The Only Luxury Stock Worth Owning

Note: This article originates from my Stock Research Vault. At the end of this article, I share my valuation buy levels and next potential moves with this company for premium subscribers.

I'm generally not a fan and have never owned retail stocks that rely on brand moats. In my experience, they are one of the most overrated concepts in investing: fickle, culturally dependent, and what's "aspirational" today can become irrelevant tomorrow.

But there is one exception - A 189 year old company that has been continuously run by the same founding family for six generations. It has survived two World War and a hostile takeover attempt. Each time, the next generation rallied and the brand emerged stronger.

Today, this company's share price sits 45% below its all-time highs, at valuation levels not seen since the 2022 selloff.

Even at this beaten-down levels, it still compounded shareholder returns at ~22% annualized over the last decade, nearly doubling the S&P 500's ~13% over the same period.

This company, is none other than Hermes (Ticker: $RMS on Euronext Paris).

In this article, I present a deep-dive on why Hermes is the only luxury stock I would consider owning, including:

- The Irreplicable Moat: 189 Years of Heritage

- The Hermes Game & Maslow's Hierarchy of Needs

- Why Not Ferrari or LVMH?

- Financials

- Management

- Risks (🔒Unlock with premium tier)

- Valuation Buy Levels & My Next Moves (🔒Unlock with premium tier)

The Irreplicable Moat: Heritage

Hermes was founded in 1837 by Thierry Hermes, and to this day, the same saddle stitch technique used to craft harnesses for Napoleon III's court is used to make their iconic handbags. When a customer purchases a Birkin bag, they are not just paying for leather and thread. They are paying for 189 years of this unbroken lineage and knowledge.

Hermes is the oldest luxury fashion brand in existence. The beauty of significantly old heritage brands is that this quality of time cannot be 'disrupted'. One cannot spin up a new luxury brand and claim that it is 200 years old unless you have a time machine to accelerate the passage of time.

With each passing year, this moat continues to deepen. I like to call this unique quality, "The Patina of age" (inspired by Jeff Bezos' 10,000 year clock). Compare this with brands like Nike (62 years) & Lululemon (28 years) and you can really start to see the huge contrast and why Hermes has an irreplicable moat by virtue of its history.

The Hermes Game & Maslow's Hierarchy of Needs

Hermes does not have a traditional marketing department. It does not use celebrity endorsements or give free bags to influencers unlike LVMH. When celebrities are spotted carrying Birkins, it is because they purchased them.

The method they use to create demand for their products is a fascinating mechanism known as The Hermes Game.

The way it works, is that you cannot walk into a Hermes boutique and buy a Birkin off the shelf. Birkins and Kellys are not displayed or listed for sale. Instead, you must build a relationship with a Sales Associate (SA) at a local boutique. You demonstrate genuine interest in the brand by purchasing across categories: scarves, homeware, jewelry, ready-to-wear. Over time, if your SA deems you worthy, you receive "the call" - a discreet invitation to view and potentially purchase a coveted handbag.

Industry estimates suggest customers need to spend up to 5:1 on other Hermes products relative to the bag's price before being offered one. For a EUR 10,000 Birkin, that means EUR 10,000 to EUR 50,000 in "pre-spend" first.

A few reasons why this 'Game' is essential for Hermes long-term foothold in luxury:

- It transforms a handbag purchase into a multi-year, multi-product customer journey, dramatically increasing lifetime value

- It creates organic demand overflow into every other Hermes category as customers buy scarves, belts, homeware as part of the 'Game'.

- It makes the purchase an achievement, which customers broadcast socially, generating free word-of-mouth

- It creates a resale market where Birkins trade at 20-50% premiums above retail, reinforcing the perception of Hermes as a store of value

No other luxury brand has this. At Louis Vuitton or Kering Group brands you walk in and buy what you want. At Hermes, money alone is not sufficient. You must earn the right to spend it.

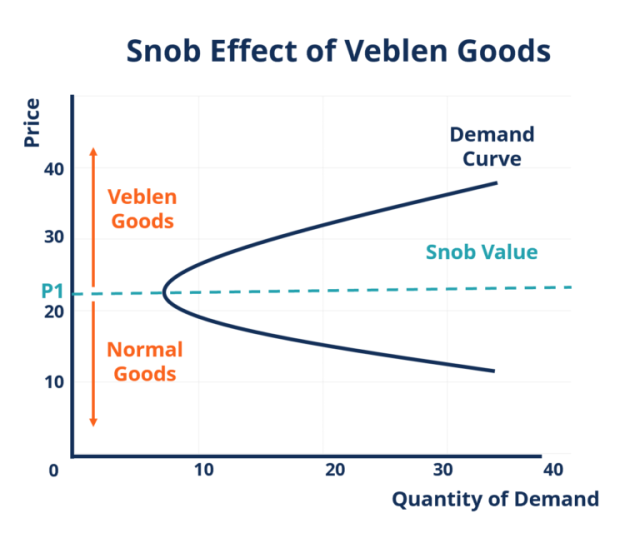

The Veblen Good Effect

Most products follow a standard demand curve: raise price, demand falls. Hermes operates in the inverse. As a Veblen good, higher prices increase desirability because the signal only works if the price is prohibitively high.

Hermes reinforces this by refusing to increase production volume to meet demand. Despite opening new workshops (the 27th leather goods atelier is planned for 2028), each bag is still made entirely by a single craftsman. CEO Axel Dumas has stated publicly that "demand exceeds capacity." This isn't a bottleneck but an intentional strategic choice.

Despite this intentional supply constraint, Hermes has two ways to continue growing earnings over the long term,

- The Hermes Game means that although handbag supply is controlled, all other parts of the business (scarves, jewelry, homeware, ready-to-wear) are not, and serve as a longer tail foundation to prop up the business' earnings

- Although handbag supply is controlled, Hermes can keep increasing the price of each handbag so that the net effect is still a growth in earnings. The retail price of a typical Birkin has grown at a long-term CAGR of roughly ~5%, according to Sotheby's. In recent years, annual price increases have accelerated to 6-10%, comfortably outpacing inflation.

Why the desire for an Hermes bag will never change

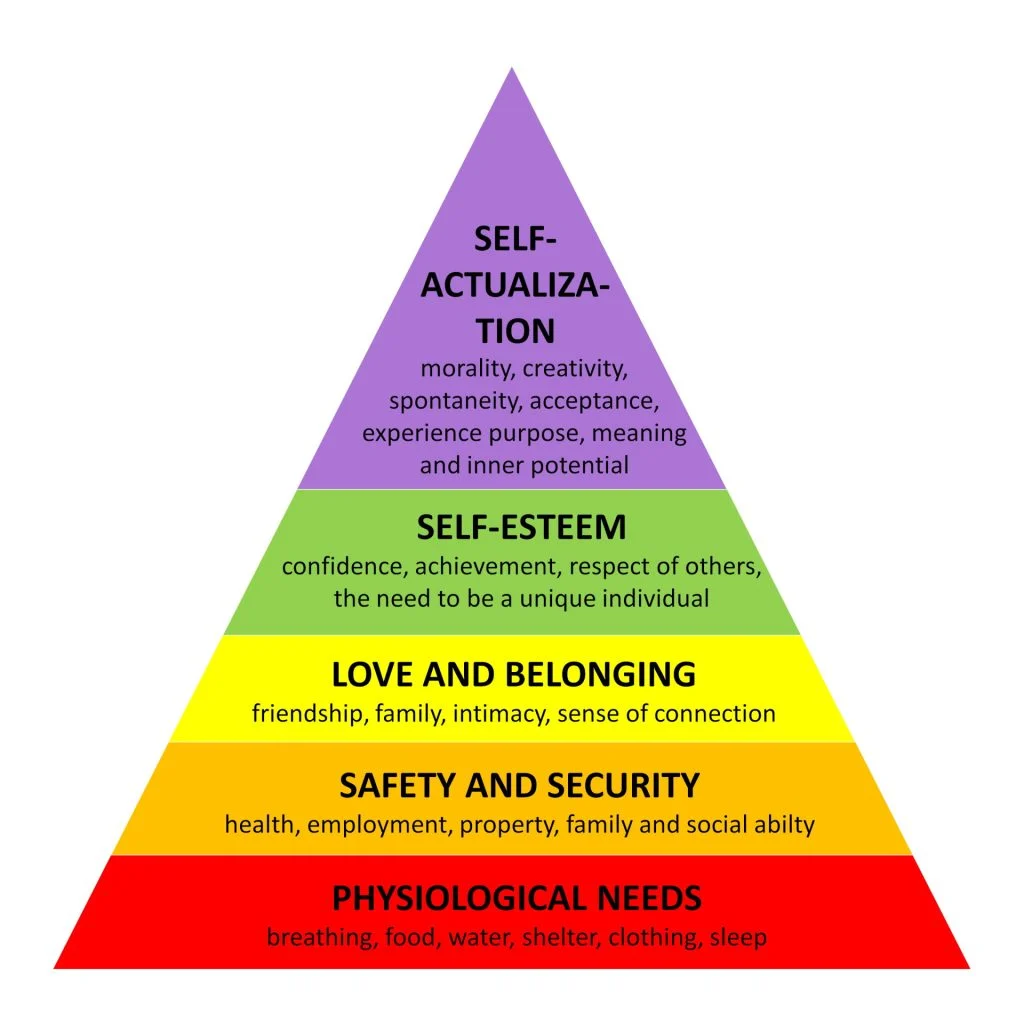

At the deepest level, my conviction in Hermes' long-term success rests on Maslow's hierarchy of needs.

Hermes targets societies where the ultra-rich have already secured the first two levels of needs: Physiological and Safety. Next up the pyramid is Love and Belonging and Self-Esteem, where one of the most common ways to 'fulfilling' these needs is owning a luxury good that signals to others that you 'belong' and are unique.

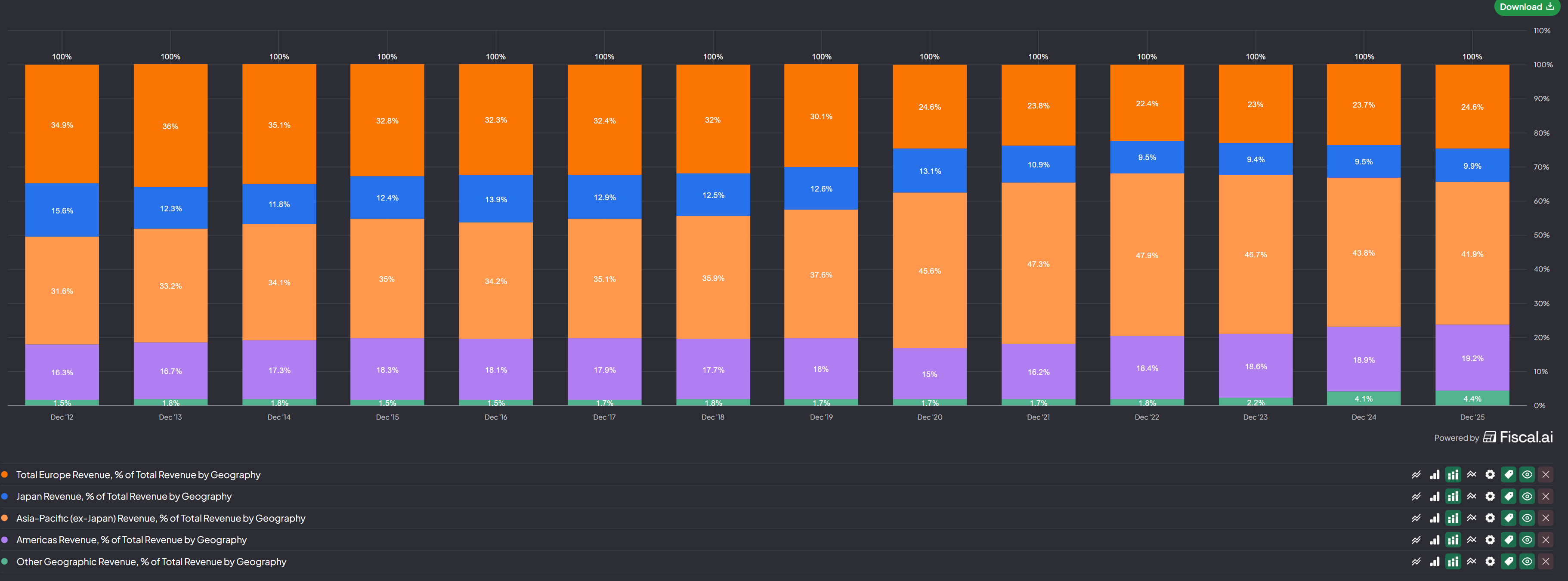

In particular, Asian society readily identifies the ownership of luxury goods as a shortcut up the social status ladder. This is one of the reasons why the largest % revenue contribution to Hermes continues to be the Asia Pacific growth story (see below breakdown):

The desire to signal social standing through luxury is as old as civilization. There will always be a class of people who want to signal wealth and taste through objects recognized by their peers. For as long as that impulse exists, there will be a place for Hermes. The last 189 years is evidence and why I believe over the long-term, Hermes will continue to eke out cashflows and maintain its position.

Why Not Ferrari or LVMH?

Before making the case for Hermes, let me address why I'm not interested in two other commonly discussed luxury investments.

Ferrari:

Ferrari is often held up as the ultimate luxury compounder. On the surface, the numbers look incredible: pricing power, scarcity, heritage and passionate customer base.

However, Ferrari operates in an industry undergoing structural change. BYD, Tesla, and a growing roster of Chinese EV manufacturers are reshaping what "prestige" means in the automotive world whilst adhering to ESG. BYD's luxury sub-brand Yangwang has demonstrated that electric powertrains can deliver performance specs matching traditional supercars at a fraction of the price.

Ferrari plans to launch its first fully electric vehicle. But if the core emotional proposition of a Ferrari has always been the roar of a V12 and the drama of combustion, does an electric Ferrari carry the same magic? There is a real risk that Ferrari becomes a hobbyist niche for combustion enthusiasts, with a limited ceiling for growth.

Hermes faces no such risk. There is no technological disruption coming for handbags. No startup is going to 3D-print a Birkin that makes the original obsolete. The desire for a handcrafted leather bag, stitched by a single artisan over 18+ hours, is rooted in human nature, not technology.

LVMH:

LVMH is a portfolio of 75 brands spanning fashion, wines, perfumes, watches, jewelry, and retailing. It is a conglomerate, not a singular brand.

Aspirational vs Ultra-Luxury exposure. LVMH's breadth means heavy exposure to "aspirational luxury" consumers, the segment that pulls back hardest during recessions. When the economy weakens, aspirational buyers stop buying Louis Vuitton. Ultra-wealthy Hermes clients do not stop buying Birkins.

Store-level productivity. LVMH operates over 6,280 stores worldwide. Hermes operates 293 stores across 45 countries. Hermes generates roughly ~EUR 54 million in revenue per store. LVMH generates roughly ~EUR 12.7 million per store across its group. Nearly a 4x difference.

Succession risk. Hermes has successfully passed the baton across six generations. LVMH has never done it once, and Bernard Arnault is already 76. More on this in the Management section.

Inflation Resistant

Hermes' customer base is the global ultra-wealthy. These are not consumers who adjust spending based on interest rates. Compare that to LVMH or Kering Group brands like Gucci, which skew far more towards the aspirational luxury consumer.

During the 2024 luxury downturn, Gucci's revenue collapsed 23%, LVMH's organic growth flatlined at 1%, and Kering's operating income nearly halved. Hermes, in the same period, grew revenue 15% and posted a record 40.5% operating margin.

Financials

Now that we have an idea on the intangible strengths of Hermes, let's look at its financials and compare it to LVMH (its closest competitor).

Revenue Growth

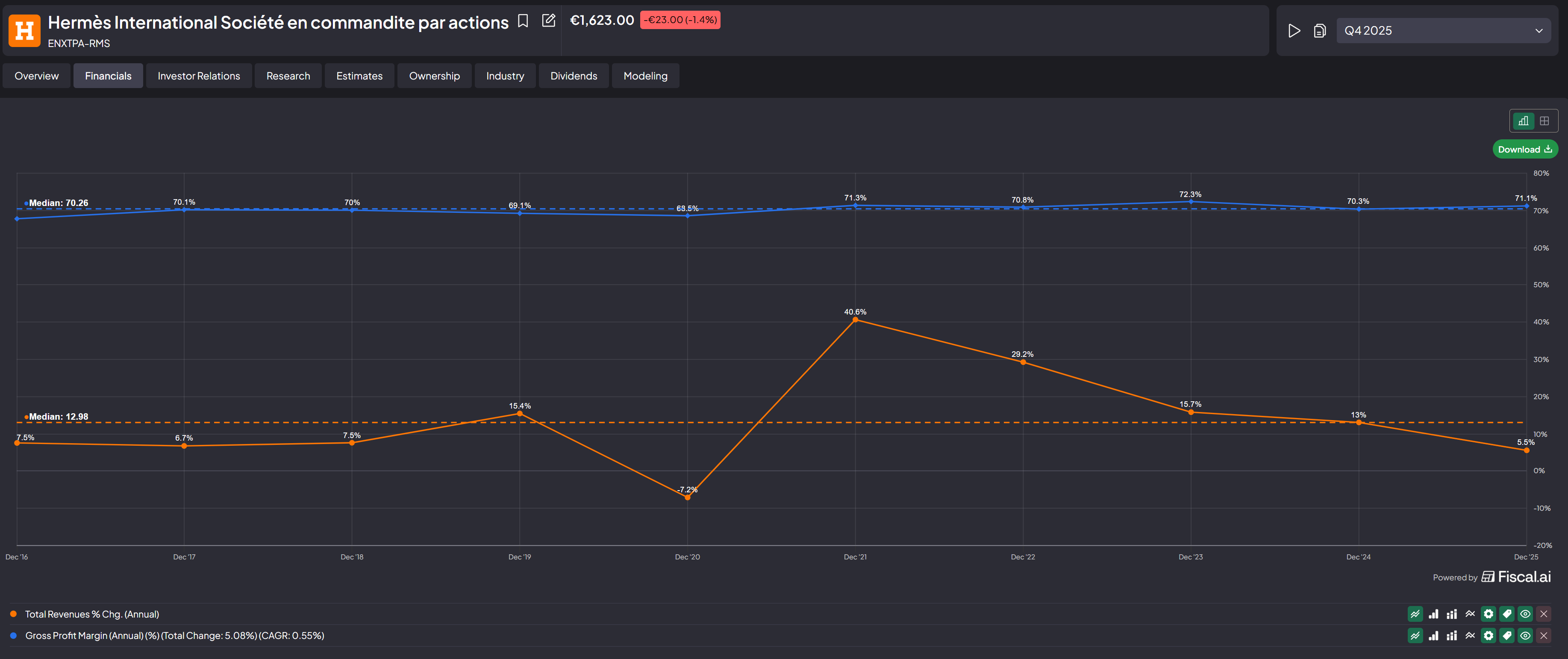

Hermes is growing revenues at a median of ~13% YoY over the last 10 years, about 3% faster than LVMH's ~9.83%. For a company that deliberately constrains its own production to a larger extent, growing faster than LVMH is remarkable.

In addition, it continues to maintain gross margins at ~70% compared to LVMH's 66%.

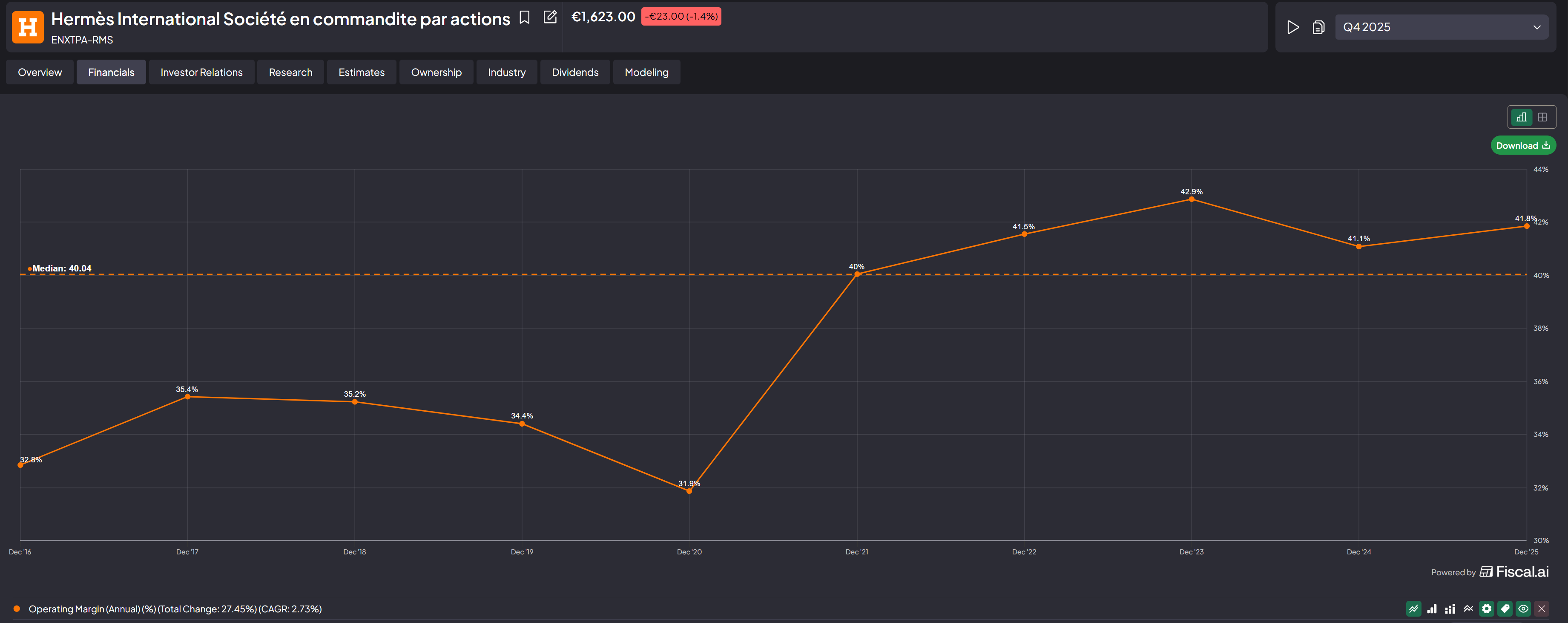

Operating Margins & ROIC

This is where the gap blows open. Hermes is currently doing ~40% in operating margins compared to LVMH's ~21.86%, nearly double its operational efficiency!

In terms of ROIC, Hermes is at~45.6% vs LVMH ~12%, a 4x difference.

Hermes generates extraordinary returns on minimal capital because it doesn't need to acquire businesses or deploy capital into underperforming sub-brands like LVMH. Its sheer focus on a singular brand creates a level of efficiency that is far easier to drive impact than a bloated house of brands.

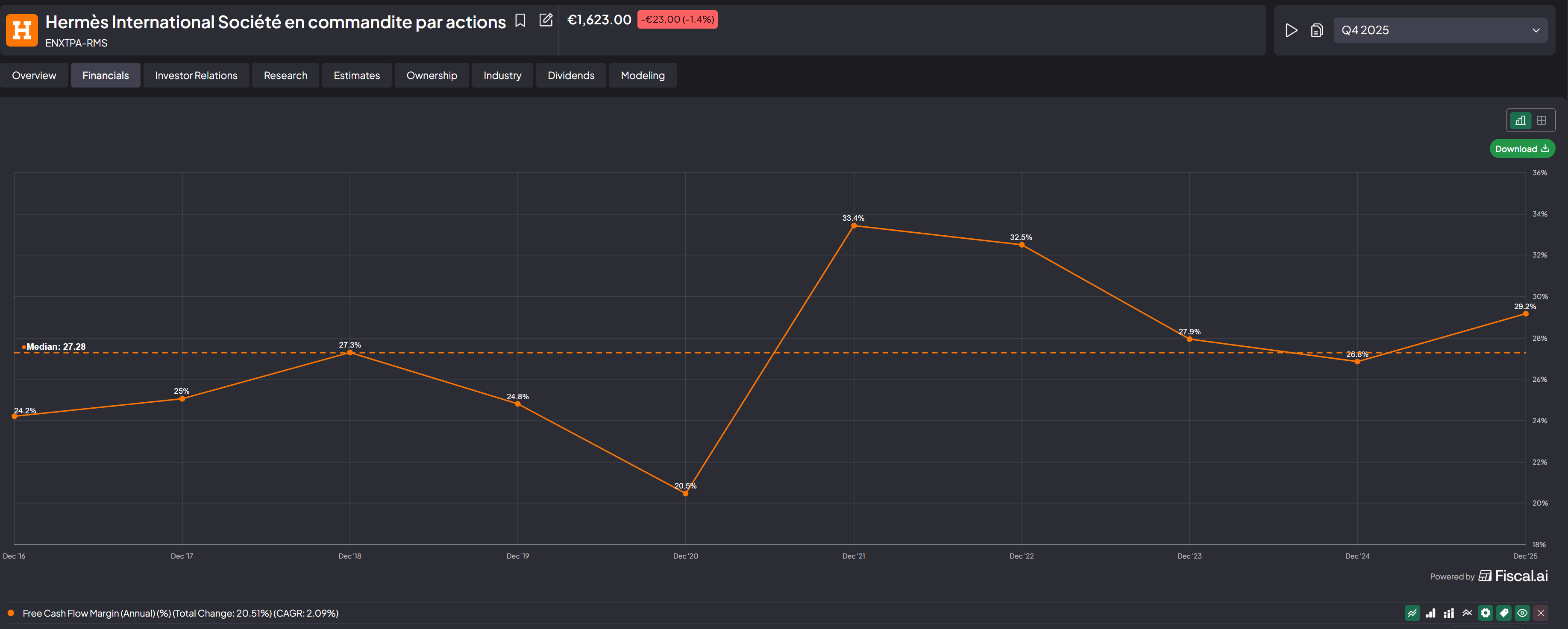

Free Cash Flow Margins

Hermes has a 27% FCF margin compared to LVMH: ~16.8%. For a company reinvesting heavily into new French workshops (four new ateliers planned 2025-2028), this is exceptional.

Balance Sheet: Hermes vs LVMH

Hermes:

- Net Debt EUR 10.13B (negative net debt)

- Debt/Equity 0.1

- EBIT/Interest 121.7

LVMH

- Net Debt EUR 23.73B

- Debt/Equity 0.5

- EBIT/Interest 15.4

Hermes sits on approximately EUR 12.5 billion in cash with negative net debt of EUR10.13B. LVMH carries EUR 23.73 billion in net debt with a Debt/Equity ratio 5x higher. Hermes' EBIT/Interest coverage is 121.7x vs LVMH's 15.4x.

Comparatively, Hermes is a debt-free cash printing machine whilst LVMH is a leveraged acquisition vehicle. In an uncertain macro environment, I much prefer Hermes' balance sheet.

Revenue Per Store

One more interesting stat I learnt from this podcast is that Hermes generates one of the highest revenue per square meter of any retailer, even more than Apple!

Hermes: ~EUR 60,000 - 80,000 / sqm

Apple: ~EUR 50,000 - 60,000 / sqm

Average Luxury fashion store: ~EUR 30,000 - 40,000 / sqm

Lululemon: ~EUR 16,000 / sqm

This speaks volumes as to how efficiently run every new store can potentially be and aligns with the high Return on Invested Capital (ROIC) numbers we're seeing for Hermes.

Management

Six Generations of Proven Succession

Hermes has been continuously run by descendants of its founder:

- Thierry Hermes (1837): Founded as a harness maker in Paris

- Charles-Emile Hermes (1880): Moved to 24 Rue du Faubourg Saint-Honore, expanded clientele internationally

- Emile-Maurice Hermes (early 1900s): Introduced the zipper to French leather goods, pivoted to handbags as automobiles replaced horses

- Robert Dumas (1951): Oversaw the rise of the Kelly bag, expanded silk scarves and product lines

- Jean-Louis Dumas (1978): Created the Birkin bag in 1984, IPO'd in 1993, grew revenue from ~$50M to $2B+

- Axel Dumas (CEO, 2013) and Pierre-Alexis Dumas (Artistic Director): Current stewards

Artisan First, Executive Second

What makes Hermes' succession distinct is the requirement that family members must first learn the craft. Both Axel and Pierre-Alexis apprenticed as teenagers, spending years in the ateliers learning the saddle stitch and crafting bags with their own hands before taking management roles.

This is the opposite of LVMH. All five of Bernard Arnault's children hold senior executive roles across the empire, from Christian Dior to TAG Heuer (where Frederic was appointed CEO at just 25) to Tiffany to Louis Vuitton watches. Each was educated at elite schools and placed into leadership early.

I'm not questioning the Arnault children's talent but rather the succession model. When you've spent years making a perfect saddle stitch with your own hands, you develop a decision-making instinct rooted in craft quality rather than financial/political engineering. You're less likely to approve decisions rooted in short-termism such as production or material compromises.

The critical question for LVMH investors is that Arnault is 76 and has already extended the CEO age limit from 75 to 80. The succession question for LVMH remains open.

Hermes has successfully passed the baton across six generations without missing a beat. LVMH has never done it once.

Governance

Hermes operates as a societe en commandite par actions (SCA), a French limited partnership where managing partners (all family members) hold executive authority that cannot be overridden by a shareholder majority vote. The family controls approximately 67% of capital through holding entities H51, H2, and other family vehicles. When LVMH quietly accumulated a 17% stake through equity swaps in 2010, the family pooled 72 members' shares into H51 and repelled the takeover. LVMH eventually divested by 2014.

This structure protects the shareholders from external takeovers, allowing Hermes to make decisions that prioritize the brand over decades rather than quarters: refusing to ramp production, maintaining slower artisanal methods, and turning away short-term revenue in favor of long-term scarcity. A publicly pressured board would struggle to approve any of these.

In the next premium subscriber section, I cover,

- Risks of a Hermes investment

- My Valuation watchlist Buy Levels and specific portfolio next steps with regards to Hermes

Risks

The first risk that any prospective investor of Hermes needs to pay attention to is...

🔒Unlock below with premium tier