Thoughts on $AXON

Over the past 8 months, $AXON has fallen ~60% from its all-time high of USD885 in August 2025 to ~USD351 recently.

Is this a falling knife or a rare buying opportunity?

Here are my quick notes on each of the events that possibly resulted in a fall in $AXON's stock price.

Prepared & Carbyne Acquisition

The market almost never likes acquisitions on high-valuation stocks, and tends to find reasons to punish them. The question I always ask is whether said acquisitions are net-accretive to the business long-term. It's tempting to look at the stock price and conclude these are bad M&A, but remember, the stock price is not the business.

Strategically, both acquisitions serve a singular purpose: disrupting the 911 dispatch layer and upending Motorola Solutions' stranglehold (~75% market share in public safety communications).

Axon isn't trying to compete head-on with Motorola's legacy radio infrastructure. It's flanking from a completely different angle. Carbyne adds cloud-native call routing and handling whilst Prepared brings AI-powered real-time transcription and translation of 911 calls across 33 languages. Together, these form "Axon 911": a platform connecting the caller, dispatcher, and responding officer with real-time intelligence from the first moment of an emergency through to case resolution.

The key insight is that rather than replacing the radio, Axon is building an intelligent layer on top of the 911 workflow. Once agencies adopt Axon 911 for call intake, that data feeds directly into body cameras, Evidence.com, and Draft One on the back end, creating a closed-loop ecosystem from call to courtroom. That is a flywheel Motorola simply does not have.

The combined ~USD1.4B price tag is not small, but the strategic logic of owning the entire public safety workflow from 911 call through to prosecution is compelling. And for these reasons, I'm comfortable with management's decision here and find that the stock price's correction with regards to these acquisitions are merely short-term minded.

Claude Disruption

One of the advantages I have in my field as a solutions engineer is a front-row seat to this technology. I use Claude pretty much everyday, from coding to solutioning to building assets. Fun fact: I currently rank 4th in my org in terms of Claude token usage and I think I'm in a position to confidently conclude whether Claude's cowork plugins, or Claude in general, can truly disrupt $AXON.

I can conclusively say that Claude is not a panacea to replace mission-critical vertically integrated companies like $AXON, for 3 reasons:

1. Proprietary data moat. $AXON holds proprietary data in Evidence.com that is irreplicable by even the smartest AI models, or whatever AGI could potentially emerge in 5-10 years. Evidence.com is the largest cloud-based digital evidence management platform in law enforcement, housing terabytes upon terabytes of body camera footage, case files, chain-of-custody records, and redacted evidence across thousands of agencies. What the AI can't "see" has no threat of being disrupted, because it has no access to train on it. This data is siloed behind strict compliance frameworks (CJIS, FedRAMP) and is not sitting on the open internet waiting to be scraped by AI agents.

2. Hallucination is a non-starter for law enforcement. The issue of hallucination will not go away, even with upcoming improvements like Claude's Mythos model. This is inherent to the nature of how transformer models work: they are probabilistic next-token predictors, not deterministic truth engines. Law enforcement agencies deal in evidence that must hold up in court. A single hallucinated detail in a police report or evidence summary could compromise a prosecution or, worse, implicate an innocent person. This is not a risk any agency will take, no matter how good the underlying model gets and hence, I don't see how Claude can fully substitute the law enforcement work flows without $AXON's involvement.

3. Institutional inertia is massively underestimated. Even at my company, which is likely one of the most AI-native in the world, we're still figuring out how best to use AI optimally (despite it having been nearly 4 years since the advent of ChatGPT). If a technologically forward company like mine still hasn't figured things out after so long, I'm dead sure dinosaur, slow-moving law enforcement agencies would take far, far longer to adopt Claude and replace whatever internal processes they have. Crucially, is it really in their interest, in terms of time and focus, to be building and maintaining law enforcement software? These are agencies that are chronically understaffed and underfunded. Their job is to protect communities, not to become software development shops. That is precisely why $AXON's value proposition, a turnkey integrated platform, is so sticky.

The AI Bubble Hedge?

Here's an angle I find increasingly interesting: at the rate things are going, $AXON may well be the best hedge in my portfolio against an AI bubble bursting.

Since $AXON has now been lumped in with every other SaaS company in this "SaaSpocalypse" meltdown, the market is effectively pricing it as though AI disruption is an existential threat to its business. But consider the inverse. If AI turns out not to be the panacea for everything it's expected to be, and the bubble pops, $AXON should actually re-rate upward. Why? Because the entire bear case around Claude and AI disrupting Axon's law enforcement workflows would evaporate overnight, while the underlying business (body cameras, TASERs, Evidence.com) would continue growing regardless.

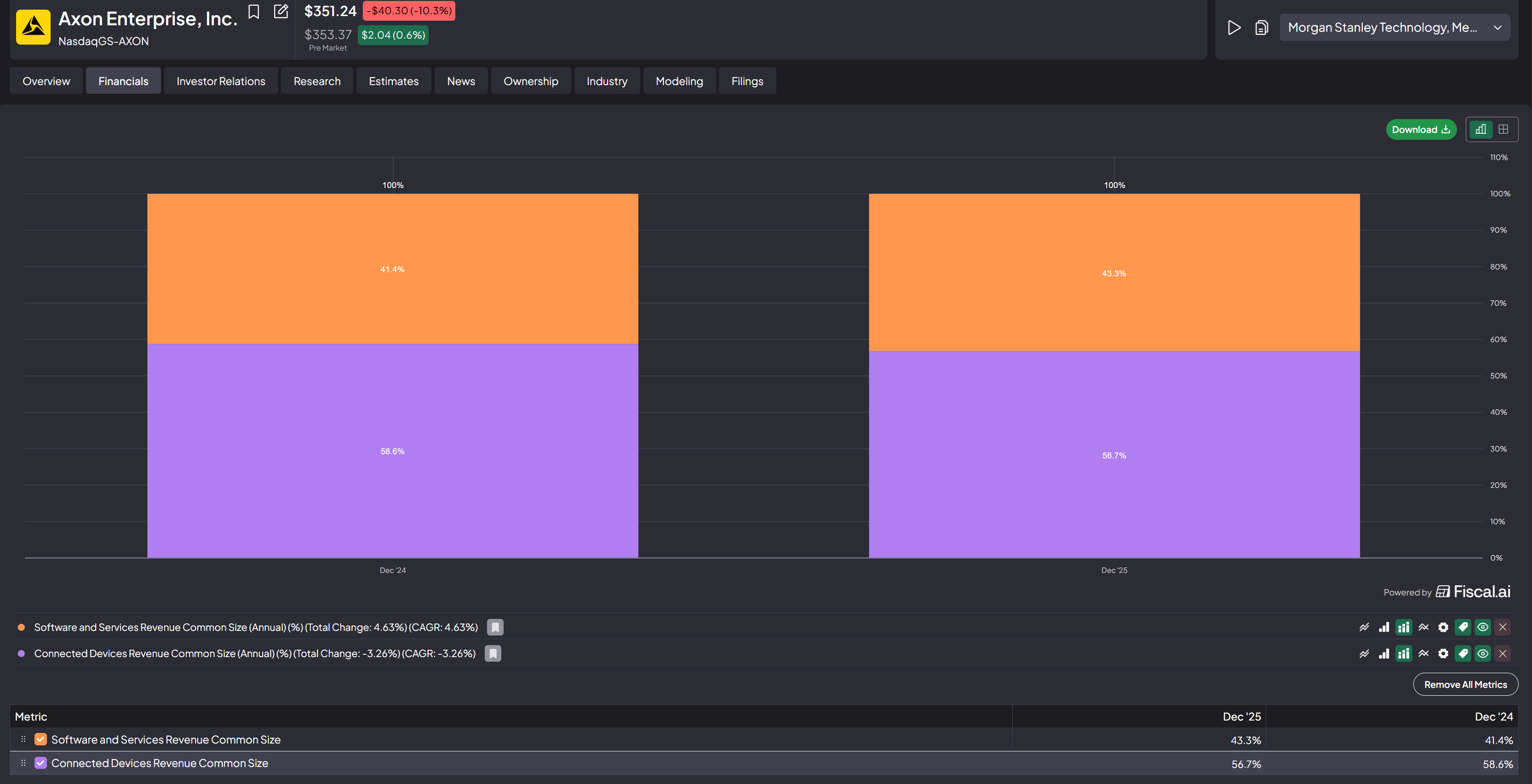

Also, let's not forget something the market seems to be conveniently ignoring: $AXON isn't even a pure software company. In FY2025, Connected Devices (TASERs, body cameras, in-car cameras, drones, counter-drone systems) contributed approximately 57% of total revenue, with Software & Services making up the remaining 43%. More than half of Axon's revenues are tied to proprietary hardware and connected devices that no AI model is going to replace. You can't download a TASER. You can't prompt-engineer a body camera. It's almost comical that the stock is being sold off alongside pure-play SaaS names when the majority of its revenue is physical, proprietary hardware (see diagram below).

My Next Investment Steps & Valuation buy levels:

Note: The following does not constitute financial advice/recommendation and is merely a journal of my own portfolio investment actions.

Given the way $AXON is moving in line with the prevailing SaaSpocalypse narrative, my next portfolio moves are to...