The Quiet Compounder Stock everyone missed

Note: This article originates from my Stock Research Vault. At the end of this article, I share my valuation buy levels and next potential moves with this company for premium subscribers.

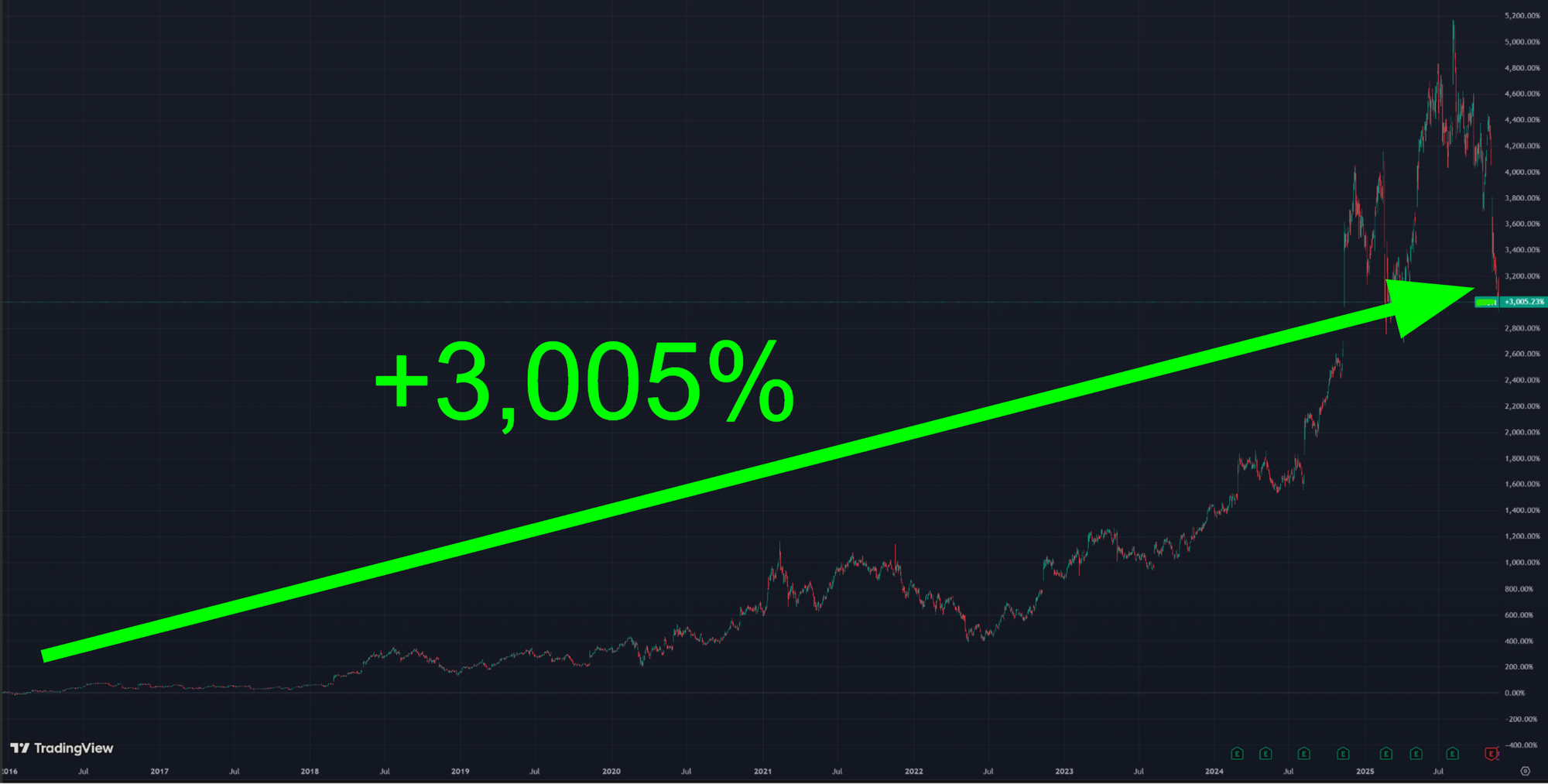

Over the past 10 years, the S&P500’s biggest winners have followed a predictable pattern tied to the AI buildout:

1) Nvidia’s +23,671%

2) AMD +10,358%

3) ???? +3,005%

4) Arista Networks +2,750%

5) Broadcom +2,510%

*Above as of market close on 14th Nov 2025

To most investors, this leaderboard looks exactly as expected.

But within the top five best performers of the entire S&P500 lies one more company that breaks the pattern in an unexpected way. It quietly compounded +3,005% over the same period, placing 3rd overall, while touching neither the AI GPU boom nor the data center infrastructure wave. It is also not part of the Magnificent 7.

Most investors could not name it and some even mistake it for another oil and gas firm. It earns far fewer headlines than Big Tech, yet has outpaced every other high-profile name of the past decade by dominating a niche market with almost no real competition.

Today, the stock sits ~40 percent below its all time highs, creating an attractive window for consideration.

That company is none other than Axon Enterprise (Ticker: AXON).

In this article, I present a deep-dive on this company, including:

- Origins of Axon & its Mission

- Business Model & Economic Moat

- Industry & Competitive Positioning

- Financials

- Management

- Risks

- Growth Catalysts: Why it's still early days

- Valuation Buy Levels: Recent sell-off - Opportunity or Trap?

- My Next Portfolio Moves

Origins of Axon & its Mission

The history matters because it reveals the founder’s enduring resolve as he overcame successive setbacks over a 30 year journey to pursue a mission he was profoundly committed to, building Axon into what it is today.

The Failed Invention (1991 - 1994)

In 1991, following the death of two close friends who were killed by lethal firearms in a road rage incident, a young 21 yr old Rick Smith was determined to find a less-lethal alternative.

However, the idea didn't turn into action until 1993, when Rick's mother found herself looking for protection following a rise in local crime. She was terrified of using a lethal firearm, so Rick suggested she buy a Taser - a device he had heard of from the Rodney King news. But when she visited the gun store, she was told the Taser was illegal for civilians.

Rick couldn't understand why a less-lethal tool was banned while lethal guns were readily available. He became obsessed with finding the answer.

After moving back to Arizona later that year, Rick made it his mission to find out more about the Taser. Since the internet didn't exist yet, he couldn't just Google the answer. Instead, he would regularly head to the ASU Law Library to manually scour through patent indexes. Spending hours scrolling through microfilm, he found what he was looking for - a recent patent filed by an ex-NASA scientist named Jack Cover.

Crucially, the patent wasn't just for the old illegal Taser. Cover had filed a patent for a new Taser version that used compressed air propellant. Rick realized at that point that Cover was on to something interesting and decided to reach out.

When Rick cold-called Cover and finally met him, he learnt why Cover’s original device had failed to take off as a commercial product. The first Taser models used gunpowder as a propellant, which caused the Bureau of Alcohol, Tobacco and Firearms (ATF) to classify it as a firearm, in the same legal bucket as a sawed-off shotgun. This meant that the Taser required federal tax stamps, registration, and other requirements - ironically making a less-lethal self-defense tool harder to buy than lethal weapons.

Rick identified the classification as the core bottleneck and began working with Cover to redesign the Taser to use compressed air instead of gunpowder - thus began the founding of the company known as Air Taser Inc. in September 1993.

Because the ATF required a real working model before granting commercial approval, the duo set out to build a prototype, at one point using bicycle tire valves from a local hardware store to create the air propellant system. Within just 30 days, they had a working prototype and mailed it to the ATF.

What followed was incredible. The ATF received the prototype on November 15th that year and within 15 days, gave approval for the newly-designed Taser to begin commercial sales. The usual approval typically took 6 - 18 months, so how was this possible?

It turned out that the chief of ATF firearms technology was a guy named Ed Owen. Earlier in 1976, Ed had signed an order outlawing the original gunpowder Taser. He felt terrible for the earlier prohibition, knowing he indirectly caused the death of thousands of Americans who died from lethal firearms.

Ed was quoted as saying:

“Rick, I don't get to make the laws. I got to interpret the laws. And under the way the laws are written, that thing was a firearm.”

And so when a guilt-ridden Ed saw the new prototype, he approved it much faster than usual. This is an underrated point - when you build something that truly benefits the world or saves lives, the stars usually align to help.

The ATF's signing removed the Taser's firearm designation and with that, Air Taser Inc launched their first commercially approved product - The Air Taser 34000.

The Dark Iterative Years (1995 -1999)

Early progress was slowed because Cover had previously licensed Taser IP to a rival called Tasertron. Under that agreement, Air Taser Inc was legally blocked from selling to North American law enforcement until February 1998.

Desperate for sales outside the US, Rick travelled to Prague in 1995 to demo the Air Taser 34000 to the Czech National Police Academy. During the demo, the Air Taser failed to incapacitate all seven volunteers, an outcome Rick found deeply embarrassing.

It turned out that this first version of the Taser only had enough power to hit the pain nerves, not the motor nerves required to truly incapacitate humans. This confirmed why police at that time did not trust less-lethal weapons: pure "pain compliance" tools (like pepper spray or early stun guns) often failed against determined attackers or those high on adrenaline and drugs.

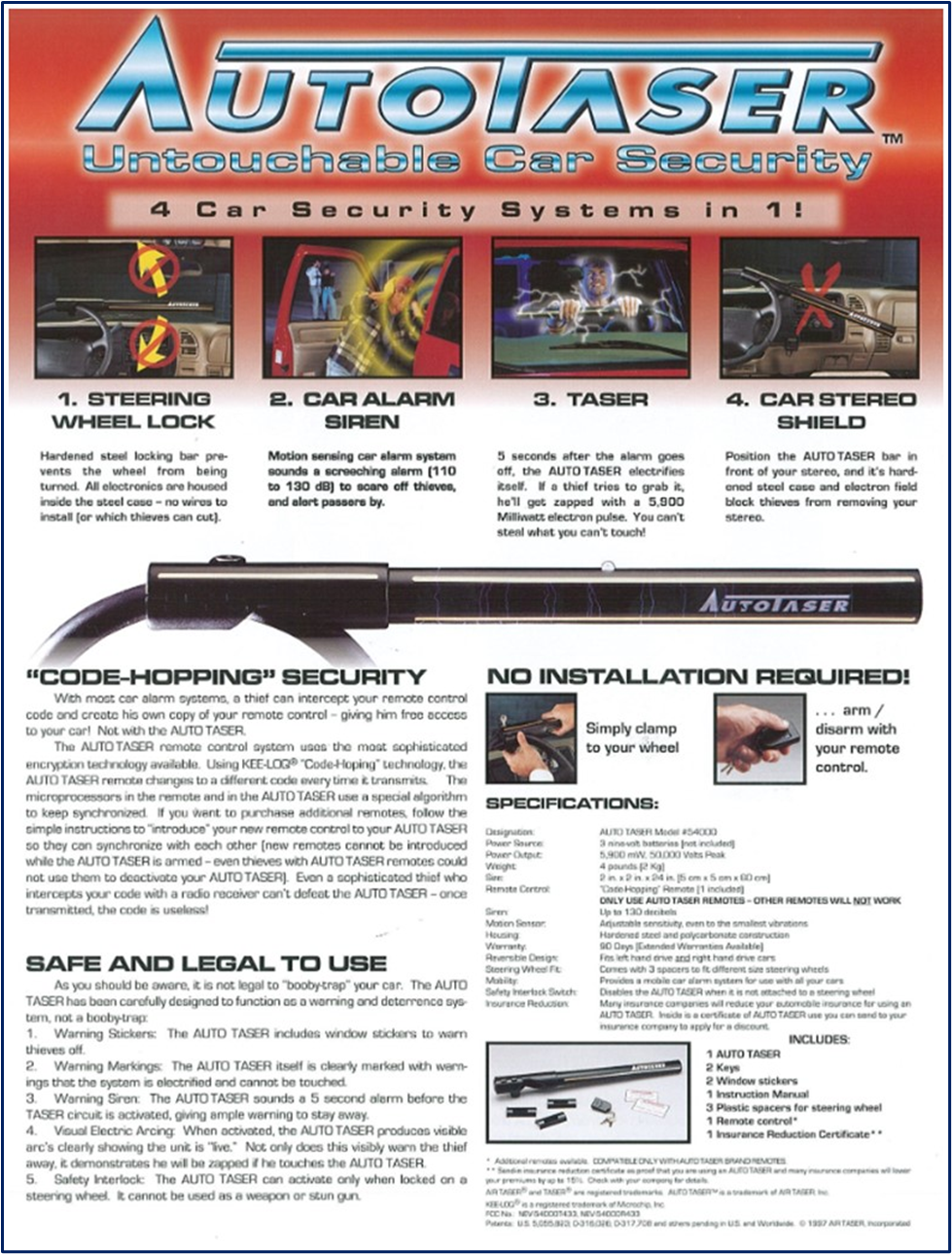

With the company bleeding money due to the Tasertron restrictions and the failed Prague demo, Rick pivoted to a consumer focus, hoping to make quick cash with the Auto Taser to stay afloat. Showcased at CES Las Vegas in 1997, this was an electrified anti-theft steering wheel lock.

The gimmicky product drew massive media attention but failed to sell, and was discontinued by 1999. Following the Auto Taser flop, Rick recounted two critical lessons he learnt:

Generating excitement and actually selling a product are fundamentally different things.

Chasing a "quick buck" without solving a problem that truly matters rarely works for me.

By 1999, the company was on death’s door. Following the failure of the Auto Taser and slow traction of the Air Taser 34000, they were nearly insolvent.

The business survived only on a final lifeline: a loan from Rick’s father, who bet the last of his retirement savings ($500,000), and angel investor Bruce Culver, who matched the funds. The Smith family had bet everything they had.

Following the expiry of the Tasertron 1998 restrictions, the company changed its name from Air Taser Inc. to TASER International, marking a fresh start and a strategic pivot from consumer gadgets to professional police gear.

They then used their remaining capital to develop one final "Hail Mary"- The Advanced Taser M26.

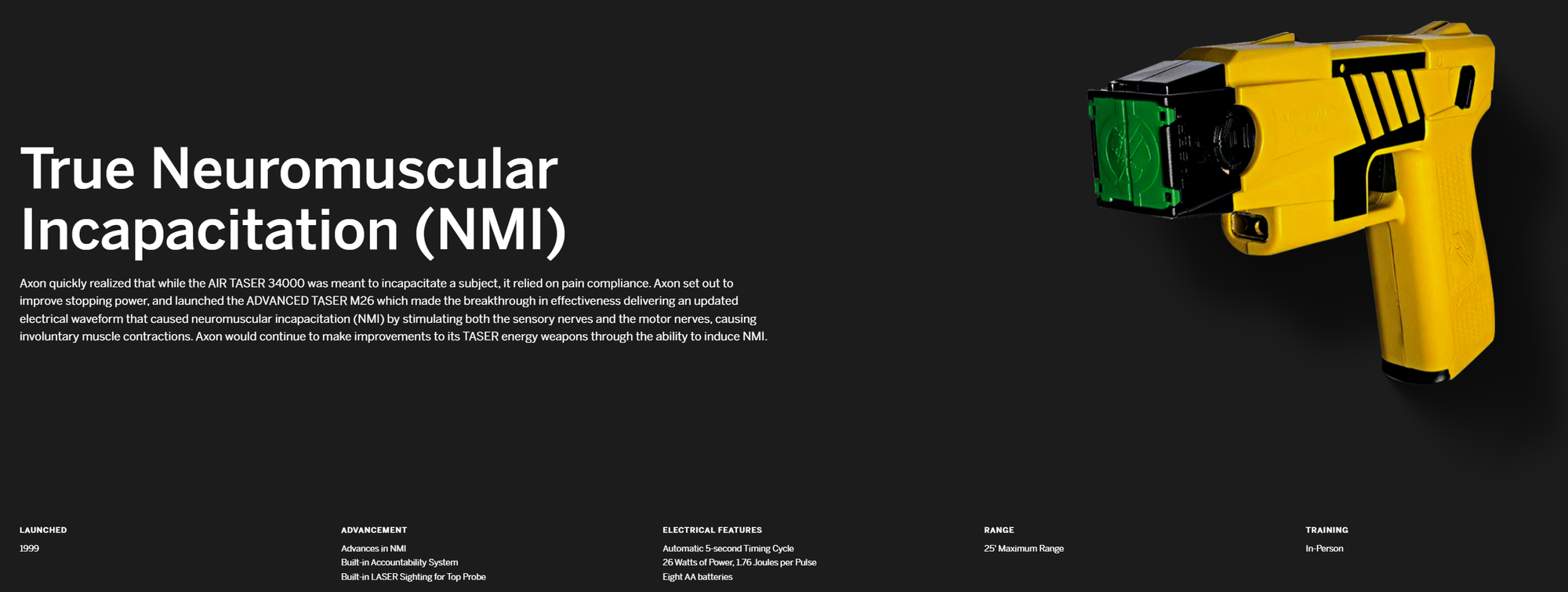

"All-In" Bet & Turning Point (1999 - 2000)

Launched in late 1999, the M26 was the first device to utilize Neuromuscular Incapacitation (NMI) technology. Unlike the failed Prague model that relied on pain, the M26 used higher amperage to override the motor nervous system, physically locking up a subject’s muscles regardless of their pain tolerance.

This was the breakthrough Rick needed.

In the early 2000s, Rick recounts going around police stations and betting officers $100 that they would not be able to withstand the M26's electrocution. Every one of the officers were knocked down but got right back up once the taser was removed. The officers had never seen anything like that and word started spreading about the M26's effectiveness.

Needless to say, the Taser witnessed incredible growth following these guerilla demonstrations and revenues nearly tripled every year for a few years.

A Series of (Un)fortunate events (2001)

Riding the momentum of the M26’s initial success, the company went public on the NASDAQ in May 2001 under the ticker TASR.

The IPO timing was paradoxically lucky. The recent "Dot-com bubble" collapse meant investors had stopped throwing money at internet vaporware and were desperate for companies with real, physical products and actual revenue growth.

Then, September 11 happened.

Airline security became an urgent national priority. United Airlines announced it would equip its aircraft with Tasers. The logic was simple: Tasers could incapacitate a threat without puncturing aircraft fuselages and risking decompression. Other airlines quickly followed suit.

Turnaround and The Golden Era (2001 - 2005)

Fueled by the M26's adoption and the post-9/11 security boom, TASER International ended 2001 profitable for the first time, generating roughly $6.8 million in revenue.

In 2003, the company solidified its dominance by acquiring its old rival, Tasertron, for roughly $1 million, finally consolidating the core patents and becoming the undisputed leader in conducted energy weapons.

Later that year, they released the X26, a revolutionary device that offered stronger NMI (incapacitation) delivery in a form factor 60% smaller than its predecessor the M26. The X26's compactness made it feasible for officers to carry the Taser on their belts every day, and it soon became standard issue for law enforcement nationwide.

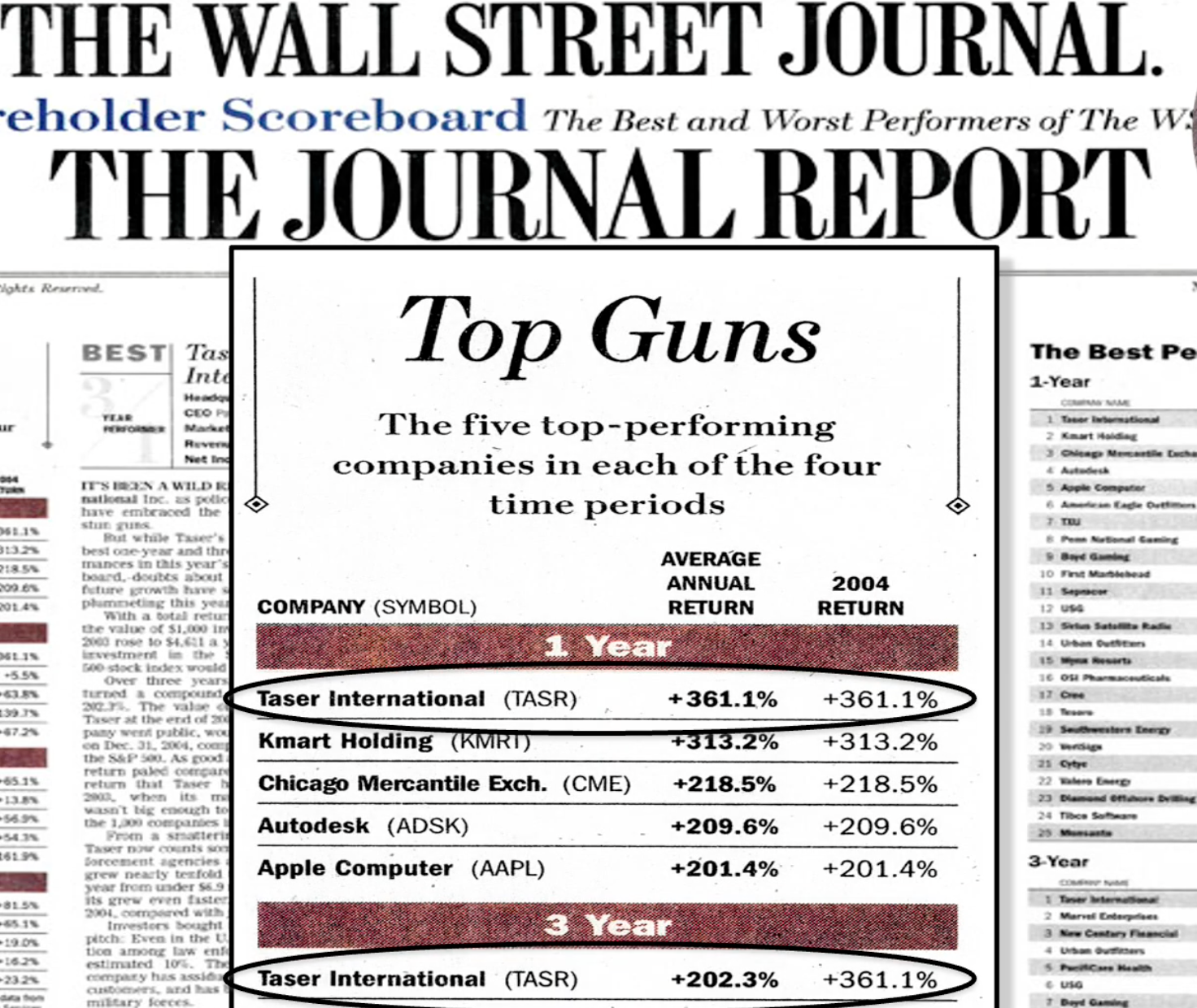

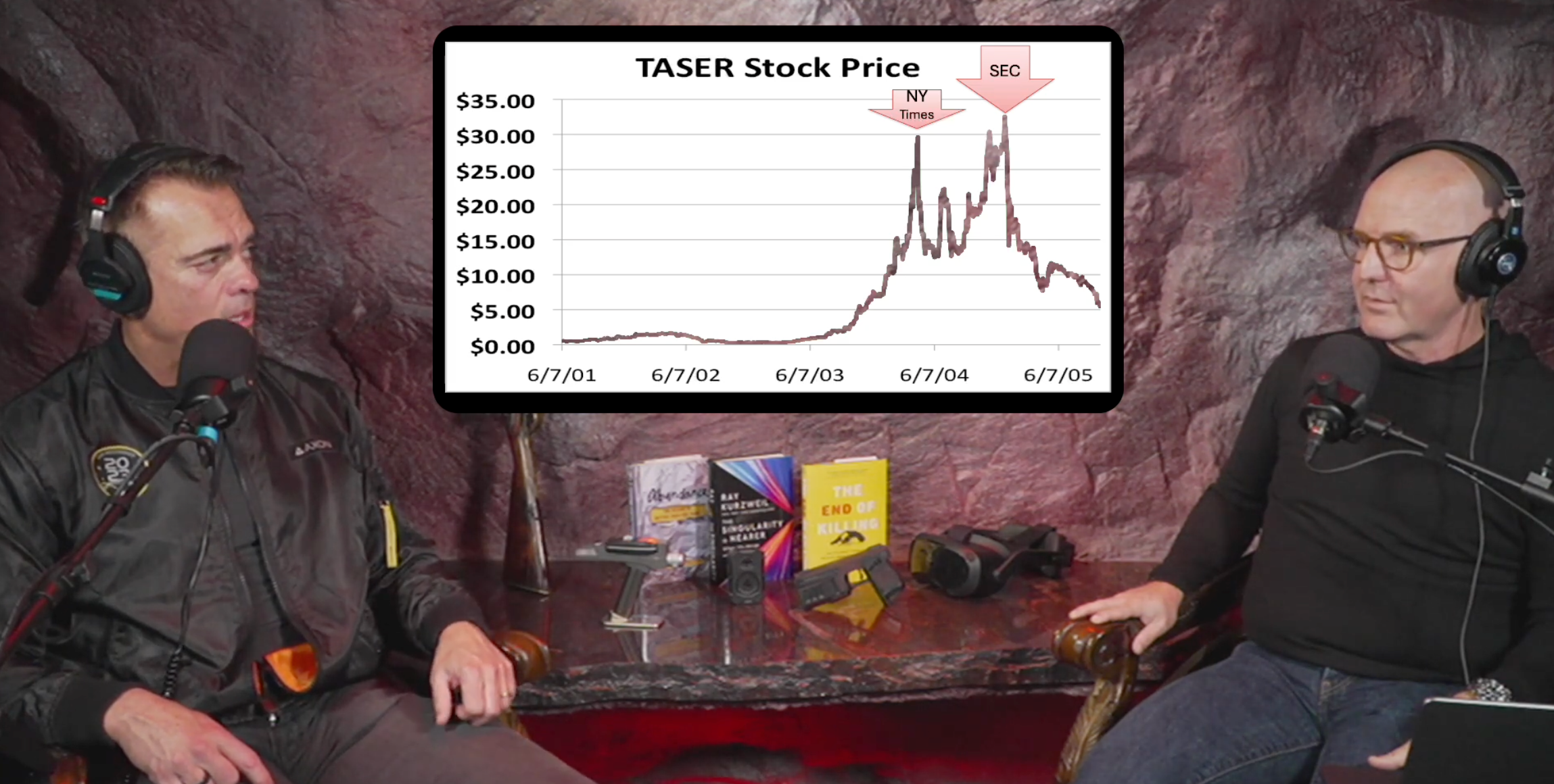

At one point in 2005, the Wall Street Journal even reported Taser International as the best performing stock over a 3 and 1 year period (see pics below).

The Crisis: Trial by Media & The SEC (2005)

As the X26 began to scale, negative news media flooded the scene, accusing the Taser of having poor safety standards. In 2005, as scrutiny intensified, the SEC opened an inquiry into Taser International.

The investigation had catastrophic consequences. The stock price collapsed, and sales plummeted as police departments became hesitant to place orders with a company under federal scrutiny.

Against his lawyers' advice, Rick went full “transparency mode.” He proactively walked into the SEC investigators' office, offering to answer every question they had to clarify the safety data backing the Taser. This unconventional move paid off, cutting years off the investigation. More importantly, it revealed a bit of Rick's character - a no-nonsense founder who believed so strongly in his mission that he had the integrity to share his dealings transparently and the technical chops to back it up.

Litigation Pivot: Birth of Body Cams (2006–2009)

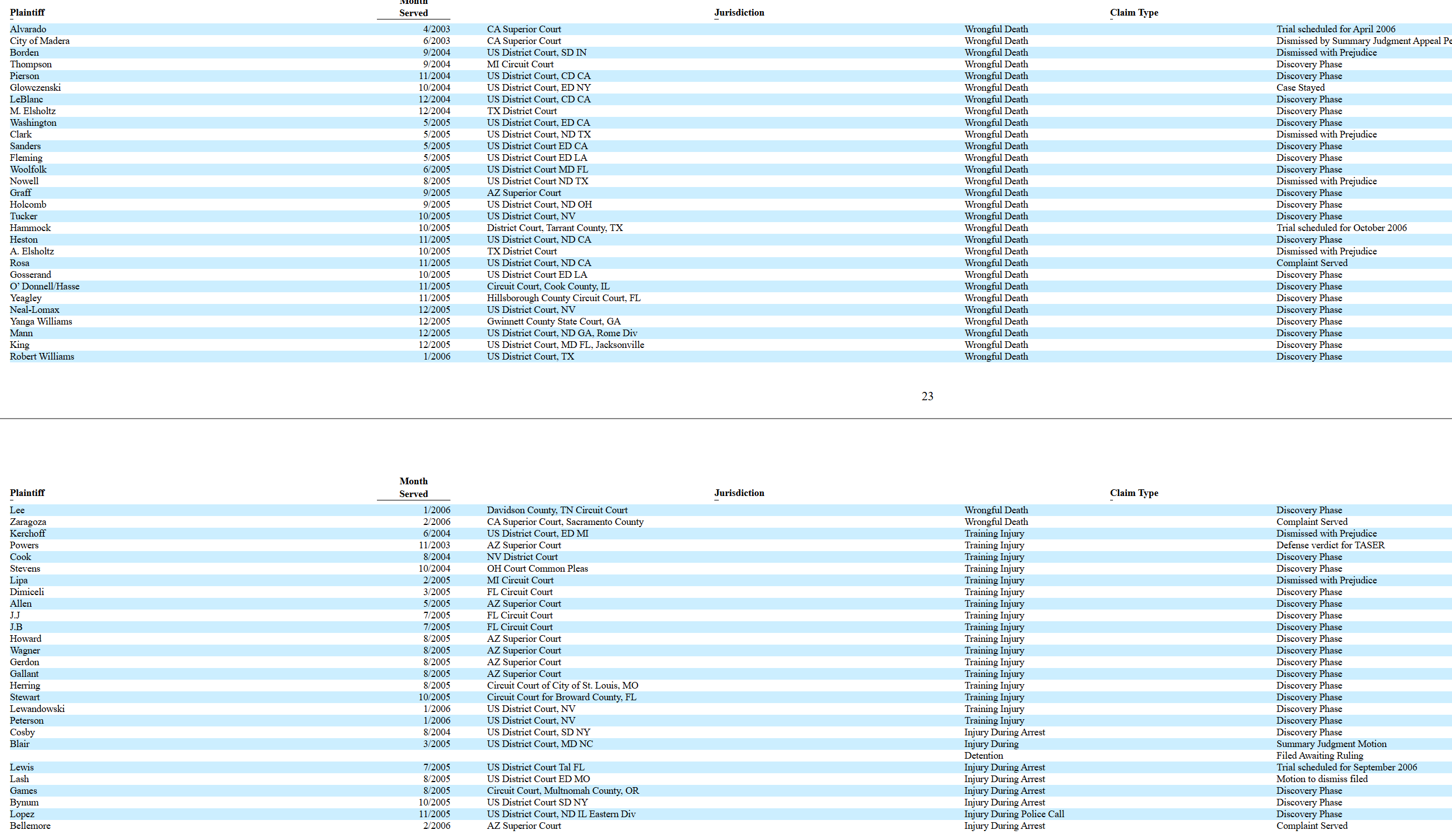

Although Rick managed to clear the SEC investigation, once the story of a federal investigation hit, the company became flooded with wrongful-death lawsuits and shareholder litigation (See screenshot below of the 49 Product Liability Litigation cases they were facing)

Net income collapsed 95%, falling from $18.9 million in 2004 to roughly $1.1 million in 2005, largely due to spiraling legal and insurance costs.

Through the litigation crisis, Rick realized that the company could not protect officers, users, or itself without some form of objective video evidence of what actually happened during Taser encounters.

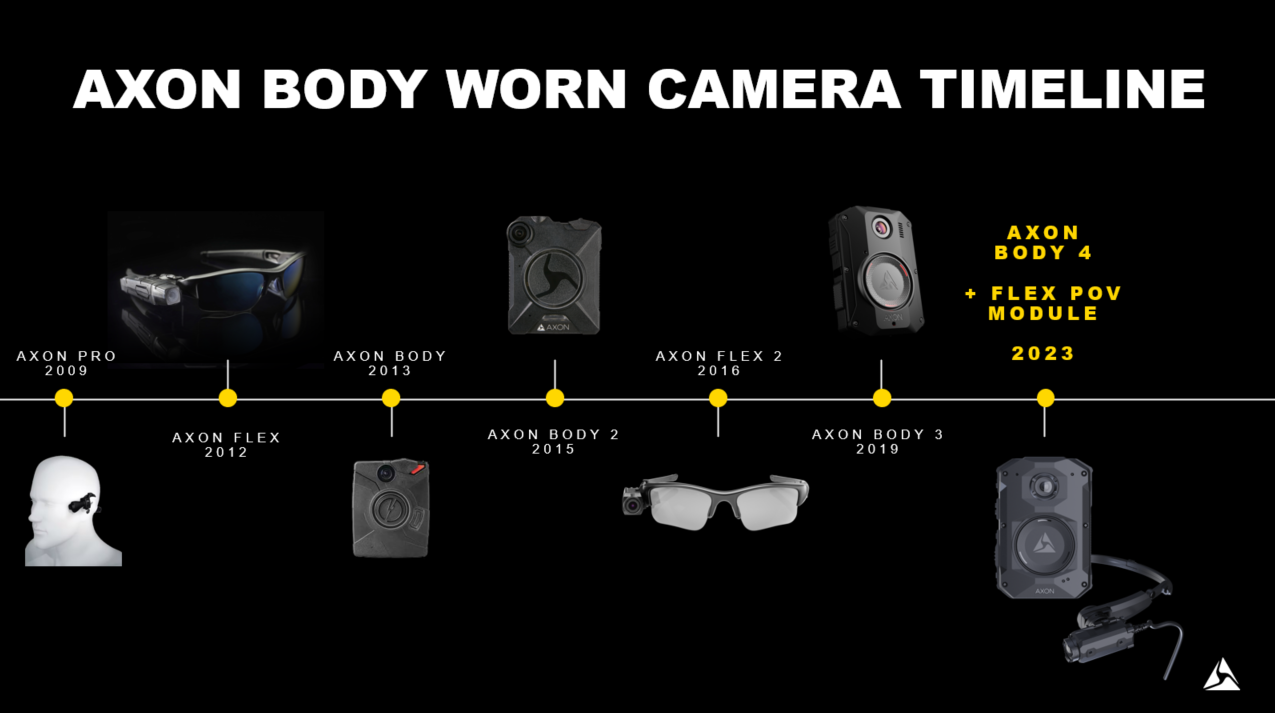

The company's first solution was the TASER Cam, introduced in late 2005. It was a grip-mounted camera that activated automatically when the Taser's safety was disengaged, creating a basic evidentiary record of use-of-force events. That early concept later evolved into Axon Pro, the company’s first head-mounted body camera and a predecessor to the latest Axon Body 4.

This pivot became the foundation of the modern Axon. Cameras did not just reduce litigation risk, they created the first frontline sensor that generated digital evidence. Once Axon had a stream of video coming off devices, it opened the door to something far bigger than hardware.

Building the Cloud ecosystem (2009 - 2017)

In 2009, Axon launched Evidence.com, the cloud-based platform that would redefine the business:

- Body Cameras rapidly expanded the installed base of connected evidence- generating devices

- Evidence.com monetized evidence storage, retrieval, and management through multi-year SaaS contracts with extremely high retention

Rick later revealed in a recent podcast that the strategy was inspired by Apple’s iPod and iTunes. Body cameras were the iPod and Evidence.com was the system that created lasting value like the iTunes.

An Inflection point: TASER International to Axon (2017)

On April 5, 2017, TASER International officially changed its name to Axon Enterprise, signaling a shift from a weapons-centric identity to a broader technology and solutions company.

The rebrand launched alongside one of the boldest go to market plays in Axon’s history. On the same day, the company offered every police officer in the United States a free Axon Body 2 camera plus one year of unlimited Evidence.com storage, aiming to accelerate adoption and seed a large base of future subscribers.

Later that year, Axon introduced the Officer Safety Plan (OSP), its first full platform subscription. OSP bundled Tasers, body cameras, Evidence.com, and scheduled hardware upgrades into one predictable per officer fee, marking the company’s formal transition into a subscription-driven model.

Moonshot & Platform goals (2017 - Today)

Rick Smith has consistently emphasized that Axon’s long-term mission is to reduce violence and protect lives. In 2022, the company formalized this into a public Moonshot goal:

“Cut gun-related deaths between police and the public by 50 percent by 2033.”

This Moonshot acts as Axon’s strategic north star. It guides product direction, capital allocation, and long-term planning. It is also deeply personal for Rick, tying directly back to the event that sparked Axon’s founding: the loss of two close friends to gun violence in 1991.

As part of this broader mission, Axon has expanded beyond tools on an officer’s duty belt (Tasers and body cameras) into robotics, real-time operations, and next generation emergency communications.

Collectively, these moves push Axon towards a true public safety platform that spans the entire emergency lifecycle, from the first 911 call all the way through real-time response, evidence management, and case resolution.

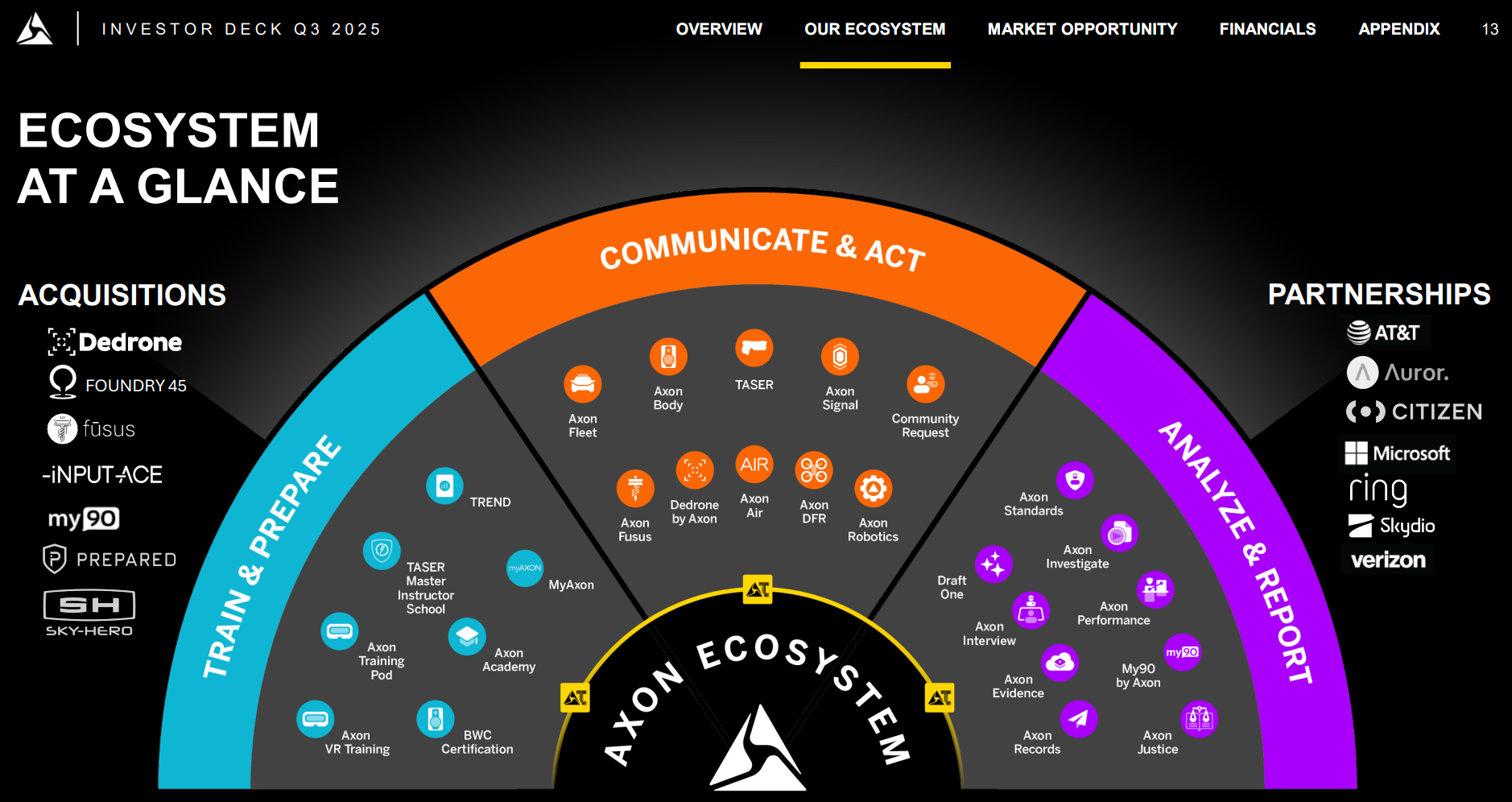

Like a platform company, Axon integrates with a growing ecosystem of partners, exposing APIs that allow agencies and software vendors to build on its core stack. This model resembles how Apple opened its iOS ecosystem to developers, and is one reason why some analysts have begun referring to Axon as the “Apple of public safety”.

Business Model & Economic Moat

1. The Entry Point: Mission-Critical Devices

Nearly every Axon customer relationship starts with a device: a TASER, an Axon Body camera, an in car Fleet system, or a drone deployed as a first responder. These devices are intentionally designed to rely on Axon’s cloud platform to deliver their full value.

For example:

• Taser sends logs and metadata directly to Evidence.com

• Axon Body cameras auto-record when a Taser is drawn and upload the footage to Evidence.com

• Drones stream live video into Axon Respond for real time coordination

2. The Flywheel: Subscription Software & Cloud Evidence

Once a device is deployed, most agencies subscribe to Evidence.com to store and manage data in the cloud.

Evidence.com is arguably the strongest lock in moat in public safety. Once a department’s video, reports, and casework are embedded inside Axon’s ecosystem, switching becomes nearly impossible. Migrating petabytes of video, logs, transcripts, chain of custody records, and legal documents is not a realistic option for any real world police agency. Fun fact: Rick Smith once mentioned that Axon stores more video footage than YouTube and Netflix combined!

The user base also extends far beyond frontline officers and includes prosecutors, defense attorneys, enterprise security teams, civil defense, EMS, and more.

As a testament to Evidence.com’s importance in Axon’s value chain, software now represents 43% of the company’s revenue and is growing faster than devices. In effect, Axon has built the public safety equivalent of Amazon Web Services. Instead of hosting compute workloads, it hosts the procedural memory of law enforcement.

3. Contracts and Revenue Design

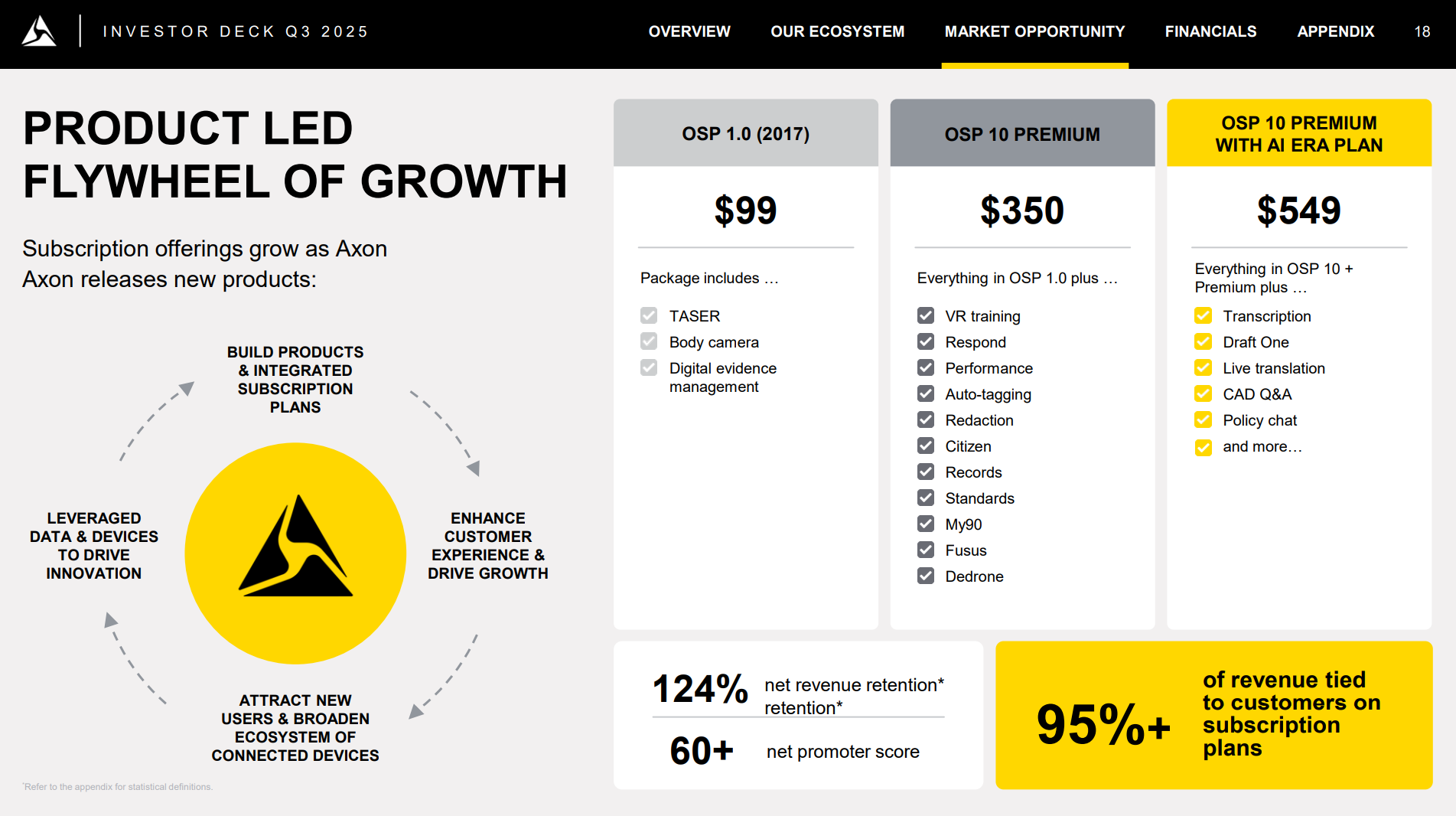

Axon’s flagship bundle is the Officer Safety Plan (OSP) - a multi year subscription that packages everything a law enforcement agency needs. Each plan combines:

- TASER device

- Axon Body camera

- Automatic replacement on every upgrade cycle

- Evidence.com

- VR Training

- and more (see below OSP diagram)

Unlike traditional hardware companies that rely on unpredictable replacement cycles, Axon bakes the hardware (Taser, Bodycam, etc.) replacement schedule directly into OSP contracts, converting what used to be episodic hardware sales into a predictable refresh cadence, streamlining Axon's production and R&D efforts.

In October 2024, Axon layered the AI Era Plan on top of OSP, adding new AI driven capabilities such as:

- Draft One: Automated report writing.

- Axon Assistant: Voice commands and real-time translation on Axon Body cameras

- Auto-Transcribe: Transcription of body-worn camera recorded audio.

- Smart Detection: Allows investigators to quickly jump to video moments when people appear to speed up evidence review

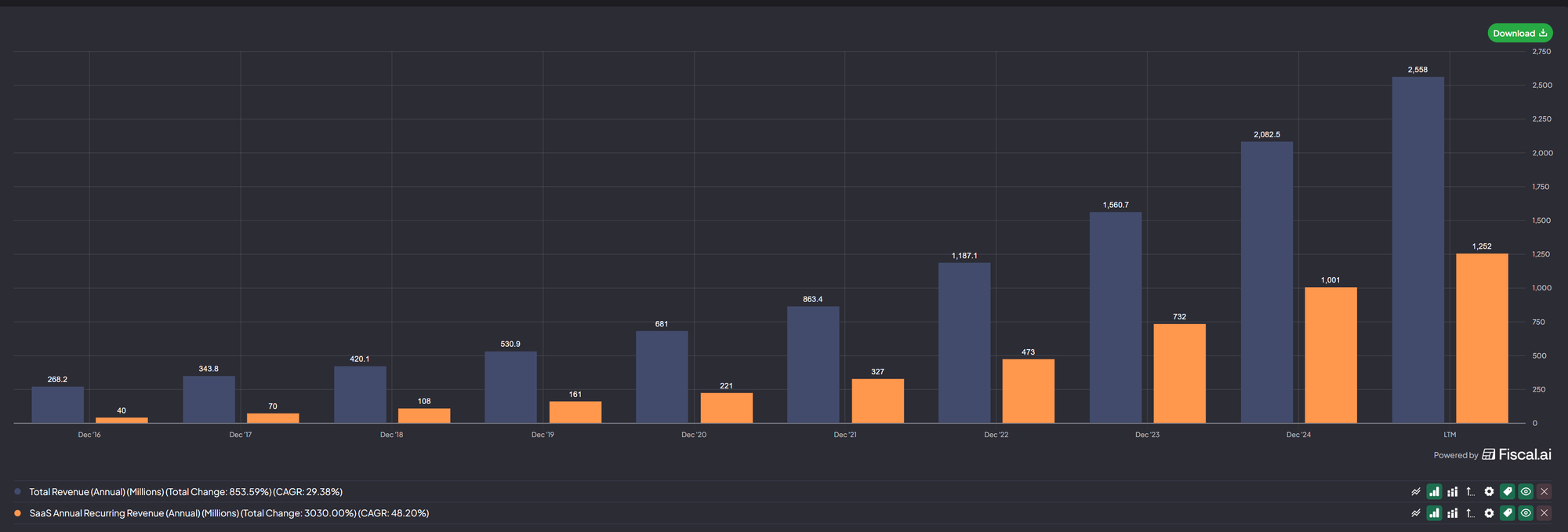

The OSP bundle transformed Axon’s business model into predictable recurring revenue, locking agencies into long term SaaS-like contracts. Between 2016 to 2025, Annual Recurring Revenue as a % of Total Revenue grew from 15% to 49% (see diagram below).

As of the latest quarter, the company has over 11.4 billion dollars in future contracted revenue, growing ~39% year over year (diagram below).

4. Land, Expand, Automate

Axon’s go-to-market philosophy is simple: win the first hardware deployment, then expand into everything else. A typical trajectory looks like this:

- Department buys TASERs or Body cameras

- Subscribes to Evidence.com for storage and chain-of-custody

- Upsells into Records, Fleet, Respond, and AI software

- Integrates drones and real-time operations

- Moves dispatch workflows and 911 stack into Axon’s cloud

The company's Net Revenue Retention (NRR) is evidence of this expansion dynamic - between 2019 to 2025, NRR rose from 121% to 124%.

This is no longer a “razor and blade” model. It is a data gravity model: every new workflow pulled into Axon's cloud ecosystem increases retention, ARPU, and strengthens the long-term economic moat.

Industry & Competitive Positioning

To understand Axon's competitive position in the Public Safety industry, we must examine each layer of its integrated stack.

Less-lethal weapons

The North American Non-Lethal Weapons Market is expected to reach US$ 4.41 billion by 2033 from US$ 2.86 billion in 2024, with a CAGR of 4.92% from 2025 to 2033.

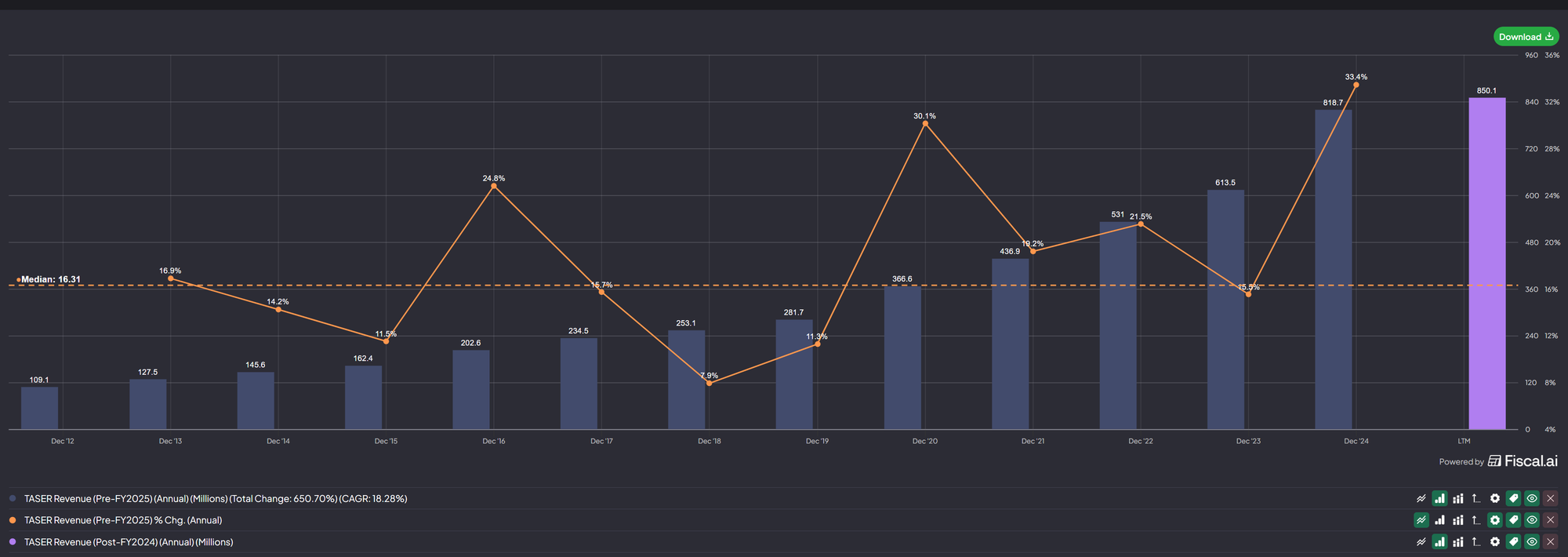

Axon's Taser segment represents 33% of company revenues. It generated USD850M in LTM revenue which comes up to about ~30% share of the USA Non-lethal market. As of 2024, the Taser business is growing at a rapid pace of over +33% YoY(see diagram below).

Within the Conducted Energy Weapon (CEW) category, Taser is estimated to have a whopping monopolistic share of 95%!

The scale gap between Axon and its next two competitors is substantial:

- Byrna Technologies, which sells less-lethal launchers (disables via chemical irritant and kinetic impact) to both civilians and agencies, reported about USD111M million LTM revenue

- Wrap Technologies, maker of the Bola Wrap restraint device, did roughly USD2.9M LTM revenue

Beyond these players, there are other non-lethal tools like stun guns, pepper sprays, and rubber bullet launchers from companies such as SABRE and PepperBall Technologies. Their market shares are materially smaller relative to Axon and the competitors listed above.

Numbers aside, Rick Smith’s early failures in Prague with the Air Taser 34000 model highlighted a fundamental truth about non-lethal weapons. The vast majority of competing products rely on pain compliance or physical entanglement. The Bola Wrap, for example, restrains rather than incapacitates. Chemical irritants depend on pain response. These mechanisms are unreliable against highly motivated individuals, suspects experiencing adrenaline spikes, or persons under the influence of drugs.

Taser’s neuromuscular incapacitation is point-and-shoot and designed to override voluntary muscle control. That reliability is the unique proposition of Axon’s Taser product.

A telling anecdote comes from UK police reporting that in 92 percent of cases, the presence of a Taser alone is enough to defuse dangerous situations safely and quickly.

Cameras & Sensors

Axon’s second major pillar is its Cameras & Sensors portfolio, which includes Axon Body 4, Axon Fleet 3, Axon Outpost and Axon Lightpost. Within this segment, the Axon Body line is widely believed to drive the majority of revenue.

Axon’s dominance in body-worn cameras is long-standing. After acquiring rival VieVu in 2018, Axon effectively consolidated the market and today controls roughly 85% market share of body-camera deployments in major US police departments. That dominance persists because it sits at the heart of two reinforcing loops:

First loop: OSP bundling.

Most agencies do not buy cameras in isolation. They adopt the OSP, which pairs the Taser with Axon Body cameras. As Taser penetration rises, body-camera penetration tends to follow, because agencies prefer an integrated workflow for training, evidence handling, and chain of custody.

Second loop: Axon Signal and automated activation

Axon’s holsters allow a drawn Taser to automatically trigger the officer’s body camera to begin recording. This creates an immediate evidentiary trail, reducing liability for officers and agencies. Once this workflow is embedded into training doctrine and incident policy, it becomes very difficult for an agency to split vendors for weapons and cameras.

Motorola Solutions is the closest challenger in the market. Its latest product, the SVX Video Remote Speaker Microphone, combines voice communications with high-definition video capture in a single device. This is Motorola’s attempt to position a unified communications plus sensor endpoint directly against Axon Body 4. What Motorola lacks, however, is the upstream trigger device. Without a conducted-energy weapon that automatically activates the camera system, Motorola cannot replicate Axon’s end-to-end use-of-force workflow.

Direct comparisons between the two companies are challenging because their reporting structures differ. Motorola’s video security and access control segment includes enterprise CCTV, fixed cameras, and Avigilon video management systems, most of which are outside frontline policing. Axon’s Cameras and Sensors revenue, in contrast, is tightly focused on officer-worn and in-vehicle devices.

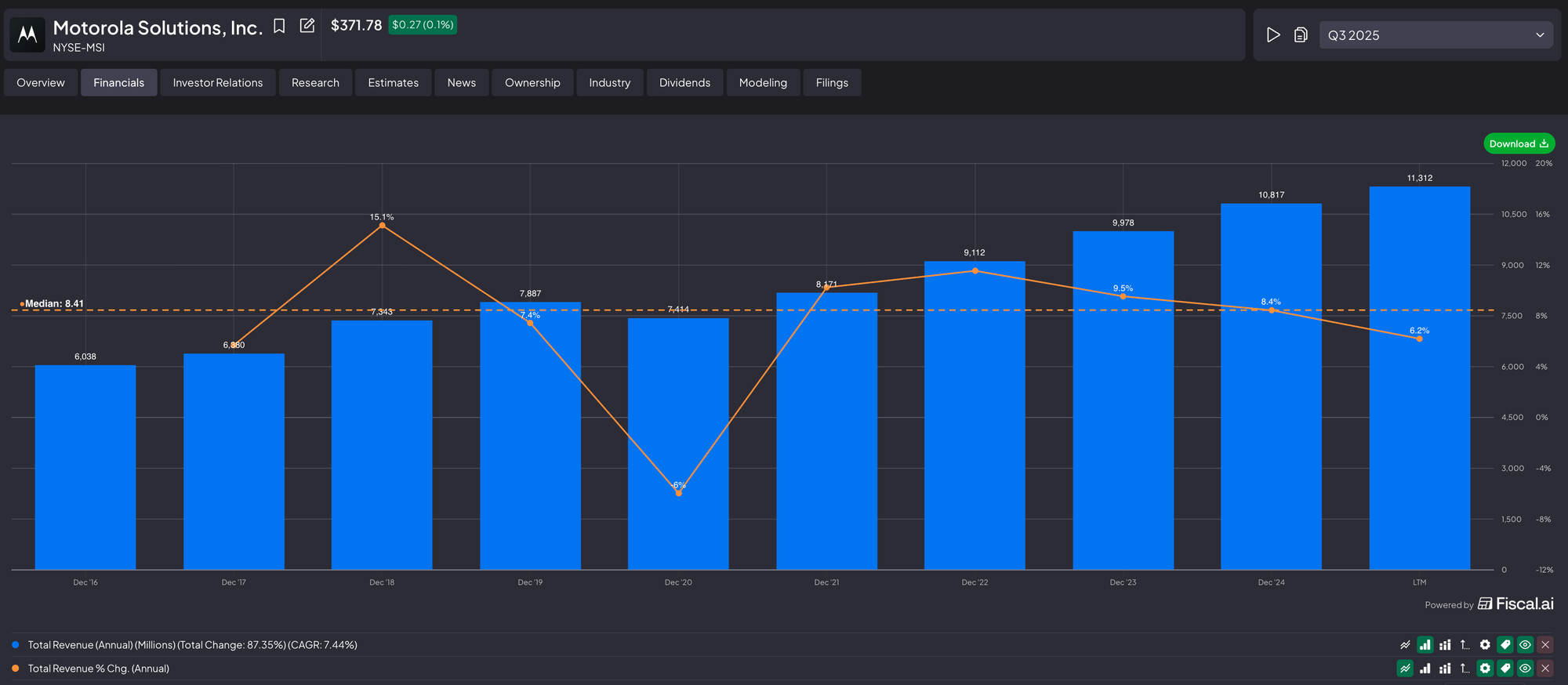

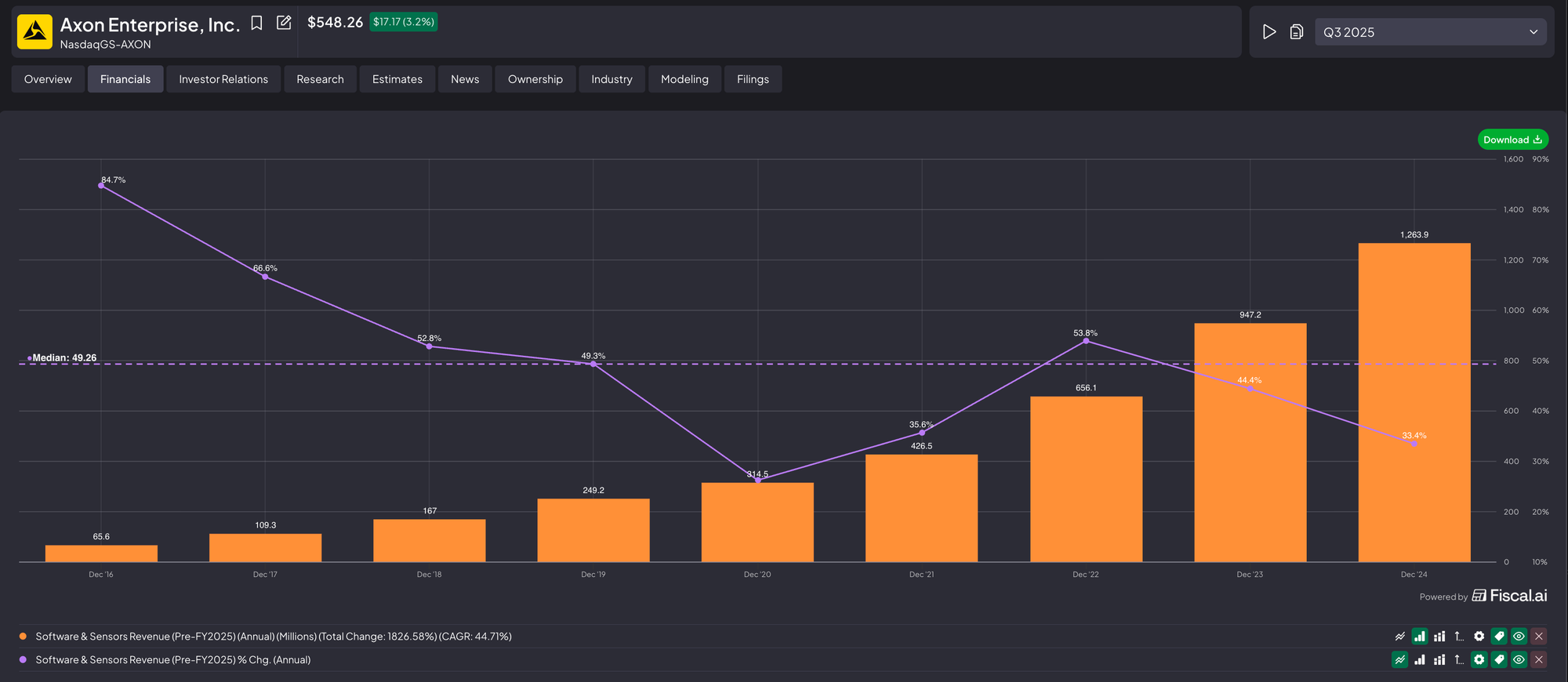

Still, one rough indicator of competitive momentum is to compare Axon’s ex-Taser growth against Motorola’s overall revenue growth on a non-weapons basis. Over the past nine years, Axon has grown at a median rate of roughly +49% year over year, while Motorola has grown at a median rate of roughly +8.4% over the same period (see diagrams below). Axon is scaling off a smaller base, but the delta highlights how quickly demand for its integrated hardware plus cloud model has accelerated.

Cloud Software

One of the main reasons Motorola stands out as Axon’s closest integrated rival, is that it operates a parallel Bodycam-to-Cloud architecture of its own. The core of that system is Motorola's CommandCentral DEMS, a cloud-native digital evidence repository similar in purpose to Evidence.com.

Footage from Motorola’s body-worn and in-vehicle cameras uploads directly into DEMS, which lives inside the larger CommandCenter Software Suite. This makes Motorola one of the few companies attempting a full sensor to cloud loop, connecting frontline devices to evidence management, analytics, and command-center workflows.

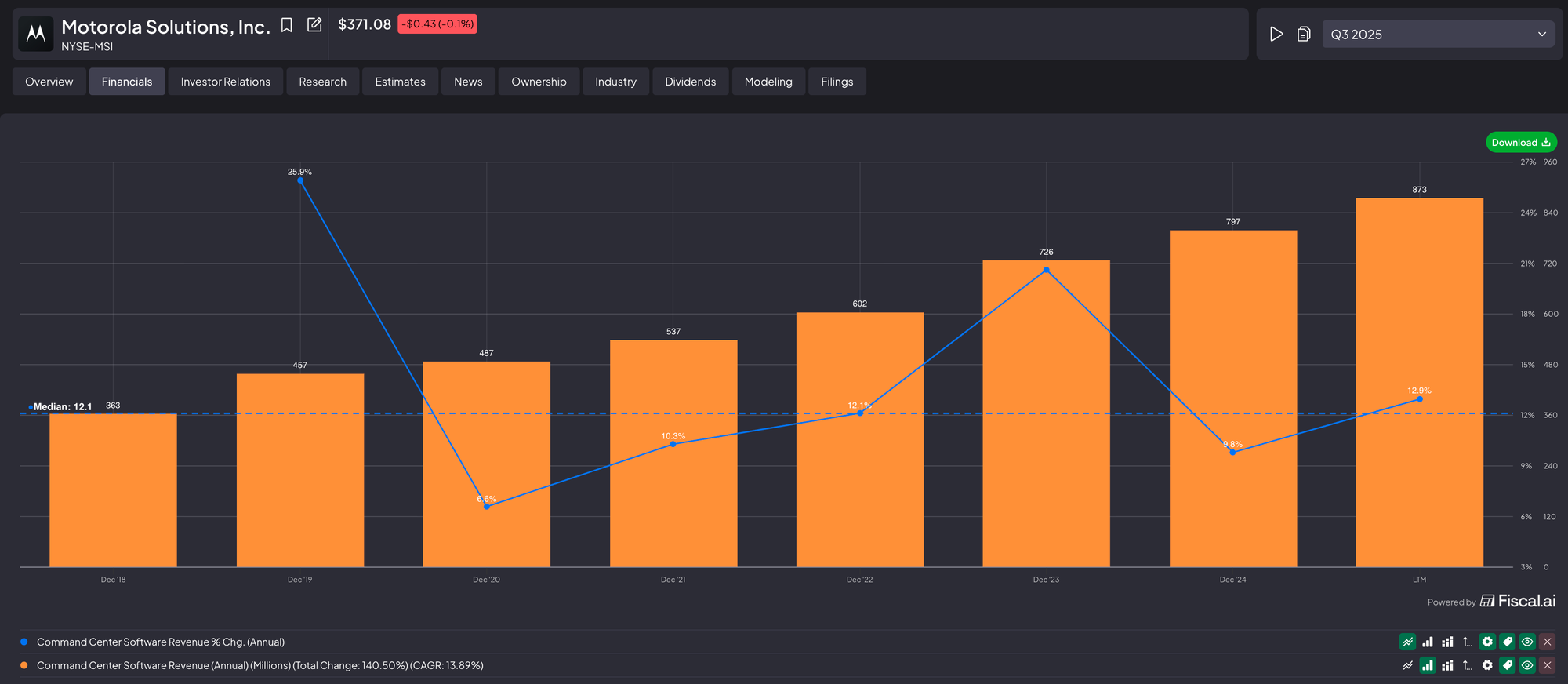

Growth trajectories, however, show a widening gap. Over the past nine years, Axon’s Software and Sensors segment has grown at a median rate of about +49% year over year, compared with roughly +12.1% for Motorola’s CommandCentral software (see 2 diagrams below). The comparison is not perfect, since Axon’s segment includes both software and hardware, while Motorola’s figure reflects software only. Even with that caveat, the divergence once again illustrates how much faster Axon is scaling its integrated cloud platform relative to Motorola.

Dispatch, 911 and Radio Workflows

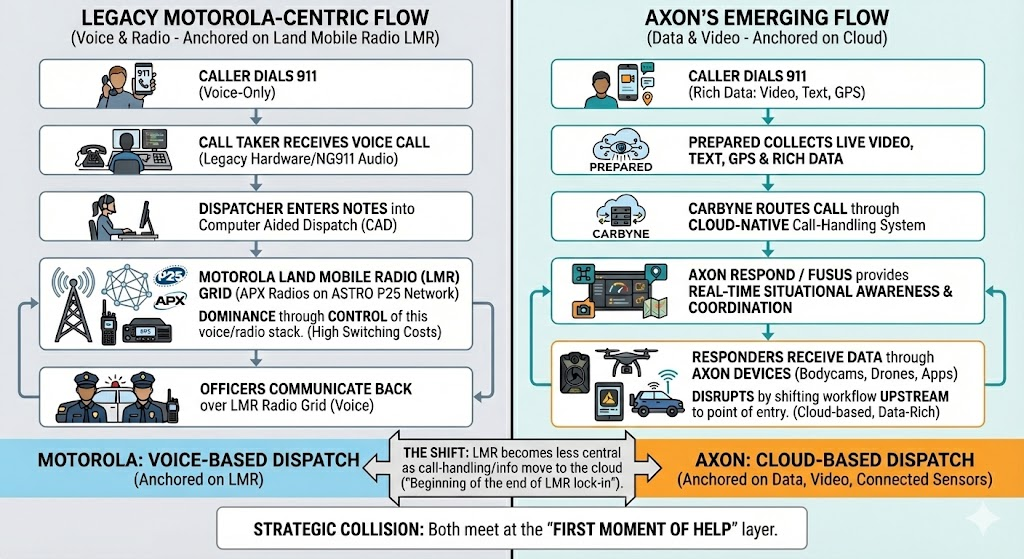

To understand the next competitive frontier between Axon and Motorola, it helps to zoom out and look at how a typical 911 call flows through the system today.

Motorola’s dominance comes from its control of the voice and radio stack. This infrastructure has enormous switching costs. Agencies spend tens of millions on radio networks with 10 to 15 year refresh cycles, which is why the LMR layer has been the hardest part of public safety to disrupt.

That is the rationale behind Axon's Prepared and Carbyne deals. The easiest way to fully grasp how Axon is re-building the 911 stack is to watch this 3 min video.

This shift is profound because once the call-handling and information layers move to the cloud, the LMR system becomes less central over time, potentially spelling the beginning of the end for LMR lock-in.

Motorola’s acquisition of RapidDeploy, a leading cloud-native Next Generation 911 provider, is its counter to Axon’s moves. RapidDeploy augments Motorola’s NG911 and call-taking suite with cloud mapping, caller location intelligence, and next-gen digital capabilities.

Why the 911 dispatch competition matters for investors

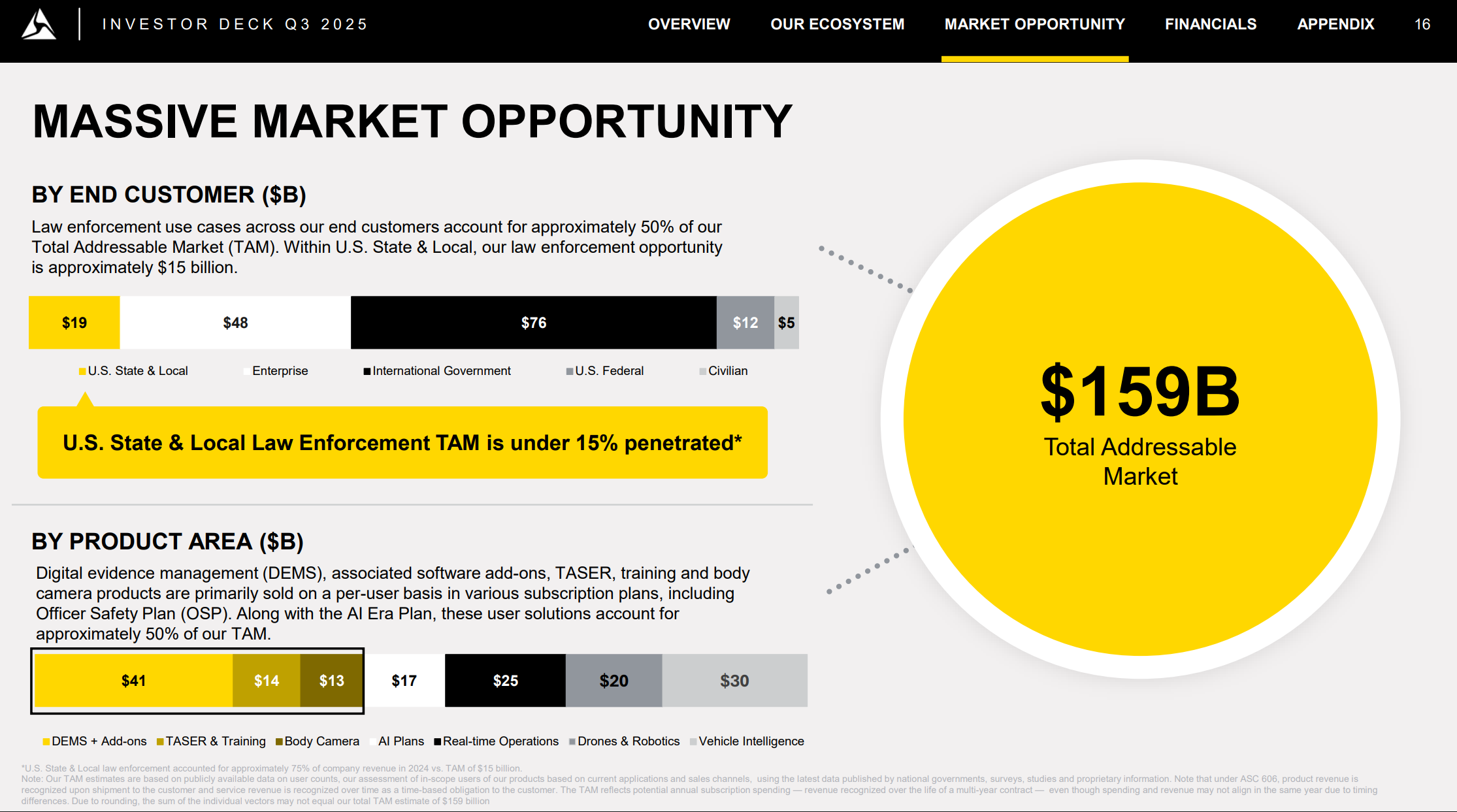

The company that controls 911 dispatch controls the entry point of the most significant public safety workflow. That entry point spills into several large adjacent TAM buckets:

- Digital Evidence Management (DEMS): USD 41B

- Real-time Operations: USD 25B

- AI Software: USD 17B

See Axon’s Q3 2025 TAM breakdown below (attached image)

This is why the next few years of Axon vs Motorola competition will be shaped less by bodycams (a segment Axon has already won) and more by who can define the next-generation 911 experience.

Financials

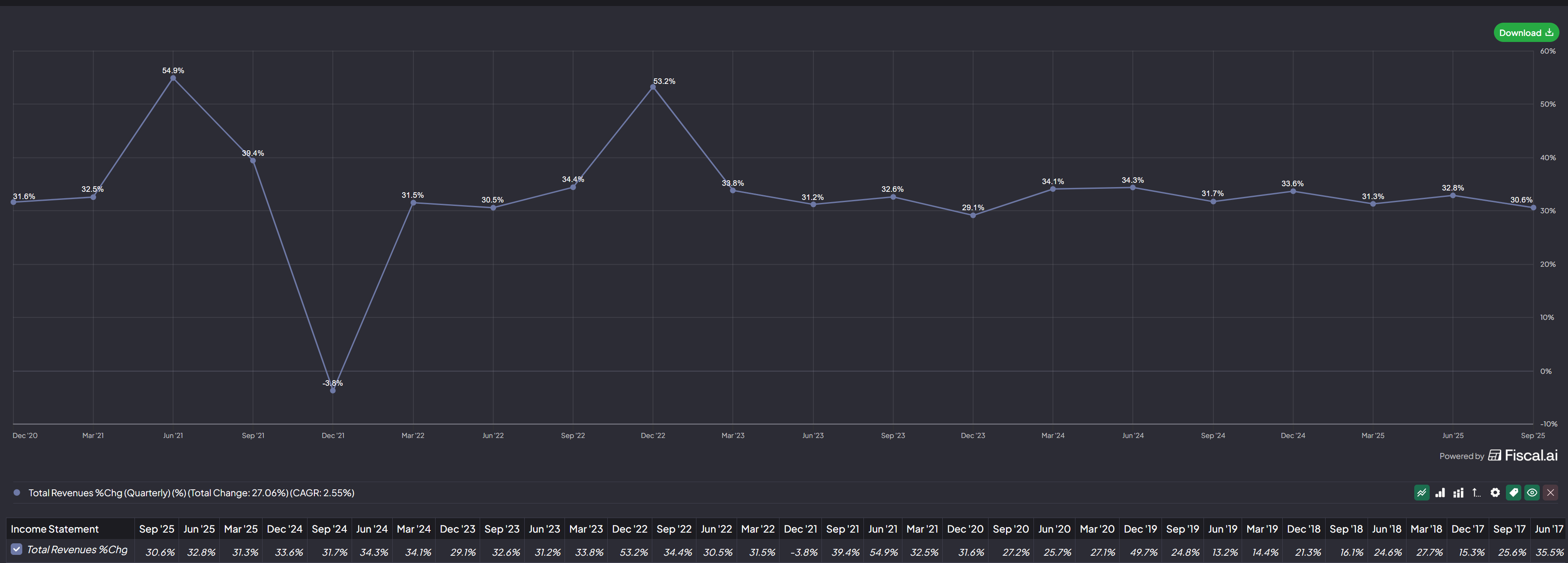

Axon has delivered more than 25% year over year revenue growth across 15 consecutive quarters. The only exception is Q4 2021, where sales dipped 3.8 % year over year due to two one-offs:

- A tough comparison against a USD20M US Federal TASER order in Q4 2020

- Temporary supply chain constraints affecting Taser 7 and Axon Body 3 production

Excluding that quarter, Axon would have posted more than 24 straight quarters of >25% growth!

Before 2025, Axon reported two buckets:

- TASER

- Software and Sensors (Evidence.com, body cameras, in-car cameras)

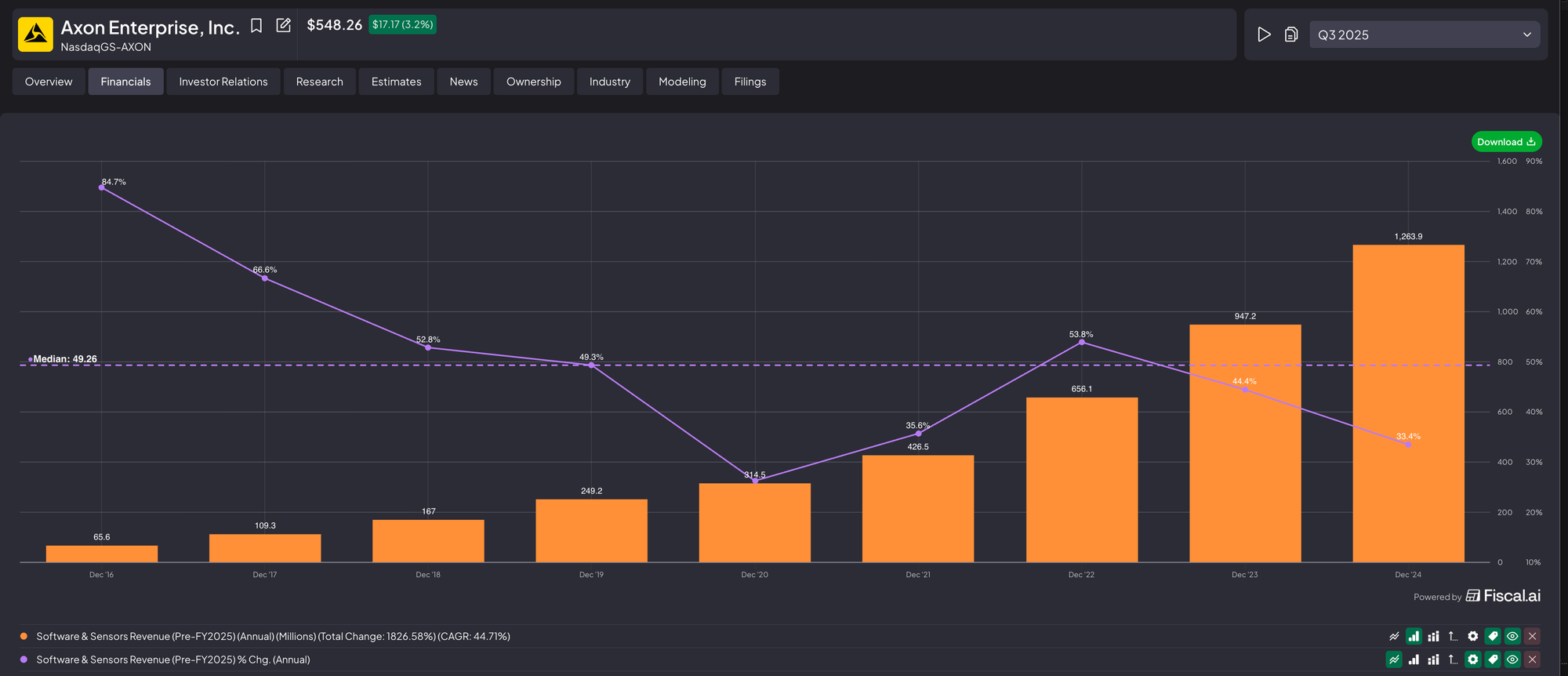

From Q4 2021 onward, Software and Sensors became the larger revenue driver, maintaining a 39% median YoY growth rate, well above TASER's 24% median.

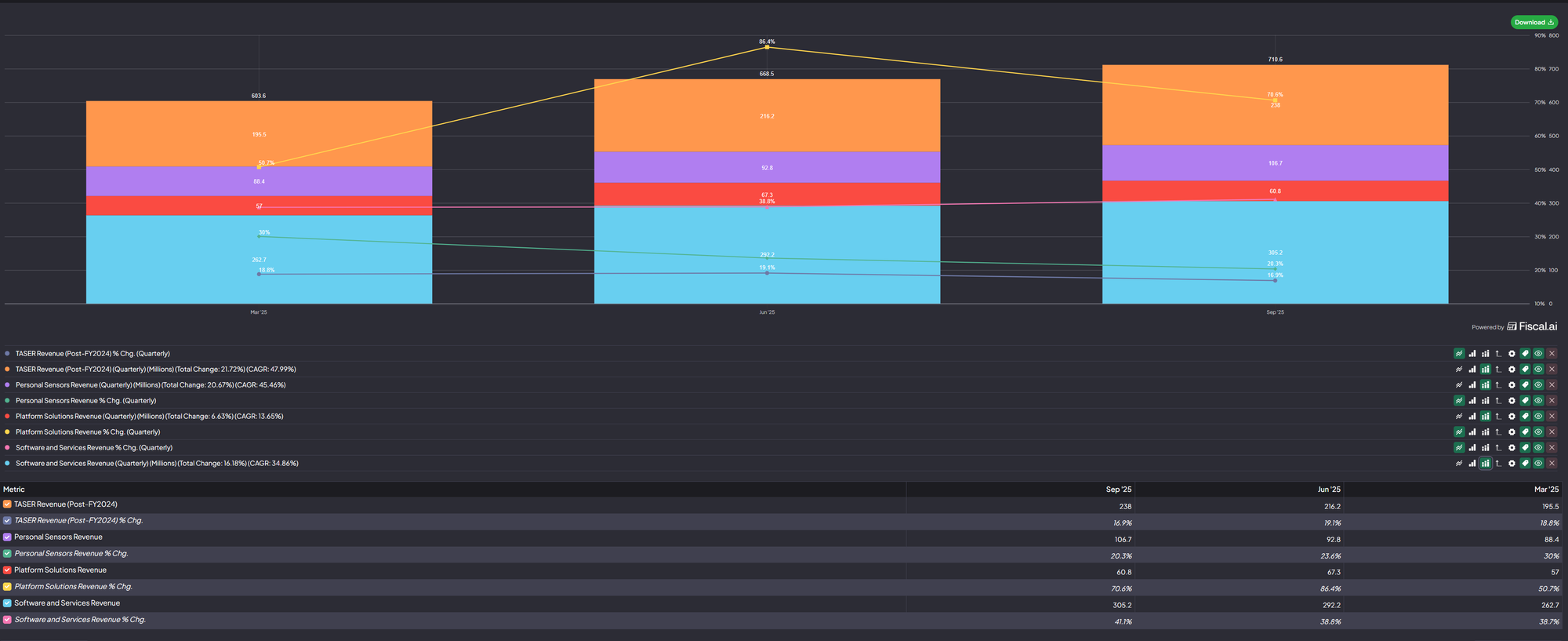

Post-2024, Axon split Software and Sensors revenue into more granular segments (see below) to show the expanding cloud mix. The shift was important because it now allows far easier analysis of each business segment.

The most important reveal from the above chart is that the pure software segment is now the single largest contributor to revenue, accounting for ~43% and is the 2nd fastest growing segment at +40% YoY, less than Platform Solutions ~(+70% YoY but off a far smaller base).

It is reasonable to infer that Evidence.com was likely the largest contributor of Axon's multi-year growth pre-2024. This makes sense, as all roads (camera, Taser, drone, fixed sensor) lead to Evidence.com.

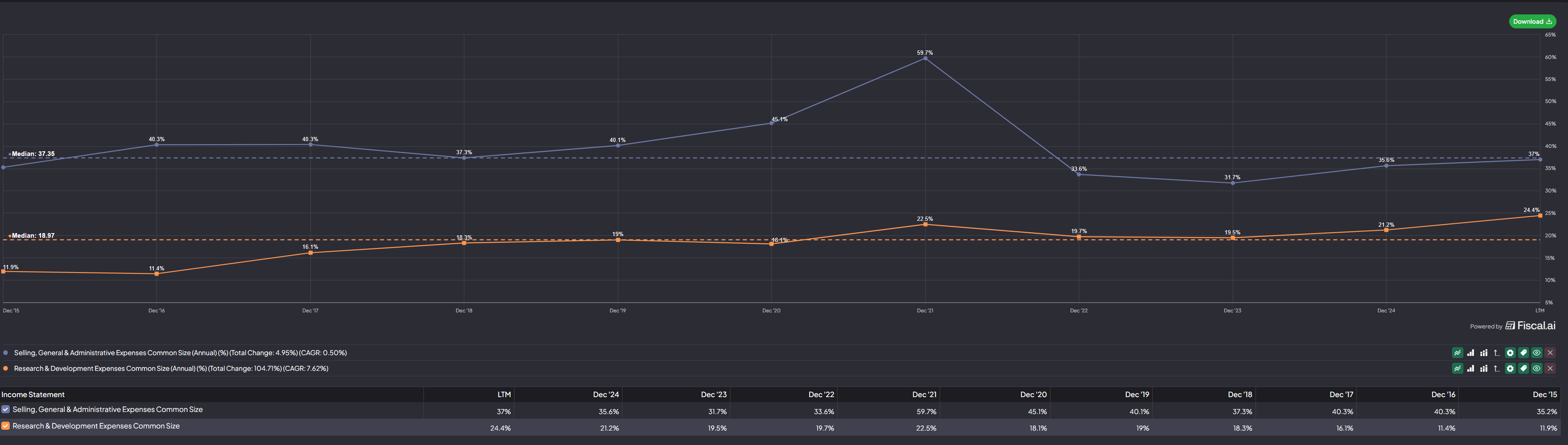

Margins

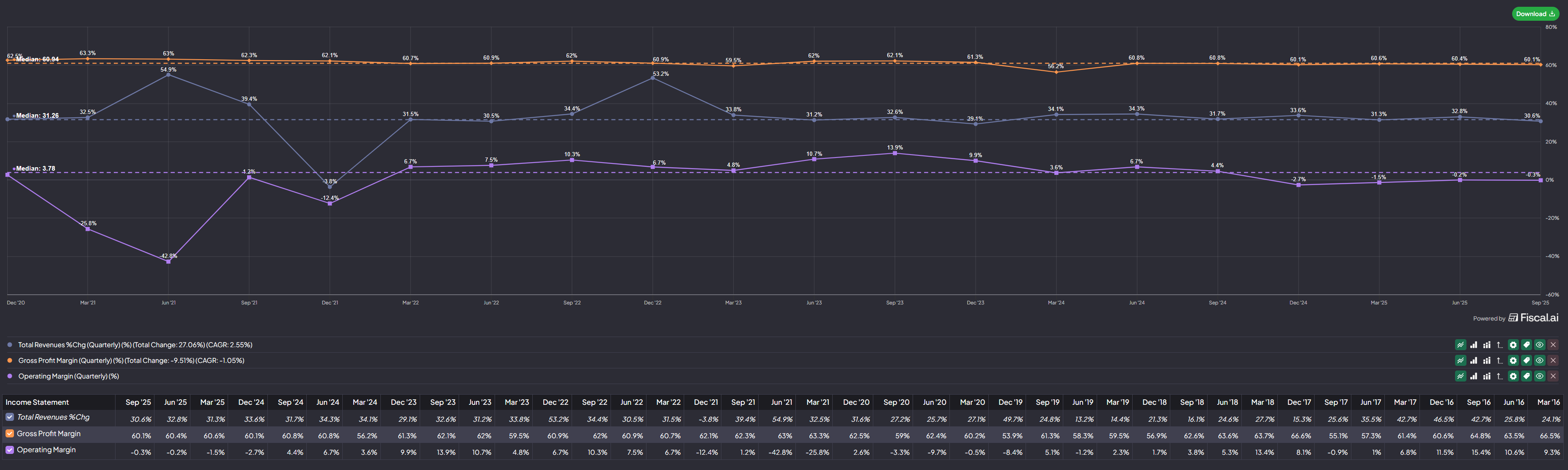

Over the last 40 quarters, while growing revenue at ~31% YoY, Axon has maintained:

- Gross margins of ~61%

- Operating margins of ~3.78%

One important observation is Axon’s R&D intensity, which has averaged about ~19% of total revenues over the last decade (see below diagram). This is more than double Motorola’s ~8.7% and sits close to Meta’s ~21%, which is the highest among hyperscalers.

Axon’s elevated R&D spend is visible in its rapid cadence of product innovation across TASER, body cameras, AI features, cloud software, drone program and more. Given how early Axon is in its platform expansion, this spending level is justified and serves as a competitive advantage versus slower-moving incumbents.

SG&A has also been steady at ~37 percent over the same period. As Axon grows and a larger share of its revenue shifts toward software subscriptions rather than hardware shipments, both R&D and SG&A are positioned to deliver operating leverage. This is amplified by a lollapalooza effect where:

- The fastest and largest growing part of the business (Software)

- Is also the highest-margin part of the business

Once Axon scales past its current high-growth investment phase, both R&D and SG&A have meaningful room to compress as a percentage of revenue. This sets the stage for free cash flow margins to rise well above today’s ~11%.

Management

Modus Operandi & Soul in the game:

One thing worth highlighting is Rick Smith’s unusual operating style. In the Q4 2024 Earnings Call, he explained how he works with his executive team:

I'm like a bee carrying pollen back to the hive, and then Jeff's (CTO) got to make sense of it all. Segment it, work with our 1,000 plus engineers and product people to take these great customer ideas and put them together. And then Josh (President) and Brittany (CFO) are going to like, then staff and execute the business to run it, and I get to go out on the road again. So the team works really well together and I just, I love my job getting to go, just sort of imagine, talk to customers about their problems and try to match it on what tech is going to work. To be honest, Jeff really holds me accountable. A lot of our conversations, Jeff uses the word “actually” a lot. Like, okay Rick, like this is great stuff. What can actually work right now in a way that customers will actually use, and it won't disappoint them, and it's not going to be buggy.

This gives a clear sense of Rick’s role. He is not a passive CEO sitting behind dashboards but more a field operator who spends significant time with customers, absorbing frontline problems and bringing those ideas back into Axon’s engineering hive. Combined with the earlier chapters of his story, this paints a picture of a founder driven less by financial reward and more by a deep personal mission. In every sense of the phrase, Rick has soul in the game.

The best way to get a feel of his love for the business is to watch the Boldly Go Podcast, where Rick shares decades of stories about Axon’s innovations, failures, pivots, and technical breakthroughs. When you watch it, you'll realize it's a bunch of geeks passionately discussing about tech stuff with little Youtube viewership! Much of the narrative in this article actually draws from the podcast episodes because some intimate insights of Rick's character simply do not exist anywhere else.

M&A philosophy and examples:

Rick’s approach to acquisitions is interesting. The clearest window into this comes from the Q3 2025 Earnings Call, where he describes his recurring decision loop:

...you know, every time we move into a new space, we do a thoughtful make, build, buy or partner analysis...

And when discussing the Prepared and Carbyne acquisitions:

...if you look at the types of investments or acquisitions we're making, we're not buying mature or cash cow businesses. Those tend to come with a lot of tech debt. We're a disruptor. And when we identify like we looked at coming out of our strategy meeting earlier this year one of the takeaways, I sat with the team and said, look, with the AI sort of explosion that's happening, now is the time for us to make our move into AI voice, in particular on the 911 call space. And we did a hard look at should we build this ourselves or not? And as we looked around, we actually found two very talented teams that were relatively early with very different sort of product offerings, one that Prepared, that goes wide, quickly and easily, and another one that goes deep and really sets the foundation for the long term. And so we said, look, this was on our roadmap. The decision was we found two awesome teams. They're both pretty early in their growth cycle, but we think they're at the perfect time of the maturity of their platforms, their great teams built on modern tech. You know, what a great way to integrate that into our ecosystem. It's not like we're again buying something that's mature where we're going to rationalize sales teams and try to cut our way to profitability. We think this is what makes our ecosystem so sticky and so valuable over the long term.

This illustrates a very intentional capital allocation philosophy. Axon does not buy outdated assets nor acquire for revenue optics. It targets early-stage, modern-architecture teams whose technology integrates naturally into Axon’s long-term flywheel without adding technical baggage. It is one of the cleaner and more coherent M&A strategies in the public markets today.

Skin in game:

As the founder and CEO of Axon for the past 32 years, Rick Smith owns 3.9% of the company, worth about 1.7 billion dollars as of November 2025.

According to Forbes, roughly 94% of his net worth is tied directly to Axon stock. If the business stumbles, Rick personally feels that pain.

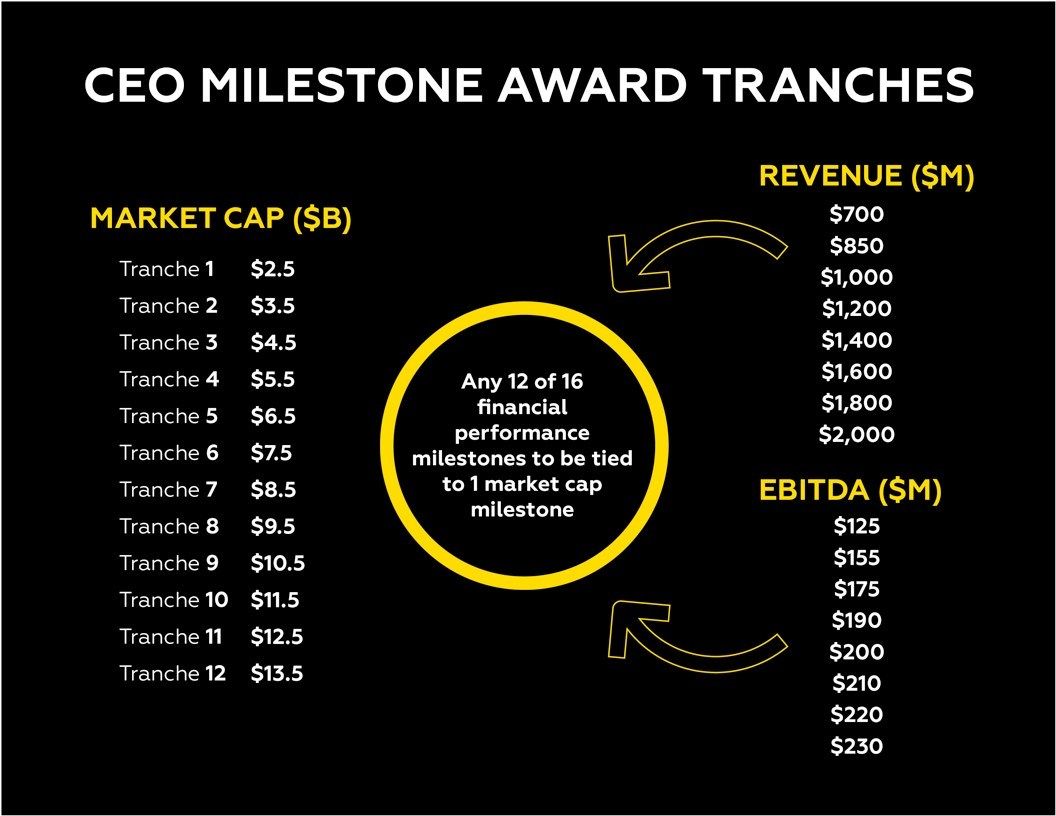

In 2018, inspired by Elon Musk’s compensation structure, Rick proposed a 10 year performance plan where he received:

- no salary

- no cash bonus

- no time-vested equity

He would only be credited with compensation if Axon hit extraordinary market cap, revenue, or EBITDA milestones (below).

At the time these milestones were announced, Axon was only a 1.4 billion dollar market cap company with 365 million dollars of revenue and 30M in EBITDA. The milestones looked almost impossible.

What followed was remarkable. By December 31, 2023, only half way through the 10 year window, all 12 tranches were achieved, triggering 246 million dollars of stock compensation to Rick.

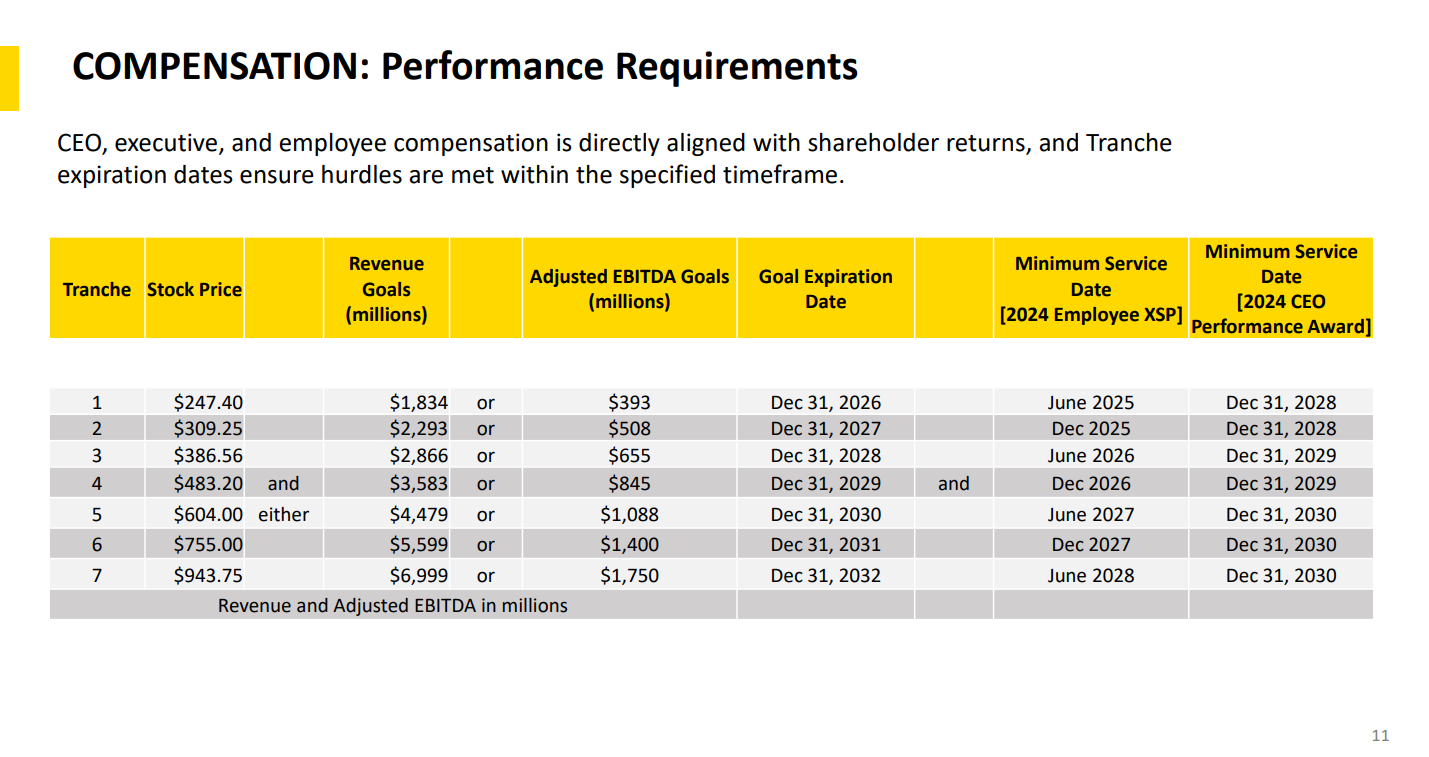

In 2024, Axon refreshed the plan with a new 7-year CEO Performance Award, again with zero salary (see below chart). The new plan requires both performance milestones and minimum service periods, reinforcing the same alignment between Rick’s personal wealth and long-term shareholder outcomes.

As of 21 November 2025, Axon stands at:

- USD522 dollar stock price

- USD2.5 billion dollars LTM revenue

- USD521 million dollars adjusted EBITDA

This shows how much distance still exists before all seven new tranches can be achieved.

Risks

Stock Based Compensation and Dilution

One of the most common objections investors raise about Axon is dilution from Stock Based Compensation. The chart below shows Axon’s share count rising at a ~4 percent median CAGR over the last decade.

There are two key reasons why this dilution needs to be viewed with nuance:

1. SBC has been tied to real performance, not time.

The rise in share count since 2018 aligns directly with management unlocking tranches from the 2018 CEO Performance Award and the employee-modified version (XSPP). These only vest when Axon actually hit demanding Revenue, EBITDA, and Market Cap milestones.

Dilution that results from genuine value creation is fundamentally different from companies that issue time-vested equity simply for retention.

2. Axon must use equity to compete for talent.

Axon is still an early-stage, high-growth company scaling revenue at more than 30 percent per year. Competing for engineering talent against the likes of Meta, Amazon, and Google is nearly impossible on Axon's base salary alone. SBC allows Axon to recruit strong engineers without diverting cash away from R&D. It is effectively the only viable currency for a company still in its compounding phase.

For now, given Axon’s growth stage and innovation cadence, SBC remains a rational lever but I will be carefully watching this metric as the company continues to grow.

High risk and Regulated industry

Axon operates at the center of public safety and law enforcement, a domain that is inherently high-risk and highly scrutinized. The company has faced:

- regulatory pressure, such as the negative media cycle and SEC inquiry in 2005

- ethical controversies, including the 2022 proposal of a Taser-equipped drone for school safety which led to mass resignations from Axon’s AI Ethics Board

- frequent antitrust accusations, for example the lawsuit from several US cities alleging monopolistic practices in body cameras and conducted-energy weapons

These factors create higher operational volatility than typical tech companies. On the bright side, Axon's other optionalities beyond the more scrutinized public safety sector looks promising (more on this below in the "Why it's still early days" section )

Fake origin story and questionable management?

In 2023, Reuters published an investigative report questioning elements of Axon’s origin story and raising concerns about internal culture. This report is a worthwhile read for anyone deeply interested in Axon.

Although it is difficult to objectively determine whether Rick’s account or Reuters’ interpretation is closer to the truth, what we can assess is management’s track record. Over 32 years, Rick has guided Axon from a near-insolvent startup to a multibillion-dollar category leader while consistently delivering innovation, navigating crises, and compounding shareholder value. Based on this long-term track record, I currently lean toward continuing to trust Rick Smith’s leadership and execution.

Key man risk

Rick Smith is central to Axon’s DNA. His persistence, willingness to iterate through failure, and decades spent directly engaging with frontline users are a large part of why Axon survived multiple near-death moments.

There is no obvious internal successor who matches his combination of vision, product instinct, and customer obsession. If Rick were ever to step down, the business and investor confidence would likely take a hit. This remains one of the most meaningful risks to the long-term thesis.

In the next premium subscriber section, I cover,

- 4 Growth Catalysts: Why it's still early days for an Axon Investment

- My Valuation buy levels: The recent selloff - Opportunity or Trap?

- My specific portfolio next steps related to Axon

🔒Unlock the below with premium tier