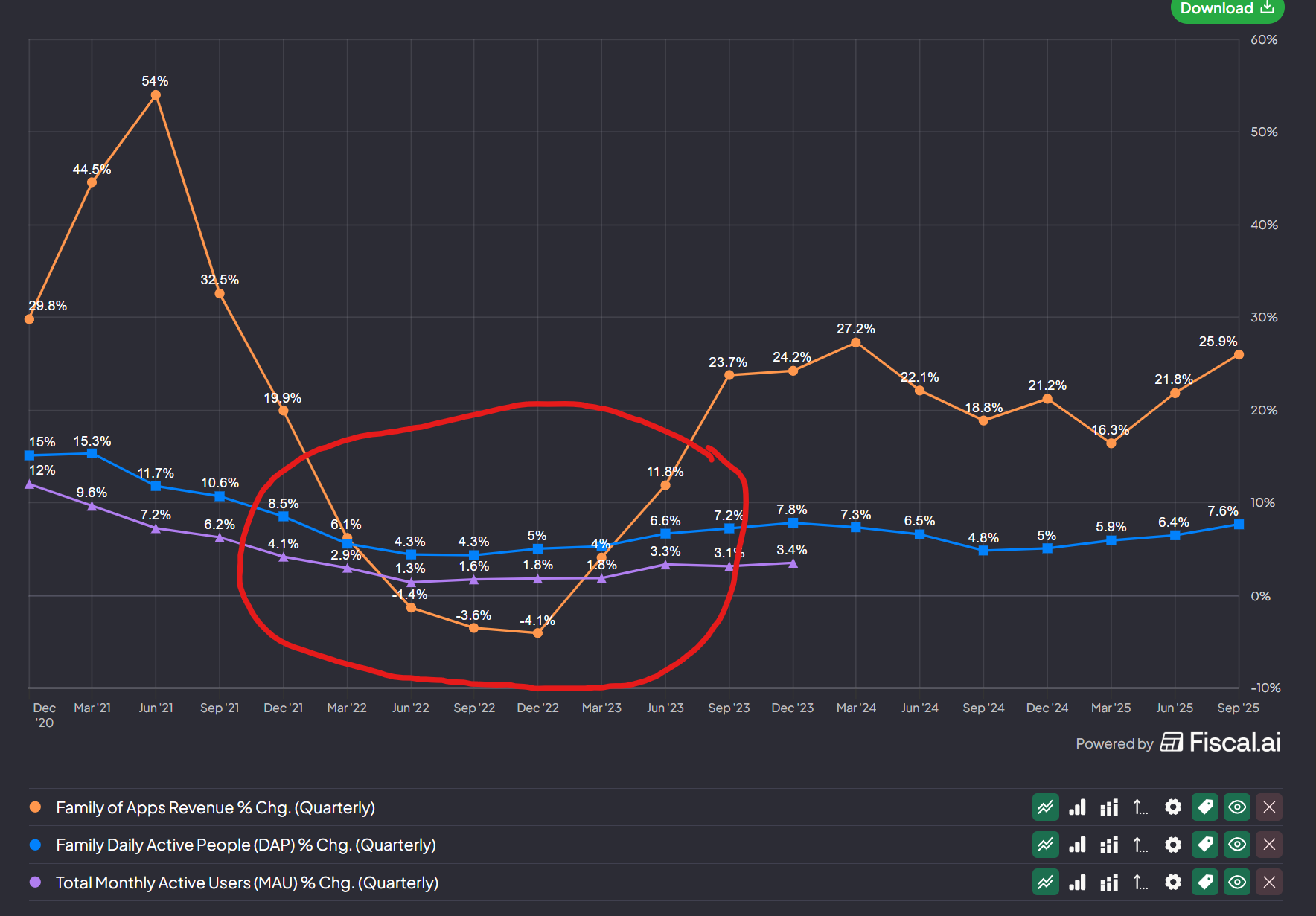

Concurrently, TikTok was exploding in growth while Meta’s engagement briefly plateaued as e-commerce activity normalized after the pandemic surge (see red-circled diagram below).

To understand how serious the TikTok threat was back then, we only need to revisit Meta management’s evasive responses to analyst questions during the Q1 2022 earnings call:

Rich Greenfield (Analyst): ... last quarter Mark had basically said the problem is not that Reels isn’t growing really quickly, but it’s that TikTok is really growing quickly as well off of a very large base. Do you think that you’re now taking share or are you still not gaining share or even losing share to TikTok competitively? And then I have a quick follow‐up on AI.

David Wehner (Meta former CFO): Yes, I don’t think I have anything on that front🤡, Rich. I think we’re pleased, obviously, with the growth that we’re seeing in Reels. Everything we see TikTok remains a very strong competitor in the market. I think it’s ‐‐ I think the third‐party data is ‐‐ we have access to some of the same data that you do so I think you can look at that. But I think they continue to perform well. And then what was your question on AI?

That exchange captured the mood perfectly: TikTok had Meta on the defensive, and the company hadn’t yet proven that Reels could stem the tide.

Reality Labs and the “Metaverse” Pivot

Finally, Reality Labs cash burn became a lightning rod for investor skepticism.

In October 2022, Altimeter Capital, one of Meta's largest shareholders, published an open letter to Mark Zuckerberg that captured the prevailing sentiment across both Wall Street and Fintwit at the time:

The conventional wisdom — press and investor — is that the core business hit a wall last fall. As a result, the team hastily pivoted the company toward the metaverse — including a surprise re-naming of the company to Meta. Worse, this skepticism seemed to be affirmed with a nearly-immediate and sizable miss in financial results and continued under-performance throughout 2022.

The takeaway was clear: Reality Labs’ spending was interpreted as a direct signal that Meta’s leadership had lost confidence in its core advertising business and was effectively “burning the boats” to pivot toward an unproven future.

To appreciate how grim sentiment was back then, consider the optics in 2022:

- On one hand, Meta was pouring capex into rebuilding its ad infrastructure post-ATT - systems that were still unproven, with Advantage+ only starting to show real promise by mid-to-late 2023.

- On the other, it was doubling down on the metaverse, a long-duration bet with little to no near-term payoff.

Put together, it’s easy to see why markets viewed Meta’s capex as reckless rather than strategic.

This convergence of three forces - ATT’s impact, TikTok’s surge, and the metaverse spending spree - drove the deepest wave of pessimism in Meta’s history, culminating in its ~80% drawdown in 2022.

Fast Forward to Today

The dynamics today are completely different.

For one, the ATT era is firmly behind us. What was once viewed as an existential threat has, in hindsight, become the greatest test of Meta’s anti-fragility. Apple’s intent with ATT was clear: to position itself as the champion of user privacy while weakening Meta’s data-driven ad engine - a move that many interpreted as both moral and competitive.

Yet, the outcome was the opposite of what Tim Cook intended. Rather than crippling Meta, ATT forced the company to evolve. Meta rebuilt its entire ad infrastructure on probabilistic foundations and what emerged was a new post-ATT paradigm, one where Meta’s reconstructed ad stack became its strongest moat. Few others could follow because they lacked the scale, data richness, or capital intensity to do the same. We only need to look at the numbers to confirm this.

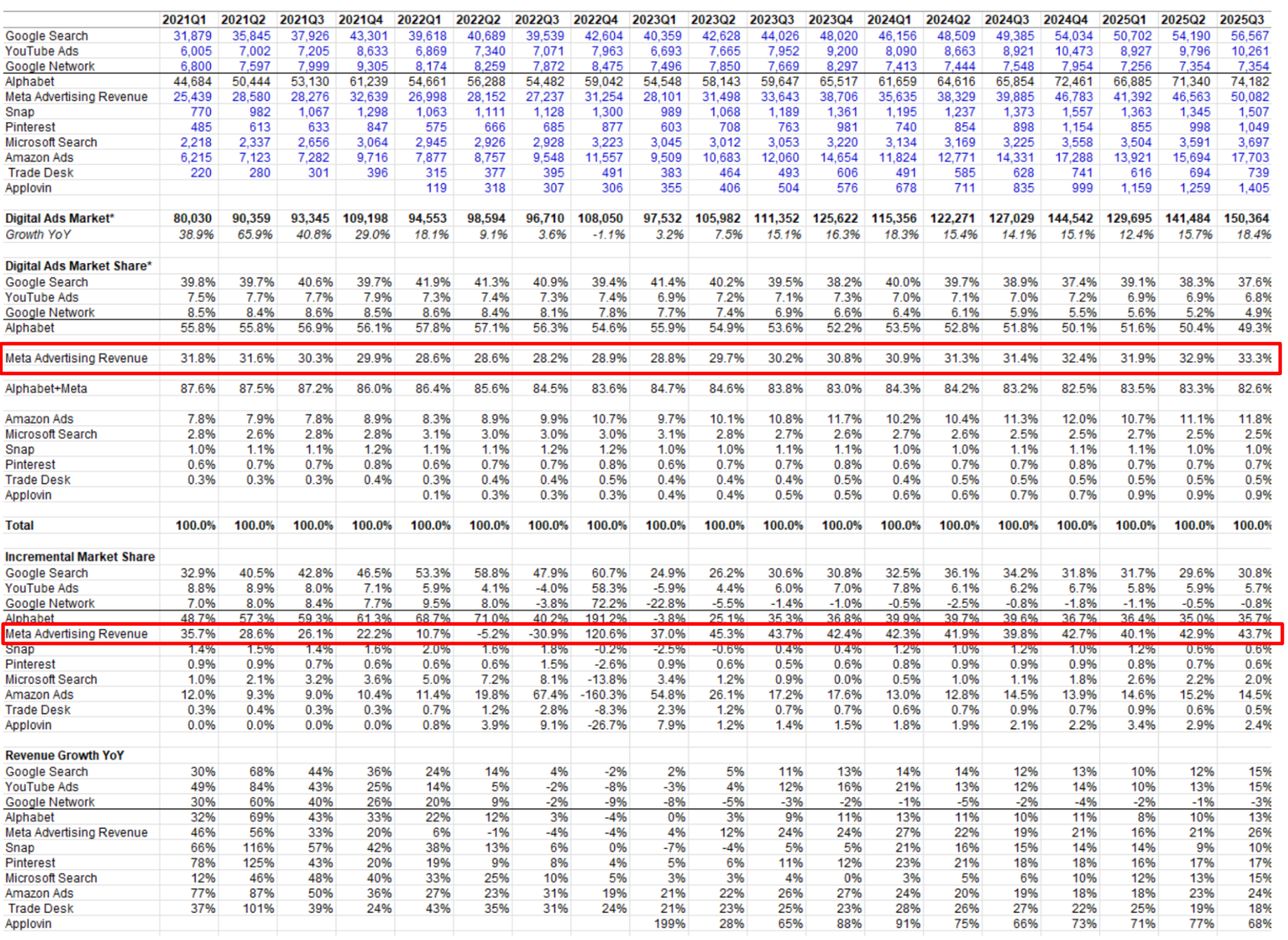

Meta’s share of the global digital advertising market (see diagram below):

- Stands at 33.3%, the second highest after Alphabet’s 49.3% as of Q3 2025.

- Has recorded the highest incremental market share gains for 11 consecutive quarters since Q1 2023 - just four months after the launch of Advantage+, the automated ad suite that marked Meta’s post-ATT comeback.

Meanwhile, Instagram also more than caught up in the race vs TikTok, reporting 3 billion MAUs as of Q3 2025, compared to TikTok's estimated 1.8billion.

GPU Fungibility

As for capex, compared to 2022, Meta now enjoys a distinct advantage through GPU fungibility, as I first mentioned in my Q3 earnings analysis.

I've broken out Meta's GPU use cases across time horizons:

Short-Medium term:

- Core ad recommendation systems for existing FoA (Instagram, Facebook and Threads)

Medium-Long term: Training and inference of Llama models, which in turn power internal applications such as:

- Advantage+ Creative suite Gen AI Tools, whose adoption grew 20% QoQ as reported in Q3 2025

- Yet to be proven:

- A fully automated Advantage+ advertising suite, where advertisers simply state their goals (for example, “I want to maximize brand reach”), and Meta automatically handles everything - creative generation, copywriting, targeting, and budget allocation

- Business AI

- Reality Labs in the form of Meta AI, ensuring performance and competitiveness against frontier models to serve as a truly ambient assistant - parsing the world through AR glasses and returning intelligent responses on the HUD display

In addition to capex fungibility, Meta also benefits from a fail-safe option: channeling excess compute to meet FoA’s insatiable demand.

From the Q3 2025 earnings call, Zuckerberg commented on the expanded capex buildout heading into 2026:

"I think it's the right strategy to aggressively front-load building capacity so that way we're prepared for the most optimistic cases. That way, if superintelligence arrives sooner, we will be ideally positioned for a generational paradigm shift and many large opportunities. If it takes longer, then we'll use the extra compute to accelerate our core business – which continues to be able to profitably use much more compute than we’ve been able to throw at it. And we’re seeing very high demand for additional compute both internally and externally. And in the worst case, we would just slow building new infrastructure for some period while we grow into what we build."

Although there’s talk of a repeat of 2022, many investors misunderstand that the current buildout is far more tightly aligned with Meta’s core business ROI and offers significantly greater flexibility in use case deployment.

Notice as well, the extra prudence in Zuckerberg's comments to "just slow building new infrastructure" - a marked contrast to 2022 as explored in the following section.

Management's Evolved Cashflow Discipline

In a recent podcast between John Collison and Susan Li (Meta CFO), Li recounted what investors told Meta's management back in 2022:

Yes. And one of the things that really stuck with me from one of those conversations is someone said, "Look, I get that you're building the future of computing and the next mobile platform and all that, and that is great, and I am glad someone wants to do it and I am rooting for you, but why should I invest in your stock today? Why don't I just wait for your phone equivalent, your scaled consumer product to come out and invest in you then, and you tell me that that's going to be years away?"

And the way that question was framed actually really stuck with me, and is the way that, frankly, now Mark and I think about this. Which is like, great, we've got a lot of these bets, and the bets are technologically exciting. People can get excited about them and the vision of the world. But as investors, they're like, "Cool, why don't I just wait for your bets to be ready to succeed before I come?" We need people to invest with us along the way. When we think about the financial outlook of the company, a large part of it is not just, okay, cool, you're building the next massive platform out here in some decades, it’s, why would you hold our shares until then? What do we need to keep delivering in terms of consolidated results?

After what they went through during the 2022 share price collapse, both Li and Zuckerberg realized they could no longer spend indiscriminately on a distant future. They needed to earn investor buy-in along the way.

As a long-term shareholder, I view this as a double-edged sword, or perhaps a yellow flag of sorts. Ideally, we do want Meta to continue investing for the long term, and optimizing capital purely to appease investors isn’t ideal.

But at the very least, this interview suggests that any capex Meta undertakes today, compared to 2022, is expected to generate both near-term and long-term returns.

Thanks to GPU fungibility, much of that investment is already delivering measurable short-to-medium term impact.

Conclusion

Meta’s renewed cashflow discipline, combined with far fewer pessimistic factors and greater GPU flexibility, gives me confidence that the sharp drop in its share price after Q3 earnings was largely a reflexive, 2022-conditioned overreaction from the market to the words "increased capex".

This is precisely why I initiated such a large top-up in $META last week. I believe there is still a gap in market understanding and analysts have not yet fully recognized how different today’s environment is compared to 2022.

I don’t have a crystal ball and can’t tell you whether I caught the bottom, or if the stock will fall further. Nor can I say how long these depressed levels will last. As Confucius said, “Those who pick the bottom have smelly fingers”

But at the price I entered, I’m more than satisfied. The stock has fallen below my pre-determined watchlist valuation buy levels, and I’m happy to wait for the market to eventually re-rate Meta.

Portfolio View & My Next Investment Steps:

Note: The following does not constitute financial advice/recommendations and is merely a journal of my own portfolio investment actions.

I've included my:

- Buy levels for $META

- Additional action plans depending on how prices move in the coming weeks

- Valuation & Entry thought process

See below: (🔒Unlock with premium tier):