A dangerous behavior is emerging in the Stock Market

In this article, I cover,

- What's happening with South Korean Memory stocks?

- An emerging dangerous behavior and why you should avoid it

- Stocks I'm looking at that have been wrongly sold off on AI concerns (🔒Unlock with premium tier)

What's happening with South Korean Memory stocks?

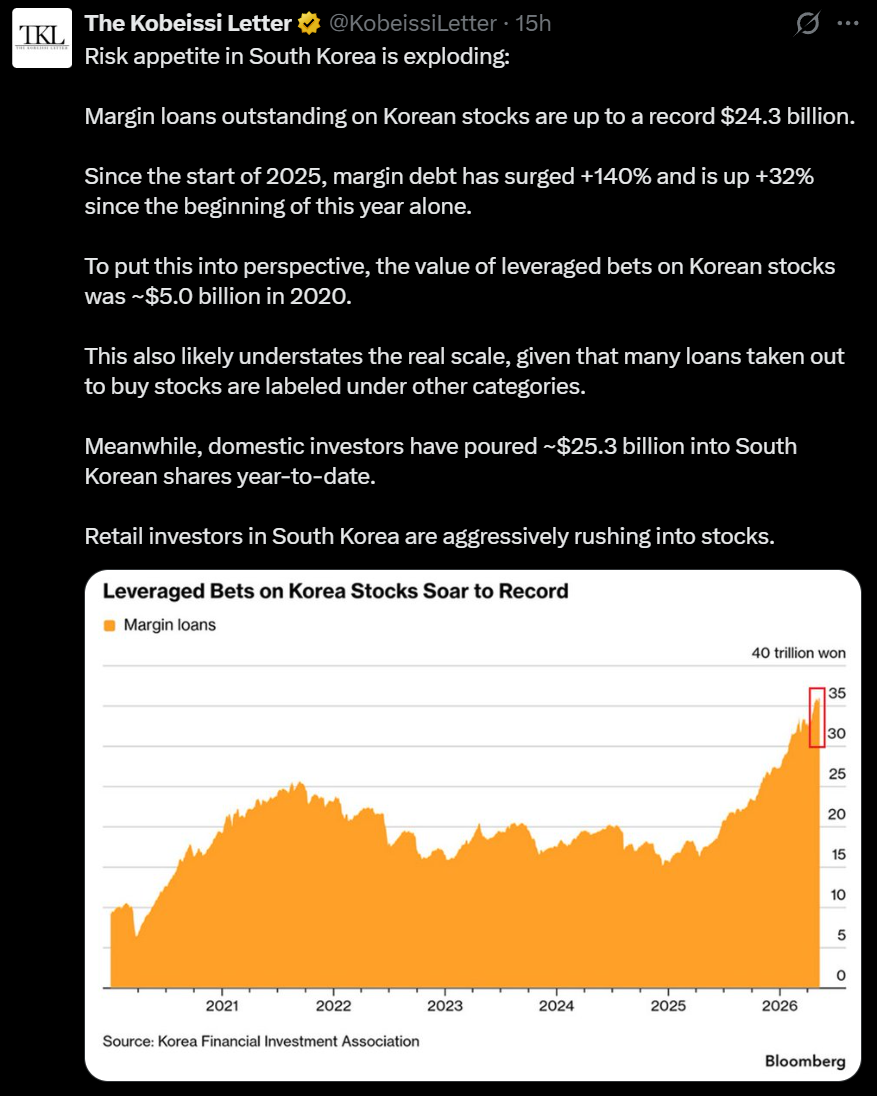

Year to date, shares of SK Hynix and Samsung Electronics have risen by over 157% and 114% respectively.

Since both stocks account for over 50% of the Korean Kodex 200, the ETF itself has risen by over 80% YTD!

This sharp rise is largely due to a memory shortage, since AI needs a lot of HBM (High Bandwidth Memory) and given that both Korean companies account for nearly 80% of global supply, their share prices have accelerated tremendously in a short span of time.

An emerging dangerous behavior and why you should avoid it

The focus of this article however, is on a dangerous behavior beginning to emerge from the South Korean market, which could spill to the rest of the world.

Here are a few snippets from this article to illustrate what I mean:

...a Seoul Metro employee in her 20s, who wrote that rather than missing out on the rally, she would “risk complete collapse,” adding that she had used 150 percent margin financing to fully leverage into stocks...

...the nation’s 10 largest brokerages — Korea Investment & Securities, Mirae Asset, Samsung, Kiwoom, NH, KB, Shinhan, Hana, Meritz and Daishin — generated a combined 600 billion won in interest income from margin lending in the first quarter of this year, up 55.9 percent from a year earlier..

As well as this tweet:

What's frightening is that even Korean seniors are getting in on the memory train, quote from this article:

investors aged 50 and older accounted for 62.3 percent of the roughly 27.2 trillion won in total margin loan balances at the top 10 brokerages as of the first quarter of this year

The real danger here

I think you get the gist of where I'm heading with in this article. The sharp rise in South Korean memory stocks is not just attracting investors, it's attracting leveraged investors. And not just a handful of them.

Record-setting amounts of margin debt are flooding into what is, at its core, a cyclical semiconductor trade. Retail investors, from the young to retirees, are piling into the same names using borrowed money, convinced that these stocks can only go up. This is textbook bubble behavior, and history tells us it rarely ends well for leveraged participants.

Two rules I have in investing

- Don't short-sell

- Don't buy on margin

Breaking these 2 rules are the only way to not only lose your portfolio but to potentially go bankrupt as well. The former because there's unlimited downside (a stock can go up infinitely with no theoretical cap, as we saw with the Roaring Kitty GameStop hedge fund debacle). And the latter, which is what I'm going to expand on, because margin amplifies not only upside but also downside.

Why buying on margin is so dangerous

Let me walk through a concrete example.

Say you want to buy shares in a hot memory stock called MemoryTech Inc, currently trading at $100 per share. For this example, let's use a common margin setup: 50% initial margin (you put up half, the broker lends the rest) and 25% maintenance margin (the minimum equity you must maintain before the broker steps in).

You have $10,000 in cash. Without margin, you buy 100 shares. With 50% margin, you buy 200 shares instead, borrowing $10,000 from the broker.

The upside looks amazing. MemoryTech rises 20% to $120:

- Position value: 200 shares × $120 = $24,000

- Your equity: $24,000 - $10,000 loan = $14,000

- Your return: +40% on your original $10,000, double the 20% you'd have made without leverage

This is the part that gets people hooked.

But watch what happens when it goes down. MemoryTech falls 20% to $80:

- Position value: 200 shares × $80 = $16,000

- Your equity: $16,000 - $10,000 loan = $6,000

- Your return: -40% on your original cash, double what you'd have lost without margin

It gets worse. MemoryTech falls 33.3% to $66.67:

- Position value: 200 shares × $66.67 = $13,334

- Your equity: $13,334 - $10,000 loan = $3,334

- Equity ratio: $3,334 / $13,334 = 25%, hitting the maintenance margin threshold

The broker then issues a margin call, demanding that you deposit additional cash into your account to bring your equity back above the 25% maintenance threshold. If you can't meet the margin call in time, the broker forcibly liquidates your shares to cover the loan. You don't get a say in when or at what price.

In fact, some brokers don't even issue a margin call first. They simply auto-liquidate your positions in real-time the moment your account breaches the maintenance threshold, giving you zero chance to react.

And here's the truly nasty part. If the stock gaps down hard overnight on a bad earnings print or a sudden shift in demand outlook, the broker liquidates at whatever price is available. If the proceeds don't fully cover the loan, you still owe the broker the difference. You can end up with zero shares AND a debt. This is how people go bankrupt!

Memory chips are cyclical, even with AI

Now, it's tempting to look at the current memory rally and think these stocks will keep going up forever. I'm not in a position to judge since memory semiconductors are not my core technical competency. But one thing I do know is that the memory chip industry is a brutally cyclical business.

Over the past three decades, the memory market has followed a remarkably consistent pattern: prices boom, manufacturers invest heavily in new capacity, supply eventually floods in, prices crash, and margins collapse. Then the whole thing starts over. Here are some examples, per this article:

- 1993-1996 PC supercycle: DRAM prices fell 51% in the first year and another 65% in the second. Memory company stock prices fell 60-80% from peak to trough, contributing to the Asian Financial Crisis.

- 2016-2018 cloud and smartphone supercycle: Micron peaked at ~$64 in May 2018 and fell to ~$28 by December 2018, a 56% decline. SK Hynix followed a similar trajectory.

- 2020-2023 COVID cycle: Micron fell from ~$98 in early 2022 to ~$49 by late 2022, a ~50% decline. SK Hynix fell similarly, posting a net margin of approximately negative 28% in 2023.

"But this time is different because of AI!" I can hear the pushback already. And yes, the AI-driven demand for HBM is significant. But if hyperscalers slow their data center buildouts for any reason, whether due to a recession or a re-rating from tokenmaxxing, memory demand could normalize much faster than the market expects.

The point is not that memory stocks will crash tomorrow, this year or next - I'm not making such a prediction, nor am I saying AI demand will falter soon. The point is buying these stocks on margin, on a parabolic upslope, is playing with fire. When the downturn eventually comes, it won't be a gentle 10% correction, since memory stock downturns historically involve 50-60% drawdowns. If you're leveraged when that happens, you won't just lose money. You'll be wiped out entirely and potentially owe your broker on top of it.

Stock Watchlist I prefer instead & Portfolio Investment Next steps

Note: The following does not constitute financial advice/recommendation and is merely a journal of my own portfolio investment watchlist and actions.

I don't chase stocks that have already gone parabolic in environments where greed is running rampant.

My preference is finding companies that...

See below: (🔒Unlock with premium tier):